Email

Email Print

Print

Self-Injection Device Market – By Age Group , By Dosage Type , By Usability , By Route of Administration , By Type , By Application , By Distribution Channel , By Geography - Opportunity Analysis & Industry Forecast, 2024-2030

Self-Injection Device Market Overview:

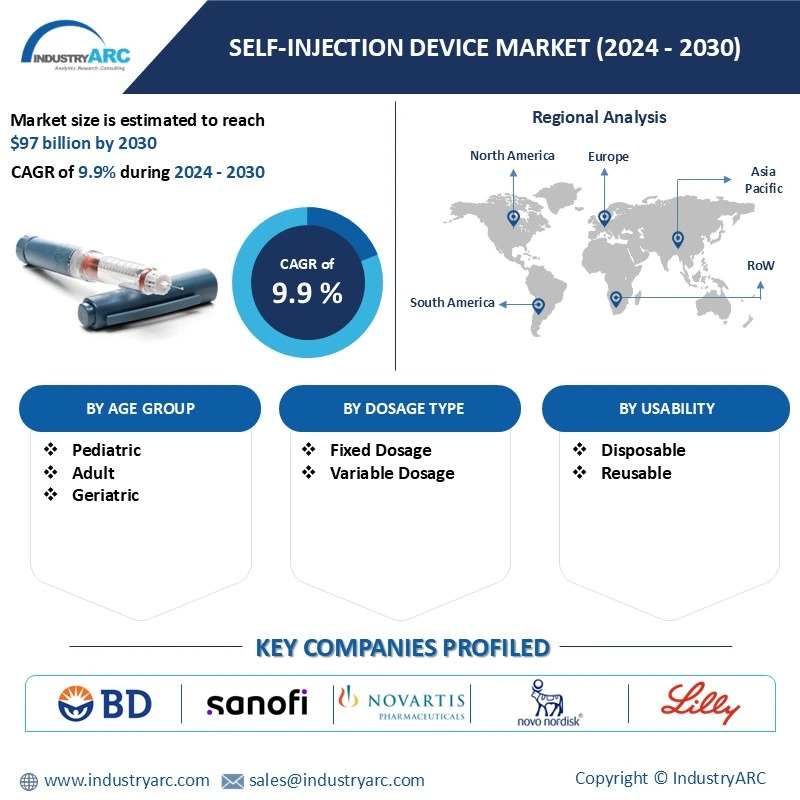

The Self-Injection Device Market size is estimated to reach $97 Billion by 2030, growing at a CAGR of 9.9% during the forecast period 2024-2030. Self-injection devices are medical instruments that let patients independently administer drugs, therefore saving the need for regular clinical visits and increasing convenience. The demand is rising due to the increasing prevalence of chronic diseases like diabetes and rheumatoid arthritis which often necessitate regular, long-term dosing. Moreover, the growth in biologic drugs, which usually require injectable delivery, fuels the market. Technological advancements in self-injection devices has made it safer, more accessible, and user friendly, such as auto injectors and needle free injectors, further driving the market. In addition, the adoption of these devices is driven by the trend towards home based care and healthcare cost saving initiatives as Self-Injection devices reduce the need for healthcare facilities, providing a cost-effective solution for patients and providers. These convenient devices also benefit the aging population that often has multiple chronic conditions and greater patient awareness and efforts to reduce needlestick injuries help to increase usage of such devices.

The rising popularity of path injectors and the shift towards home based treatment including telemedicine integration are the two major trends in the market for Self-Injection devices. Patch injectors like Luna, introduced by Luna Diabetes in October 2024, exemplify this shift. Touted as the world’s smallest automated insulin patch pump, Luna simplifies nighttime glucose management by delivering precise micro-doses of insulin. Its innovative algorithm, designed for use with insulin pens, and user-friendly onboarding process make it accessible to users of all experience levels. This trend complements the increasing adoption of home-based treatments, where telemedicine enables seamless remote monitoring and patient care. Together, these advancements address the rising demand for safe, convenient, and efficient self-administration solutions, enhancing user experience and catering to the needs of individuals managing chronic conditions at home.

Market Snapshot :

Self-Injection Device Market - Report Coverage:

The “Self-Injection Device Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Self-Injection Device Market.

| Attribute | Segment |

|---|---|

|

By Age group |

|

|

By Dosage Type |

|

|

By Usability |

|

|

By Route of Administration |

|

|

By Type |

|

|

By Application |

|

|

By Distribution Channel |

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- The market for Self-Injection devices was greatly affected by the COVID 19 pandemic as demand for home based medical treatments increased. Unlike in-clinic injections, the devices for managing chronic conditions like diabetes and autoimmune diseases became popular as patients searched for alternatives during lockdowns and social distancing. However, small shortages and delays in device manufacturing caused supply chain interruptions to adversely affect production schedules and distribution. This change accelerated the market for Self-Injection devices by driving the development of personalized medical devices and remote healthcare solutions.

