Email

Email Print

Print

U.S Bituminous Coal Market – By Sulfur Content , By Type , By End-Use Industry - Opportunity Analysis & Industry Forecast, 2024-2030

U.S Bituminous Coal Market Overview:

The U.S Bituminous Coal Market size is estimated to reach 478 MT by 2030, growing at a CAGR of 6.5% during the forecast period 2024-2030. In regions that depend on coal-fired power plants, coal is still utilized to meet the growing demand for energy, particularly during periods of peak demand. Additionally, regions like Asia Pacific continue to have a significant demand for high-quality U.S. coal for industrial and power production purposes. Moreover, technical advancements like increased automation and better mining operations efficiency help to lower costs and boost unit output, making coal a competitive energy and industrial sector.The two major trends influencing the U.S. bituminous coal industry are the move toward cleaner coal technology and the increased need for steel. According to the National Mining Association (NMA), cleaner coal technologies including selective catalytic reduction (SCR), low nitrogen oxide (NOx) burners, and flue gas desulfurization have made it possible to significantly reduce hazardous emissions like sulfur dioxide, NOx, and particulates. This promotes innovation and investment in coal-fired power production in line with tightening environmental restrictions and the demand for sustainable energy alternatives. Bituminous coal remains a crucial component in the steelmaking process, particularly for coking coal.

Market Snapshot:

U.S Bituminous Coal Market - Report Coverage:

The “U.S Bituminous Coal Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the U.S Bituminous Coal Market.

| Attribute | Segment |

|---|---|

|

By Sulfur Content |

|

|

By Type |

|

|

By End Use Industry |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- Weakening domestic demand and movement challenges posed by the COVID-19 pandemic disrupted the U.S. bituminous coal market. A fall in coal consumption for power generation and steel production followed lockdowns and a fall in industrial activity. Volume fell due to reduced global demand and supply chain disruptions including in Asia and Europe. Post pandemic, the market recovered slightly, as industrial activities started and international coal prices also recovered on the back of supply constraints in other major coal producing regions.

- Market dynamics were reshaped by the Russia-Ukraine war, as demand for U.S. bituminous coal in Europe grew. European nations sought alternative suppliers to Russian energy exports, coal exports from the U.S. were pushed up to meet energy security needs. It also increased transportation and fuel charges reducing coal producers' profit margins. Furthermore, geopolitical instability caused coal sector long term contracts to experience price volatility, and influenced investment decisions.

Key Takeaways:

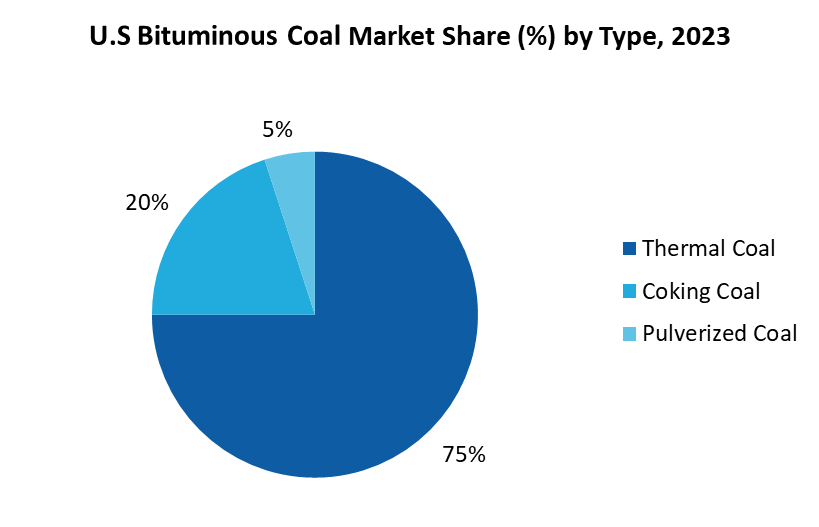

Thermal Coal is the Largest Segment

Thermal coal, or steam coal, which is widely utilized in the production of power, holds the highest share by Type in the U.S. bituminous coal market. According to the Energy Information Administration, steam coal is the most common type of coal used to produce electricity in the United States. Because of its high energy production, which is a valuable resource for thermal power plants, it is widely used in this industry. Furthermore, according to the Energy Information Administration, thermal coal accounts for an astounding 75% of the nation's coal imports, underscoring its significance in meeting the energy demands of the American market. Thermal coal is essential to sustaining the country's energy infrastructure since it is widely accessible, reasonably priced, and suitable for producing power on a big scale. Its crucial importance in the electricity industry is the primary cause of its share as the largest section by Type.

