Email

Email Print

Print

Epoxy Composites Market - Industry Analysis, Market Size, Share, Trends, Growth And Forecast 2024-2030

Epoxy Composites Market Overview

The epoxy composite market size is forecast to reach USD 38.7 billion by 2030, after growing at a CAGR of 5.7% during the forecast period 2024-2030. Epoxy composites are a form of polymer material in which a polymer matrix reinforced with fibers or other fillers is made using an epoxy resin. This enables the development of durable components with extremely high strength-to-weight ratios. Epoxy composites have lower densities than metals, which may save a lot of fuel in automobile and aeronautical applications. Epoxy composites find applications in various industries, including aerospace, automotive, marine, construction, sports equipment, and electronics. The rise in the growth of the automotive & aerospace sectors would boost the demand for epoxy composite. According to, the International Organization of Motor Vehicle Manufacturers (OICA), the total production of vehicles in America is increased from 15,692,927 in 2020 to 17,756,263 units in 2022. Therefore, the rise in auto production would increase the demand for the epoxy composite market during the forecast period. In the construction sector, epoxy composites find applications in infrastructure projects, including bridges, buildings, and pipelines. The lifetime and structural integrity of many building projects are enhanced by the great strength and endurance of these composite materials. Epoxy's considerable aviation success is not limited to structural composite applications. They have been vital in merging and polishing structural pieces, but they are also necessary for making them last. Epoxy resins are utilized in anti-corrosion coatings and adhesive applications, where they can effectively replace or supplement heavier bonding methods such as mechanical fasteners.

Market Snapshot :-

Report Coverage

The report “Epoxy composite market – Forecast (2024-2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the epoxy composite market.

By Fiber Type: Carbon, Glass and Others

By Matrix Type: Polymer, Metal and Ceramics.

By Fabrication Process: Lay-up, Compression Moulding, Resin Injection, Resin Transfer Moulding, Filament Winding and Pultrusion.

By End-use Industry: Building & Construction (Residential, Commercial, Infrastructure and Others), Transportation (Automotive, Marine, Aerospace & Defence, Rail), Electric & Electronics, Energy, Healthcare, Sporting & Consumer Goods, Industrial and Others.

By Geography: North America, South America, Europe, APAC, and RoW.

Key Takeaways

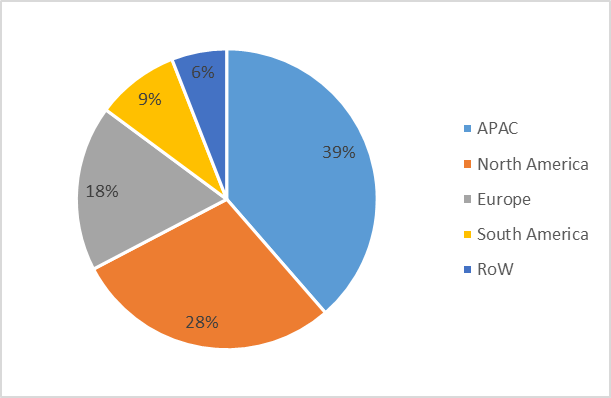

- APAC held the largest market share with 39% in 2023. The Asia-Pacific region is maintaining its leadership position. This rise is attributed to the region's great growth potential as a result of the quickly increasing aircraft manufacturing and the ambitious expansion goals set by many businesses in the electrical and electronics sectors.

- Carbon fiber composites are being explored for automotive applications, especially in high-performance vehicles, to achieve weight reduction and enhance performance. The trend toward electric vehicles and the need for lightweight materials are driving the adoption of carbon fiber-reinforced epoxy composites.

- In 2022, Solvay launched LTM® 350, a next-generation lay-up-based carbon fiber epoxy prepreg tooling material. It is intended to provide considerable time and cost benefits for industrial, aerospace, automotive, and race car applications.

