Email

Email Print

Print

U.S Hardwood Lumber Market – By Type , By Grade , By Application , By Sales Channel Opportunity Analysis & Industry Forecast, 2024-2030

U.S Hardwood Lumber Market Overview:

U.S Hardwood Lumber Market size is estimated to reach US$6.1 billion by 2030, growing at a CAGR of 5.2% during the forecast period 2024-2030. Multiple factors that reflect industry trends and market demands drive the U.S. hardwood lumber market. Demand for hardwood is fueled by construction and renovation growth, particularly with increasing home remodelling projects. Hardwood is such a desirable option because it’s a renewable material and it’s certified by FSC and SFI. High quality U.S. hardwoods continue to be highly sought after in global markets such as China and Europe, and production is boosted by export demand from these markets. Improvements in sawmilling and drying processes increase product quality and efficiency, and are applied to a range of uses. Premium hardwoods are the preferred choice of the growing furniture industry for high end products. Government grants also help to support local manufacturing and infrastructure and forest health management to provide resource availability to address wildfire risks and pest outbreaks. Together, these drivers keep and grow the market.The two major trends in U.S. hardwood lumber market are the rising popularity of engineered hardwood products and expansion of urban forestry initiatives. Advances in wood modification technologies are driving the popularity of engineered hardwood, which is both durable and cost effective. A thermally modified cross laminated timber structure was tested for seismic safety by the U.S. Army Engineer Research and Development Centre in November 2024, demonstrating the potential of modified wood in construction. Urban forestry is also changing the market through promoting sustainability and equity. American Forests allocated more than $25 million in September 2024 to 36 community projects through the Tree Equity Catalyst Fund, recycling urban wood and balancing tree cover and environmental benefits.

Market Snapshot:

U.S Hardwood Lumber Market - Report Coverage:

The “U.S Hardwood Lumber Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the U.S Hardwood Lumber Market.

| Attribute | Segment |

|---|---|

|

By Grade |

|

|

By Sales Channel |

|

|

By Type |

|

|

By Application |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- The U.S. hardwood lumber market has been severely affected by the COVID-19 pandemic with lockdowns and supply chain challenges reducing production and causing delays in shipments. Inventory levels of key hardwood types, such as oak and maple, were quickly cut back; sawmills and processing units operated at lower capacity. In addition, demand fluctuated with the initial slowdown of industries like furniture and flooring, but there was an increase in DIY home improvement projects driving retail level demand. Logistical hurdles and a falling international demand also hit the export markets.

- The Russia-Ukraine war compounded the supply chain problems and increased transportation and production costs to further strain the U.S. hardwood lumber market. The increased demand for U.S. hardwoods in international markets was the result of sanctions on Russia limiting the global supply of certain wood products. But the conflict led to high energy prices that bumped up lumber processing's operational expense. In addition, European markets became unstable, drawing attention to North America and higher export activity but also regional shortages. Such compounded effects have changed market dynamics to the extent that supply chains are becoming more diversified and price stabilization strategies are becoming more important.

Key Takeaways

Furniture is the Largest Segment

In the U.S. hardwood lumber market, furniture remains the largest application segment due to evolving consumer preferences and the increasing popularity of modern interior styles. An online destination for home design and furnishings, Houzz reports that searches for 'organic modern' interior design ideas rocketed 245 % in the first quarter of 2024 versus the prior year. This is in line with a growing trend on homeowners’ part to include sustainable and minimalist elements in their home ambience hence increased demand for hardwood furniture that fits such principles. This shift has been recognized by manufacturers who are now designing their collections to fulfil consumers’ expectations of high quality, stylish and durable furniture made from materials such as oak, walnut and maple. The long-lasting appeal, versatility and ability of hardwood to add a premium touch to interior is what makes it the preferred choice for furniture production, making it a market leader. The wide demand aspect of the furniture segment points at its prime role in the growth of the hardwood lumber industry.

