Email

Email Print

Print

Fan Out Packaging Market – By Type , By Process Type , By Business Model , By Geography – Opportunity Analysis & Industry Forecast, 2024-2030.

Fan Out Packaging Market Overview

The global Fan-out Packaging Market is estimated to grow at a CAGR of 15.2% during the forecast period 2024-2030 and reach $5.2 billion by 2030. The Fan-Out Packaging market is rapidly advancing, driven by several significant trends that reflect the evolving demands of the semiconductor industry. A key trend is the increasing adoption of Fan-Out Wafer-Level Packaging (FOWLP) technology, which offers superior performance and miniaturization capabilities compared to traditional packaging methods. This technology is particularly favored for applications in smartphones, IoT devices, and automotive electronics, where space and power efficiency are critical. Another major trend is the growing emphasis on heterogeneous integration, where multiple types of chips, such as processors, memory, and sensors, are integrated into a single package. This approach enhances functionality and performance while reducing the overall footprint of electronic devices. The demand for advanced packaging solutions is also being propelled by the rise of 5G technology, which requires highly efficient and compact components to support faster data transmission and lower latency.

Additionally, advancements in materials and processes, such as the use of redistribution layers (RDL) and through-silicon vias (TSVs), are improving the electrical performance and reliability of fan-out packages. The industry is also seeing a push towards more cost-effective and scalable manufacturing techniques to meet the high-volume demands of consumer electronics. Overall, the Fan-Out Packaging market is characterized by continuous innovation aimed at meeting the challenges of miniaturization, integration, and performance enhancement in modern electronics.

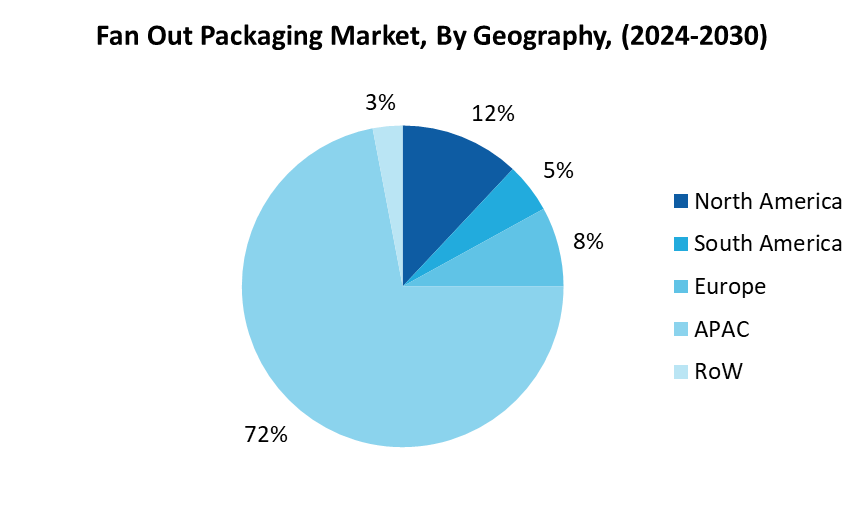

Market Snapshot:

Fan Out Packaging Market - Report Coverage:

The “Fan Out Packaging Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Fan Out Packaging Market.

| Attribute | Segment |

|---|---|

|

|

|

By Process Type |

|

|

By Business Model |

|

|

By Application |

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- The COVID-19 pandemic significantly impacted the growth of the Fan-Out Packaging market, both positively and negatively. On one hand, the pandemic disrupted global supply chains, causing delays in production and shipment of semiconductor components, which affected the availability of raw materials and manufacturing equipment necessary for fan-out packaging. This led to short-term slowdowns and increased costs for manufacturers. On the other hand, the surge in demand for electronic devices, driven by remote work, online education, and increased digital connectivity during the pandemic, accelerated the adoption of advanced semiconductor packaging solutions. The need for higher performance and smaller form factors in consumer electronics, 5G infrastructure, and automotive electronics bolstered the demand for fan-out packaging technology. Additionally, the pandemic underscored the importance of robust and resilient supply chains, prompting investments in local semiconductor manufacturing capabilities, which further supported market growth.