- The Russia-Ukraine war added to supply chain strain already worsened by COVID-19, making raw material availability and logistics a challenge for Self-Injection devices. Higher prices for medical devices resulted from rising energy costs and economic sanctions to manufacturing costs. With inflation, demand also diminished in key European markets, as purchasing power among consumers declined as a result. Reacting to geopolitical tensions, manufacturers began to diversify supply partners and localize production in an effort to minimize costs and keep access to key components.

Key Takeaways:

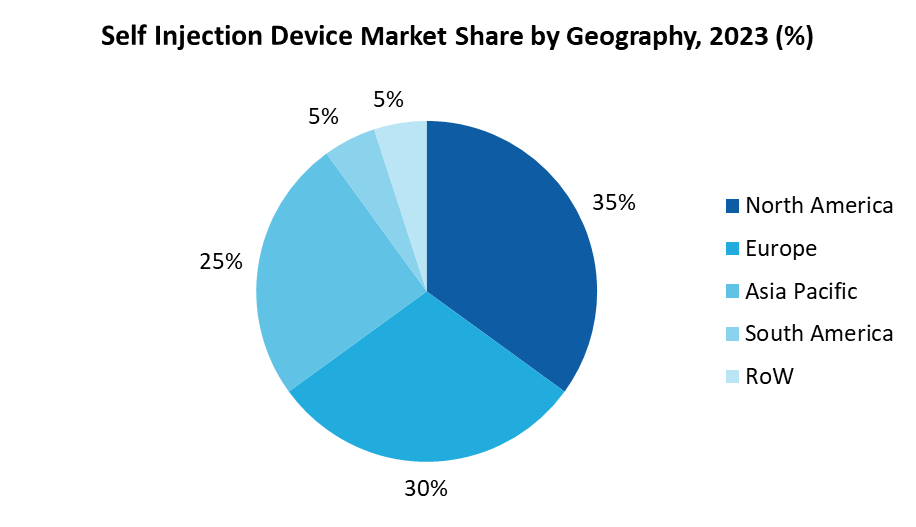

North America Leads the Market

North America leads the market for Self-Injection devices owing to its elevated rate of chronic illnesses like diabetes, which mandate at-home treatment options. The Centre of Disease Control's (CDC) 2022 National Diabetes Statistics Report states that 37.3 million Americans or 11.3 % of the U.S. population are living with diabetes, and 28.7 million have been diagnosed. In addition, 8.6 million people have diabetes but are not aware about it, and prediabetes affects 26.4 million people aged 65 and older which represents about half of the age group. Self-Injection devices are required for effective disease management and improving the patients’ quality of life for patients with chronic conditions such as diabetes, which require regular insulin injections. Additionally, North America’s well developed healthcare infrastructure, health awareness and acceptance of new medical technologies including Self-Injection systems by the population add to the regions dominance. The Self-Injection device market is also growing with the added support of favourable healthcare policies and insurance coverage, as it supports a large and diverse patient population dependent on convenient, accessible treatments.

Diabetes Dominates the Market

The high global prevalence of diabetes makes this sector the largest application segment in the Self-Injection device market. Diabetes affects millions of people around the world and continues to increase according to the International Diabetes Federation (IDF) Diabetes Atlas. By 2045, diabetes is expected to affect 783 million adults around the world, up from 537 million in 2021. An increasing age-adjusted incidence of diabetes has also been linked to a growing demand for frequent insulin injections. Patients with diabetes can manage their condition at home without having to visit the clinic frequently by using Self-Injection devices. This is only one example of how diabetes is impacting the economy; according to IDF data, $966 billion was spent on diabetes-related medical expenses in 2021. With this substantial healthcare expenditure and rising diabetes rates, diabetes is the largest segment in the Self-Injection device market due to the fact that these devices are an effective solution to regular insulin dosing for patients. Diabetes prevalence increases, and demand for Self-Injection devices is likely to continue to increase.

Auto Injectors are Leading the Market

Self-Injection devices market is dominated by auto-injectors, which are largely due to their convenience, effectiveness and ability to enhance patient safety and compliance. The National Institutes of Health (NIH) reports a high demand for epinephrine autoinjectors, with an incidence rate of 757 prescriptions per 100,000 person years and annual prescription increase of 8 % per patient. More than half (52%) of adults with severe food allergies in the United States have been prescribed an epinephrine auto-injector, highlighting its key role in emergency first response to severe allergic reactions. In the UK, for example, between 2000 and 2012, almost 24,000 children were prescribed epinephrine auto-injectors to treat life threatening conditions such as anaphylaxis. With more people relying on auto-injectors for conditions that require quick, self-administered doses, they are the preferred option in the Self-Injection device market, providing the growing demand for safe, convenient and effective treatment solutions.