By Product - Segment Analysis

Carbon dominated the epoxy composite market in 2023. Carbon epoxy composites have strong structural strength and good tensile characteristics while also being relatively lightweight. It has good thermal and electrical qualities, is fire resistant, and resists corrosion. Carbon fiber composites are being explored for automotive applications, especially in high-performance vehicles, to achieve weight reduction and enhance performance. Carbon epoxy composites have strong structural strength and good tensile characteristics while also being relatively lightweight. It has good thermal and electrical qualities, is fire resistant, and resists corrosion. It is utilized in industries including aircraft, sporting goods, automotive, and transportation where weight, strength, and durability are crucial factors. Continuous carbon-fiber-reinforced polymer composites (CFRPs) are produced by pultrusion, vacuum infusion, resin transfer molding, and compression molding of preforms. A barrier to carbon fiber's broad use in non-aerospace applications has been its expensive price. According to ACS Publications in June 2023, Thermal expansion coefficients are lower in carbon-containing composites (10 and 20%) than in non-carbon-containing composites. Carbon materials possess inherently low coefficients of thermal expansion compared to many other materials. When these materials are incorporated into the epoxy matrix, they can influence the thermal behavior of the composite. The high stiffness and low thermal expansion properties of carbon segments can help mitigate the expansion of the composite material when exposed to temperature changes, resulting in a lower overall coefficient of thermal expansion.

By End Use Industry - Segment Analysis

Transportation dominated the epoxy composite market in 2023. Numerous automobile applications, such as the interior headliner, underbody system, instrument panel, bumper beam, air duct, airbag housing, engine cover, etc., employ epoxy composites. Epoxy Composites consumption in automotive and transportation applications is increasing as a result of a growing demand for lighter, safer, and more energy-efficient automobiles. In 2023, the India Electronics and Semiconductor Association (IESA) and the U.S. Semiconductor Industry Association (SIA) jointly announced intentions to establish a private-sector task force to improve cooperation between the two nations in the global semiconductor ecosystem. Epoxy composite materials are used in a variety of transportation-related applications, which improves safety and lowers costs. Throughout the lifecycle of the final product, for instance, our PET structural core material and a variety of laminating and adhesive technologies offer cost-effective manufacturing cycles, safety, FST qualities, low toxicity, and energy savings. Epoxy composite materials are considered to be stronger than steel and aluminum while still weighing significantly less, resulting in a 25–70% weight reduction. These characteristics of epoxy composites allowed for a wider range of applications, including those in the transportation, automotive, and aerospace, sectors.

By Geography - Segment Analysis

APAC Epoxy composite market generated a revenue of $10.2 billion in 2023 and is projected to reach a revenue of $15.9 billion by 2030 growing at a CAGR of 6.6% during 2024-2030. The growth of the transportation industry is propelling the growth of the market. For instance, according to the Civil Aviation Administration of China (CAAC), China plans to expand domestic flights from 2023-2025. One of the most comprehensive initiatives to reach the pinnacle of aerospace development and production may be seen in the Chinese aerospace strategy. Over the next few years, China is anticipated to be the greatest single market in the world for the selling of civil aircraft. Automotive, electrical, machine tool, ship, chemical, processed food, textile, and non-ferrous metal manufacturers include Japan among the most technologically advanced nations in the world. The country has shared this role with the United States as the hub of global manufacturing. One of the goods that Japan exports the most is processed food, followed by consumer electronics, semiconductors, and automobiles. India is a global leader in the automotive sector as well thanks to its exports, sizeable domestic market, and domestic production capacity. Generally speaking, the country's automobile sector is relatively robust, generating about 36 lakh cars each year. The automotive industry will be the primary driver of demand for epoxy composite materials in the future as a result of increased auto production brought on by both local and foreign investment.

Epoxy Composite Market Share (%) By Region, 2023

For more details on this report - Request for Sample

Drivers – Epoxy composite market

-

The widespread use of epoxy composites in the aerospace sector

composite materials based on epoxy have become indispensable in the aerospace sector. They are mostly utilized as protective coatings on aircraft to increase their lifespan. According to IndustryARC estimates, the Aerospace & Defense market is estimated to reach $11.9 billion by 2024-2030, increasing at a CAGR of 7.5%. Epoxy's considerable aviation success is not limited to structural composite applications. They have been vital in merging and polishing structural pieces, but they are also necessary for making them last. Epoxy resins are utilized in anti-corrosion coatings and adhesive applications, where they can effectively replace or supplement heavier bonding methods such as mechanical fasteners. Furthermore, structural weight savings have an important side advantage in terms of sustainability in terms of airplane emissions. Indeed, regulatory bodies have already set CO2 emissions targets, and future emissions targets create a problem for the aerospace industry and global carriers. Fiber-reinforced polymer composite materials are fast gaining ground as preferred materials for the construction of aircraft and space crafts. According to Epoxy Europe, around 30,000 new aircraft deliveries are planned over the next 20 years, with approximately 10,000 current planes needing to be refurbished. Epoxy composites reduced the initial 2,000 pieces required for metal-based tail fins to less than 100, reducing weight and production costs. This drives the epoxy composite market and enables airlines to operate successfully in a fiercely competitive global environment. Design and maintenance efforts are primarily aimed at weight reductions for improved fuel economy and lowering service costs to ultimately reduce operating costs.