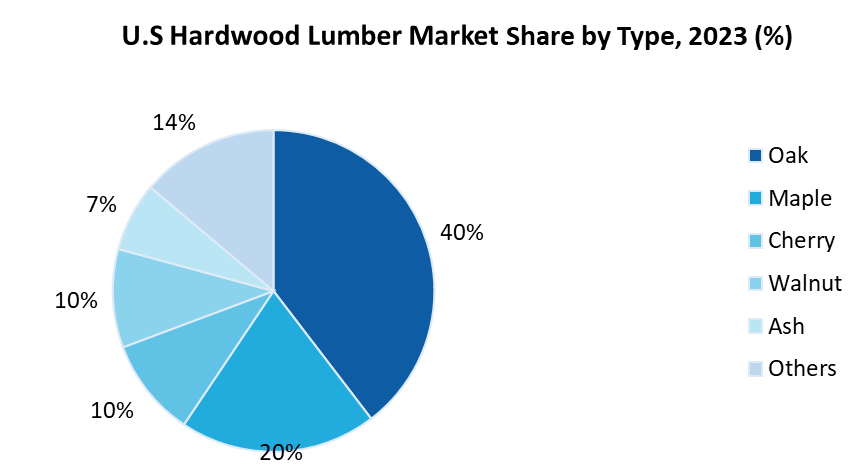

Oak is the largest segment

In the U.S. hardwood lumber market, oak dominates as the largest segment by type, largely due to the abundance and versatility of white oak. White oak trees are exclusively native to North America, and are widely distributed throughout the eastern United States, forming a foundation of mixed hardwood forests. White oak comprises approximately 33% of the American hardwood resource and is found in many subspecies in a variety of climates and terrains, according to the American Hardwood Export Council. The adaptability of the wood then gives it distinctive characteristics, dependent on growth rates in northern and southern areas. White oak is also highly sustainable. U.S. white oak growing stock is 2.26 billion m³, or 15.5% of the nation’s hardwood stock, according to Forest Inventory Analysis (FIA) data. Growth of 40.1 million m³ annually is far exceeding the 20.1 million m³ harvested, and white oak resources are increasing by 20 million m³ annually, providing ample supply for both domestic and export markets.

Construction and Renovation Drives the Market

Growth in the U.S. hardwood lumber market is driven by strong growth in construction and renovation, fueled by high levels of infrastructure investments and ongoing homeowner spending on improvements. The U.S. Department of Treasury reports that real non-residential construction spending has increased by 15% since the Infrastructure Investment and Jobs Act (IIJA) was passed, and federal dollars are being used to fund critical public projects, such as roads, bridges, and water systems. The infusion of public investment has led to private sector activity, as private transportation construction spending has increased by 14%. Simultaneously, ongoing residential renovations proceed at a steady clip as homeowners add aesthetic, comfortable, and money increasing improvements to their abodes. The Remodeling Futures Program at the Joint Center for Housing Studies of Harvard University’s Leading Indicator of Remodeling Activity (LIRA) projects home improvement spending will reach $477 billion by late 2024, and will remain strong even as the market corrects after the pandemic boom. These trends in public infrastructure and private renovation drive consistent demand for hardwood lumber among many applications.

Sustainability and Eco-Friendly Trends to Boost the Market

Sustainability and eco-friendly trends are prominent drivers in the U.S. hardwood lumber market, and they reflect the growing global and domestic efforts to fight climate change. The U.S. Green Building Council states buildings are responsible for more than 40% of global CO2 emissions, and that sustainable construction is a key solution to that environmental impact. LEED certified structures and green buildings offer tangible benefits in that they reduce carbon emissions, conserve energy and water and waste. Not only are they addressing environmental concerns, these practices also offer economic advantage, namely lower maintenance and operating costs, shorter payback periods and increased asset value. For example, LEED certified buildings have reported nearly 20% lower maintenance costs and up to 10% or more in property value, as per U.S. Green Building Council. The rapid growth of green construction is being driven by health focused designs and client demand, which together have created millions of jobs and billions in economic impact. The demand for sustainable materials like hardwood lumber, a renewable and durable material imperative for eco-friendly building, is driven by this trend.

Moisture Related Issues to Hamper the Market

One of the significant challenges in the U.S. hardwood lumber market is managing moisture-related wood deformation issues such as cupping, crowning, and buckling, which directly affect the quality and usability of hardwood lumber. Relative humidity (RH) changes with season are critical in these deformations. During winter, compositional wood shrinks and cracks due to loss of moisture content (MC). On the other hand, cupping, where the edges of the boards rise, or crowning, where the center is elevated, are often the result of high RH levels or water exposure. Extreme cases of moisture exposure can see boards pull away from subfloor, and in the worst cases, can cause buckling. The environmental conditions that give rise to these challenges require careful control of RH and MC during production, storage, and application. Some problems go away on their own with the changing seasons, but improper handling can result in costly damages, which is why it’s important to take climate control measures like humidifiers to keep wood stable and maintain market value.

For more details on this report - Request for Sample

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the U.S Hardwood Lumber Market. The top 10 companies in the U.S Hardwood Lumber Market are:

- Beasley Forest Products

- Baillie Lumber Co.

- Gutchess Lumber Co., Inc.

- Midwest Hardwood Corporation

- Northwest Hardwoods

- HHP Inc.

- MacDonald & Owen Lumber Company

- AHC Hardwood Group

- Weyerhaeuser

- Thompson Hardwoods

Scope of Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

5.2% |

|

Market Size in 2030 |

$6.1 billion |

|

Segments Covered |

By Type, By Grade, By Application and By Sales Channel |

|

Key Market Players |

|

For more Chemicals and Materials Market reports, please click here

The U.S Hardwood Lumber Market is forecast to grow at 5.2% during the forecast period 2024-2030

The U.S Hardwood Lumber Market size is projected to reach US$6.1 billion by 2030

The leading players are Beasley Forest Products, Baillie Lumber Co., Gutchess Lumber Co., Inc., Midwest Hardwood Corporation, Northwest Hardwoods and others.

Integration of smart technology and a focus on sustainability are major trends in the market.

Construction and renovation growth, sustainability and eco-friendly trends, export demand, technological advancements, growing furniture industry, government and industry support, forest health management are driving the U.S Hardwood Lumber Market growth.