Rising Prevalence of Chronic Diseases Drives the Market

The market for Self-Injection devices is growing as greater numbers of people need frequent, easy, at-home treatment owing to the rising prevalence of chronic illnesses. In accordance to the International Diabetes Federation's (IDC) Diabetes Atlas (2021), approximately 10.5% of people between the ages of 20 and 79 have diabetes, with half remaining untreated. By 2045, this number is projected to rise by 46% to 783 million people, or an eighth of the adults around the globe. Type 2 diabetes, which particularly has been triggered by socioeconomic, demographic, environmental, or genetic causes, makes up almost 90% of these cases. The requirement for Self-Injection devices continues to rise along with these chronic illnesses as they enable patients to better adhere to necessary, often lifetime therapies and control their ailments on their own. In addition, millions of citizens across the globe are affected by long-term diseases like multiple sclerosis, leading to higher the requirement for Self-Injection devices for other chronic ailments. These devices have become essential for the safe and independent administration of a variety of medications. The observed trend illustrates the growing acceptance of Self-Injection pharmaceuticals in the treatment of chronic diseases.

Regulatory Compliance to Hamper the Market

Regulatory compliance is a significant challenge in the self-injection device market due to stringent requirements and the complexities involved in ensuring patient safety. Unlike traditional injectable pharmaceuticals administered by healthcare professionals, self-injection devices must meet strict standards to allow safe and effective use by patients or caregivers in non-clinical settings. For example, auto-injectors are designed to simplify the injection process by incorporating features such as spring-loaded actuators and needle shields. These devices must comply with ISO 11608-5:2022, which outlines key performance tests for functions like cap removal force, activation force, injection time, dose accuracy, and needle length. Failure to meet these specifications could lead to delays in treatment, medication errors, or harm to patients. Additionally, devices must undergo pre-conditioning and stability testing to demonstrate robustness under various storage and transportation conditions. The detailed testing protocols and performance benchmarks add layers of complexity for manufacturers, making regulatory compliance a critical but challenging aspect of the market.

For more details on this report - Request for Sample

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships, and collaborations are key strategies adopted by players in the Self-Injection Device Market. The top 10 companies in this industry are listed below:

- BD (Becton, Dickinson and Company)

- Sanofi

- Novartis AG

- Novo Nordisk A/S

- Eli Lilly and Company

- Owen Mumford Ltd.

- Pfizer Inc.

- Biocorp Production SA

- Ypsomed Holding AG

- Gerresheimer AG

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

9.9% |

|

Market Size in 2030 |

$97 Billion |

|

Segments Covered |

By Age Group, By Dosage Type, By Usability, By Route of Administration, By Type, By Application, By Distribution Channel and By Geography. |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Russia and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

|

For more Lifesciences and Healthcare Market reports, please click here

LIST OF TABLES

1.Global Self-injection Devices Market Analysis and Forecasts, by Product Market 2023-2030 ($M)

1.1 Pen Injectors Market 2023-2030 ($M) - Global Industry Research

1.2 Autoinjectors Market 2023-2030 ($M) - Global Industry Research

1.3 Wearable Injectors Market 2023-2030 ($M) - Global Industry Research

2.Global Self-injection Devices Market Analysis and Forecasts, by Usage Market 2023-2030 ($M)

3.Global Competition Landscape Market 2023-2030 ($M)

4.Global Self-injection Devices Market Analysis and Forecasts, by Product Market 2023-2030 (Volume/Units)

4.1 Pen Injectors Market 2023-2030 (Volume/Units) - Global Industry Research

4.2 Autoinjectors Market 2023-2030 (Volume/Units) - Global Industry Research

4.3 Wearable Injectors Market 2023-2030 (Volume/Units) - Global Industry Research

5.Global Self-injection Devices Market Analysis and Forecasts, by Usage Market 2023-2030 (Volume/Units)

6.Global Competition Landscape Market 2023-2030 (Volume/Units)

7.North America Self-injection Devices Market Analysis and Forecasts, by Product Market 2023-2030 ($M)

7.1 Pen Injectors Market 2023-2030 ($M) - Regional Industry Research

7.2 Autoinjectors Market 2023-2030 ($M) - Regional Industry Research

7.3 Wearable Injectors Market 2023-2030 ($M) - Regional Industry Research

8.North America Self-injection Devices Market Analysis and Forecasts, by Usage Market 2023-2030 ($M)

9.North America Competition Landscape Market 2023-2030 ($M)

10.South America Self-injection Devices Market Analysis and Forecasts, by Product Market 2023-2030 ($M)