-

Fresh approaches to lightweight composite materials

For a quicker cure and greater strength, epoxy resins are necessary when making composites. Epoxy composite products have longer shelf lives than conventional ones. These composite materials display exceptional performance and strength in a variety of automotive and aerospace applications, despite being roughly 50% lighter than steel and nearly 30% lighter than aluminum. Due to their exceptional strength and lightweight design, they are also used in specific building applications, which has helped to expand the market and increase spending on composites research and development by the space, aerospace, marine, and automotive industries. Epoxy Composites are used in a variety of applications in the automotive industry. Additionally, epoxy-based carbon fiber-reinforced composites are used in the aerospace industry. The rapid development of lightweight and high-strength composites in the aerospace, transportation, and maritime navigation areas creates a significant need for energy and fuel. The use of lightweight and high-strength epoxy-based composites can effectively result in a decrease in energy consumption and an increase in fuel economy, driving the growth of the epoxy composites market. The aircraft (or vehicle) can obtain a longer range by reducing its specific gravity during voyage.

Challenges – Epoxy composite market

Inadequate Source: Expert Insights & IndustryARC Analysis

-

Instability in the prices of raw materials

The raw material prices for all composite grades are substantially high. Most raw material supply chains are tight due to low inventories, idled capacity, planned, and unplanned outages, some feedstock availability issues, and in some cases poor harvests. Companies that supply raw materials are making efforts to absorb these cost increases, but it is acknowledged that the situation has gotten out of hand and that further revisions to sales prices are necessary to guarantee stable supplies in the future. For instance, in January 2022, DIC Corporation changed the prices of epoxy resins and other raw materials. However, due to tight market conditions and problems with the supply-demand balance for specific materials, the price of raw materials has risen even more in the months since. The Company's financial burden has been made worse by rapidly increasing utility costs and abrupt exchange rate fluctuations. The raw materials used to make epoxies, like BPA and ECH, are derived from petroleum. As a result, changes in the price of crude oil have an impact on both the raw material costs for these products as well as the price of epoxy resins. In 2022, in the Chinese market, the price of domestic carbon fiber averaged 180 RMB/MT, while that of T300 grade 12K carbon fiber averaged 180-200 RMB/MT. Price changes in these raw materials hurt small-scale manufacturers and their profit margins. Thus, owing to the high prices of raw materials and high processing costs, the market size of epoxy composites is displaying a slightly lower growth rate.

Market Landscape

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in the Epoxy composite market. in 2023, The major players in the Epoxy composite market are Axiom Materials Inc, Hexcel Corporation, SGL Carbon, Mitsubishi Chemical Corporation, Teijin Ltd, Solvay Group, Toray Industries, Inc., Gurit Holding AG, Park Aerospace Corporation, Owens Corning and Others.

Developments:

- In March 2022, Trelleborg Sealing Solutions (Trelleborg, Sweden) introduced their Orkot C620 composite material features a strong fiberglass, which was created specially to fulfill the demands of the aircraft sector, including the need for a robust and light material to endure the high pressures and stresses landing gear.

- In September 2022, Solvay launched LTM® 350, a next-generation lay-up-based carbon fiber epoxy prepreg tooling material. It is intended to provideconsiderable time and cost benefits for industrial, aerospace, automotive,and race car applications. With its fast lay-up, fast initial cure, and shortpost-cure cycles, carbon fiber epoxy prepreg establishes new benchmarksin cost-effective composite tooling.