- The Russia-Ukraine war has had a notable impact on the growth of the Fan-Out Packaging market by exacerbating global supply chain disruptions and creating economic uncertainty. The conflict has led to significant instability in the supply of critical raw materials, such as neon gas and palladium, which are essential for semiconductor manufacturing processes, including fan-out packaging. The war has also intensified geopolitical tensions and trade restrictions, leading to increased costs and delays in the production and transportation of semiconductor components. Additionally, the heightened energy prices and economic sanctions associated with the conflict have strained financial resources, further complicating operations for semiconductor manufacturers. On the other hand, the ongoing demand for advanced electronic devices and the push for technological self-sufficiency in various regions have driven investments in local semiconductor production capabilities, including fan-out packaging technologies. Overall, while the Russia-Ukraine war has introduced significant hurdles, it has also underscored the importance of resilient and diversified supply chains, prompting strategic shifts in the industry to mitigate future risks.

Key Takeaways:

-

Asia-Pacific to Register Highest Growth:

Asia-Pacific is anticipated to experience the highest growth of CAGR of 72% in the Fan Out Packaging Market between 2024 and 2030. Asia-Pacific region incorporates chief economies of the Asian region, namely Taiwan, China, India, Japan and so on. As stated by Invest in India, the global electronics market is estimated to be over $2 tn. India, one of the largest electronics markets in the world anticipated reaching $400 bn by 2025. This is set to contribute to the market growth rate during forecast period 2024-2030. In November 2021, Amkor technology announced its plans to expand its advanced packaging technology capacity by building a new factory in Bac Ninh, Vietnam. Taiwan Semiconductor Manufacturing Co., the world's biggest contract chipmaker, and major supplier to Apple Inc., stated that it is planning a $100bn investment in the expansion. As a part of this, it has started expansions in Taiwan, Japan, US. These expansions by the major Fan-out Packaging Materials and Equipment manufacturers is set to boost the market growth rate during forecast period 2024-2030.

-

Power Management Integrated circuits (PMICs) is Leading the Market:

Power Management Integrated circuits is dominating the market in 2023 at 23.1% share. The growing ICT sector is the major factor contributing to the market growth rate. The Ministry of Industry and Information Technology (MIIT) of China, stated that the added value of electronic information manufacturers with annual operating revenues rose about $3.09 million indicating 19.8% year on year, with the compound annual growth rate reaching 12.5% over between 2021-2023. In August 2021, Samsung Group has unveiled a $205 Million expansion over 2022-2025 period. In 2021, Xiaomi announced expansion of smartphone, TV capacity in India with 3 new plants to meet the demand in the country by 2024. In 2021, South Korea unveiled ambitious plans to spend roughly $450 Million to build the world’s biggest chipmaking base over the next decade, joining China and the U.S. in a global race to dominate the key technology. These investments are analyzed to contribute to the market growth rate

-

Core Fan-out is to Register the Highest Growth:

The Core Fan-Out segment is projected to grow at a CAGR of 4.29% during 2024-2030. Fan-out packages consist of dies and redistribution layers in which the redistribution layers are the copper metal interconnects that electrically connect one part of the package to the other. The growing semiconductor industry coupled with the increasing investment by various government bodies is set to boost its market growth in the future. As a part of this, in December 2021, the government approved a Rs 76,000-crore investment by 2025 to boost semiconductor and display manufacturing in the country in an bid to position India as a global hub for hi-tech production, and attract large chip makers. In July 2021, the US Senate has passed a landmark bill that would unlock an eye-watering $52 Million to boost the national production of semiconductors. The investment is part of a wider package of about $250 Million that covers scientific endeavors ranging from artificial intelligence to quantum communications, called the US Innovation and Competition Act

-

Introduction of ECP (Encapsulated Chip Package) technology in Fan-Out Packaging Solution:

The Introduction of ECP (Encapsulated Chip Package) technology in Fan-Out Packaging Solution is set to drive its market during the forecast period. Electronics miniaturization in the form of integrated circuits has become an indispensable part of our lives since the advent of the Internet and multimedia. The rapid development of integrated circuits is dependent on advancements in not only chip design and manufacturing, but also chip packaging, to ensure its long-term operation and reliability. Unlike other packaging processes that use wafer reconstitution molding compounds, ECP technology is an advanced chip-first and face-down packaging process. Instead of the traditional liquid or powder molding compound, the ECP process employs a laminating molding film. Moreover, the lamination process replaces the wafer molding process for ultra-thin chip packaging. The lamination process allows reconstituted wafers to achieve a high degree of flatness while avoiding wafer cavities. Furthermore, when compared to liquid or powder compounds for wafer molding, it can effectively reduce chip offset and achieve small-size, high fan-out ratio packaging. In addition, the silicon support on the backside of the reconstituted wafer can effectively reduce warpage and overcome warpage-related problems owing to the unique ECP process and the low modulus characteristics of the lamination film. ECP technology not only enables fan-out, single-chip, and multi-chip packaging, but also five-sided package protection. It has a small size and a high fan-out ratio, allowing it to effectively overcome wafer warpage.