10.1 Pen Injectors Market 2023-2030 ($M) - Regional Industry Research

10.2 Autoinjectors Market 2023-2030 ($M) - Regional Industry Research

10.3 Wearable Injectors Market 2023-2030 ($M) - Regional Industry Research

11.South America Self-injection Devices Market Analysis and Forecasts, by Usage Market 2023-2030 ($M)

12.South America Competition Landscape Market 2023-2030 ($M)

13.Europe Self-injection Devices Market Analysis and Forecasts, by Product Market 2023-2030 ($M)

13.1 Pen Injectors Market 2023-2030 ($M) - Regional Industry Research

13.2 Autoinjectors Market 2023-2030 ($M) - Regional Industry Research

13.3 Wearable Injectors Market 2023-2030 ($M) - Regional Industry Research

14.Europe Self-injection Devices Market Analysis and Forecasts, by Usage Market 2023-2030 ($M)

15.Europe Competition Landscape Market 2023-2030 ($M)

16.APAC Self-injection Devices Market Analysis and Forecasts, by Product Market 2023-2030 ($M)

16.1 Pen Injectors Market 2023-2030 ($M) - Regional Industry Research

16.2 Autoinjectors Market 2023-2030 ($M) - Regional Industry Research

16.3 Wearable Injectors Market 2023-2030 ($M) - Regional Industry Research

17.APAC Self-injection Devices Market Analysis and Forecasts, by Usage Market 2023-2030 ($M)

18.APAC Competition Landscape Market 2023-2030 ($M)

19.MENA Self-injection Devices Market Analysis and Forecasts, by Product Market 2023-2030 ($M)

19.1 Pen Injectors Market 2023-2030 ($M) - Regional Industry Research

19.2 Autoinjectors Market 2023-2030 ($M) - Regional Industry Research

19.3 Wearable Injectors Market 2023-2030 ($M) - Regional Industry Research

20.MENA Self-injection Devices Market Analysis and Forecasts, by Usage Market 2023-2030 ($M)

21.MENA Competition Landscape Market 2023-2030 ($M)

LIST OF FIGURES

1.US Self-injection Device Market Revenue, 2023-2030 ($M)

2.Canada Self-injection Device Market Revenue, 2023-2030 ($M)

3.Mexico Self-injection Device Market Revenue, 2023-2030 ($M)

4.Brazil Self-injection Device Market Revenue, 2023-2030 ($M)

5.Argentina Self-injection Device Market Revenue, 2023-2030 ($M)

6.Peru Self-injection Device Market Revenue, 2023-2030 ($M)

7.Colombia Self-injection Device Market Revenue, 2023-2030 ($M)

8.Chile Self-injection Device Market Revenue, 2023-2030 ($M)

9.Rest of South America Self-injection Device Market Revenue, 2023-2030 ($M)

10.UK Self-injection Device Market Revenue, 2023-2030 ($M)

11.Germany Self-injection Device Market Revenue, 2023-2030 ($M)

12.France Self-injection Device Market Revenue, 2023-2030 ($M)

13.Italy Self-injection Device Market Revenue, 2023-2030 ($M)

14.Spain Self-injection Device Market Revenue, 2023-2030 ($M)

15.Rest of Europe Self-injection Device Market Revenue, 2023-2030 ($M)

16.China Self-injection Device Market Revenue, 2023-2030 ($M)

17.India Self-injection Device Market Revenue, 2023-2030 ($M)

18.Japan Self-injection Device Market Revenue, 2023-2030 ($M)

19.South Korea Self-injection Device Market Revenue, 2023-2030 ($M)

20.South Africa Self-injection Device Market Revenue, 2023-2030 ($M)

21.North America Self-injection Device By Application

22.South America Self-injection Device By Application

23.Europe Self-injection Device By Application

24.APAC Self-injection Device By Application

25.MENA Self-injection Device By Application

The Self-Injection Device Market is projected to grow at 9.9% CAGR during the forecast period 2024-2030.

The Self-Injection Device Market size is estimated to be $50.1 Billion in 2023 and is projected to reach $97 Billion by 2030

The leading players in the Self-Injection Device Market are Self-Injection Device Market are BD (Becton, Dickinson and Company), Sanofi, Novartis AG, Novo Nordisk A/S, Eli Lilly and Company and Others.

Rising importance of biologic medications and the shift towards home based treatment are some of the major Self-Injection Device Market trends in the industry which will create growth opportunities for the market during the forecast period.

Rising prevalence of chronic diseases, patient preference for home-based care, growth of biologic drugs, advancements in device technology, increasing awareness and education, government initiatives and healthcare cost savings, rising geriatric population and focus on minimizing needlestick injuries are the driving factors of the Self-Injection Device market.