Energy and Utilities is the Largest Segment

Because of the significant reliance on coal for the production of power, the energy and utilities sector accounts for the greatest portion of the U.S. bituminous coal market. According to the American Geosciences Institute, coal continues to be essential to the US energy infrastructure, making up 17.8% of the country's overall energy mix. In 2023, 15 coal-fired power plants with a combined installed capacity of more than 20,000 megawatts (MW) in Texas alone will account for 10.8% of the state's energy generation capacity. In addition, Texas has eight operational mines that provide energy production and is the nation's second-largest producer of lignite. Despite this, coal continues to be the country's second-largest energy source for producing power, making it crucial for supplying energy demands in both regional and national markets. Because of this pervasive reliance, the energy and utilities industry in the United States is the largest user of bituminous coal.

Increasing Demand for Metallurgy Coal Drives the Market

Because metallurgical coal is essential to the manufacturing of steel worldwide, rising demand for metallurgical coal is a major factor driving the bituminous coal market in the United States. Coking coal, often referred to as metallurgical coal, is necessary to produce coke, a crucial component of blast furnaces used in the production of steel. The U.S. Energy Information Administration (EIA) estimates that in 2023, 100 million short tons of coal were shipped from the United States to at least 71 nations, with metallurgical coal making up around 51% of total exports. The market for American-made metallurgical coal is rising globally, especially in developing nations with developing infrastructure and industrial sectors. Countries relying on steel for construction, automotive, and manufacturing industries are driving this demand, positioning U.S. bituminous coal as a key export resource. As global steel production continues to rise, the need for high-quality metallurgical coal is expected to strengthen, boosting the U.S. coal market and supporting its long-term growth prospects.

Rising Energy Demand to Boost the Market

Since coal is still a vital source of dependable power generation, rising energy demand is one of the main factors driving the bituminous coal industry in the United States. U.S. electricity consumption is expected to hit record highs of 4,101 billion kWh in 2024 and 4,185 billion kWh in 2025, according to the U.S. Energy Information Administration's (EIA) September 2024 Short-Term Energy Outlook (STEO). Data centers, industrial plants, and the electrification of buildings and transportation are the main drivers of this increase. These numbers represent a significant rise above the previous high of 4,067 billion kWh in 2022 and 4,000 billion kWh in 2023. Since bituminous coal is a major fuel for power production, the market will likely continue to be supported by its strong demand even as energy dynamics change. Furthermore, bituminous coal’s place in the American energy mix is further cemented by the fact that coal-fired facilities provide a dependable backup to sporadic renewable energy sources like wind and solar, guaranteeing grid stability during times of high demand or erratic power supply.

Stringent Environment Regulations to Hamper the growth

As environmental regulations tighten and move away from coal, the U.S. bituminous coal market faces significant regulatory pressure. On April, 2024, the U.S. Environmental Protection Agency (EPA) unveiled new rules targeted at coal-fired power facilities. These include a 70 percent decrease in mercury emissions from lignite-fired sources, a reduction of more than 660 million pounds of wastewater pollutants annually, and restrictions on carbon dioxide emissions to minimize heat-trapping pollutants. Additionally, formerly uncontrolled regions now need safer management due to new, harsher coal ash disposal regulations. These initiatives aim to address environmental concerns, but they also raise operating costs for power plants and coal companies. According to the Center for Global Sustainability, the retirement of coal plants is increasing; 124 GW have been decommissioned since 2005, and a further 81 GW are anticipated to retire by 2030. Strict rules are driving coal out of the energy market and significantly reducing demand for bituminous coal produced in the United States as part of the ongoing phase-out of coal.

For more details on this report - Request for Sample

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships, and collaborations are key strategies adopted by players in the U.S Bituminous Coal Market. The top 10 companies in this industry are listed below:

- Peabody Energy Corp

- Arch Resources Inc.

- Alliance Resource Partners LP

- CONSOL Energy Inc.

- Alpha Metallurgical Resources Inc.

- Warrior Met Coal

- Navajo Transitional Energy Company

- Foresight Energy Labor LLC

- ACNR Holdings Inc.

- NACCO Industries Inc.

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

6.5% |

|

Market Size in 2030 |

478 MT |

|

Segments Covered |

By Sulfur Content, By Type and By End User Industry |

|

Key Market Players |

|

For more Chemicals and Materials Market reports, please click here

The U.S Bituminous Coal Market is projected to grow at 6.5% CAGR during the forecast period 2024-2030.

The U.S Bituminous Coal Market volume is estimated to reach 478 MT by 2030

The leading players in the U.S Bituminous Coal Market are Peabody Energy Corp, Arch Resources Inc., Alliance Resource Partners LP, CONSOL Energy Inc., Alpha Metallurgical Resources Inc. and others.

Smart elevator technologies and energy-efficient system are some of the major U.S Bituminous Coal Market trends in the industry which will create growth opportunities for the market during the forecast period.

Increasing electricity demands, rising demand for metallurgical coal, export demand, technological advancements are the driving factors of the U.S Bituminous Coal Market.