-

Rising Automotive and Industrial Applications:

Surge in rise of Automotive and Industrial applications is driving the Fan-Out Packaging Materials & Equipment Market growth. The current automotive market for the integrated circuit (IC) packaging industry has grown significantly owing to the increasing demand for automation and higher performance in vehicles. These changes in the automotive market set to allow cars to become more reliable and intelligent. To meet the increasingly complex demands of the automotive market, the semiconductor packaging industry is shifting its focus to prioritize the development of advanced packages for next-generation automotive market requirements. Wire bond packages are typically used for automotive integrated circuits. The packaging industry is shifting toward high performance flip chip and advanced fan-out packages for automotive infotainment, GPS, and radar applications as the complexity and performance requirements of automotive applications increase. For instance, ASE Group established a FO-WLP line in Kaohsiung, Taiwan, with other major OSATs in production or planning their fan-out packaging launch phases. In addition, according to Powertech Technology Inc., Fab 3 in Hsinchu Science Park set to be the world's first fab to commercially use fan-out panel-level packaging (FOPLP) technology. Furthermore, the expanding market for fifth generation (5G) wireless communication and high performance computing has allowed manufacturers to develop newer technologies. For example, TSMC, as the sole leader in the High-Density Fan-out segment, intends to expand its FO-WLP segment into technologies such as inFO-Antenna-in-Package (AiP) and inFO-on-Substrate (oS).

-

High Manufacturing Cost Hampers the Growth of the Market:

High Manufacturing cost owing to war page causing differential shrinkage of material during FOWLP set to restrict the growth of the Fan-Out Packaging Materials & Equipment Market. Fan-out wafer-level packaging (FOWLP) has numerous advantages over other packaging technologies. FOWLP is one of the smallest packaging options, but unlike fan-in wafer-level packaging, the IO count is not limited to the die area. FOWLP's popularity is growing as a result of these benefits. While the cost of FOWLP is usually quite high, there are still opportunities for future cost savings. Many FOWLP suppliers are looking into panel-based manufacturing as an alternative to the current wafer-based approach.

For more details on this report - Request for Sample

Key Market Players:

Product launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Fan Out Packaging market. The top 10 companies in this industry are listed below:

- Taiwan Semiconductor Manufacturing Company Limited

- ASE Group

- JCET Group

- Amkor Technology

- Powertech Technology Inc.

- Nepes Laweh

- Samsung Electronics

- Evatec AG

- Camtek

- Atotech

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

15.2% |

|

Market Size in 2030 |

$5.2 Billion |

|

Segments Covered |

Type, Process Type, Business Model, Application and Region |

|

Geographies Covered |

North America, South America, Europe, APAC, RoW |

|

Key Market Players |

|

For more Lifesciences and Healthcare Market reports, please click here

The Fan Out Packaging Market is projected to grow at 15.2% CAGR during the forecast period 2024-2030.

Fan Out Packaging Market size is estimated to surpass $5.2 Billion by 2030 from $1.93 Billion in 2023.

The leading players in the Fan Out Packaging Market are Taiwan Semiconductor Manufacturing Company Limited, ASE Group, JCET Group, Amkor Technology, Powertech Technology Inc and others.

The increasing adoption of Fan-Out Wafer-Level Packaging (FOWLP) technology is a major key trend, which offers superior performance and miniaturization capabilities compared to traditional packaging methods. This technology is particularly favored for applications in smartphones, IoT devices, and automotive electronics, where space and power efficiency are critical.

Surge in rise of Automotive and Industrial applications is driving the Fan-Out Packaging Materials & Equipment Market growth. The current automotive market for the integrated circuit (IC) packaging industry has grown significantly owing to the increasing demand for automation and higher performance in vehicles.