For more Chemicals and Materials Market reports, please click here

1. Epoxy composite market- Overview

1.1. Definitions and Scope

2. Epoxy composite market - Executive Summary

3. Epoxy composite market - Comparative Analysis

3.1. Company Benchmarking - Key Companies

3.2. Global Financial Analysis - Key Companies

3.3. Market Share Analysis - Key Companies

3.4. Patent Analysis

3.5. Pricing Analysis

4. Epoxy composite market - Start-up Companies Scenario

4.1. Key Start-up Company Analysis by

4.1.1. Investment

4.1.2. Revenue

4.1.3. Venture Capital and Funding Scenario

5. Epoxy composite market – Market Entry Scenario Premium

5.1. Regulatory Framework Overview

5.2. New Business and Ease of Doing Business Index

5.3. Case Studies of Successful Ventures

6. Epoxy composite market - Forces

6.1. Market Drivers

6.2. Market Constraints

6.3. Market Challenges

6.4. Porter's Five Force Model

6.4.1. Bargaining Power of Suppliers

6.4.2. Bargaining Powers of Customers

6.4.3. Threat of New Entrants

6.4.4. Rivalry Among Existing Players

6.4.5. Threat of Substitutes

7. Epoxy composite market – Strategic Analysis

7.1. Value Chain Analysis

7.2. Opportunities Analysis

7.3. Market Life Cycle

8. Epoxy composite market – by Fiber Type (Market Size – $Million/$Billion)

8.1. Carbon

8.2. Glass

8.3. Others.

9. Epoxy composite market – by Matrix Type (Market Size – $Million/$Billion)

9.1. Polymer

9.2. Metal

9.3. Ceramics

10. Epoxy composite market – by Fabrication Process (Market Size – $Million/$Billion)

10.1. Lay-up

10.2. Compression Moulding

10.3. Resin Injection

10.4. Resin Transfer Moulding

10.5. Filament Winding

10.6. Pultrusion

11. Epoxy composite market – by End User Industry (Market Size – $Million/$Billion)

11.1. Building & Construction

11.1.1. Residential

11.1.2. Commercial

11.1.3. Infrastructure

11.1.4. Others

11.2. Transportation

11.2.1. Automotive

11.2.2. Marine

11.2.3. Aerospace & Defence

11.2.4. Rail

11.3. Electric & Electronics

11.4. Energy

11.5. Healthcare

11.6. Sporting & Consumer Goods

11.7. Industrial

11.8. Others

12. Epoxy composite market – by Geography (Market Size – $Million/$Billion)

12.1. North America

12.1.1. U.S

12.1.2. Canada

12.1.3. Mexico

12.2. Europe

12.2.1. Germany

12.2.2. France

12.2.3. UK

12.2.4. Italy

12.2.5. Spain

12.2.6. Belgium

12.2.7. Netherlands

12.2.8. Rest of Europe

12.3. Asia-Pacific

12.3.1. China

12.3.2. Japan

12.3.3. South Korea

12.3.4. India

12.3.5. Australia & New Zealand

12.3.6. Indonesia

12.3.7. Malaysia

12.3.8. Taiwan

12.3.9. Rest of Asia-Pacific

12.4. South America

12.4.1. Brazil

12.4.2. Argentina

12.4.3. Chile

12.4.4. Rest of South America

12.5. Rest of The World

12.5.1. Middle East

12.5.1.1. Saudi Arabia

12.5.1.2. UAE

12.5.1.3. Israel

12.5.1.4. Rest of Middle East

12.5.2. Africa

12.5.2.1. South Africa

12.5.2.2. Nigeria

12.5.2.3. Rest of Africa

13. Epoxy composite market – Entropy

14. Epoxy composite market – Industry/Segment Competition Landscape

14.1. Market Share Analysis

14.1.1. Market Share by Product Type – Key Companies

14.1.2. Market Share by Region – Key Companies

14.1.3. Market Share by Country – Key Companies

14.2. Competition Matrix

14.3. Best Practices for Companies

15. Epoxy composite market – Key Company List by Country Premium

16. Epoxy composite market - Company Analysis

16.1. Axiom Materials Inc.

16.2. Hexcel Corporation

16.3. SGL Carbon

16.4. Mitsubishi Chemical Corporation

16.5. Teijin Ltd

16.6. Solvay Group

16.7. Toray Industries Inc.

16.8. Gurit Holding AG

16.9. Park Aerospace Corporation

16.10. Owens Corning

"Financials to the Private Companies would be provided on best-effort basis."