Email

Email Print

Print

Rigid Polyurethane Foams Market- Industry Analysis, Market Size, Share, Trends, Growth And Forecast 2024 - 2030

Rigid Polyurethane Foams Market Overview

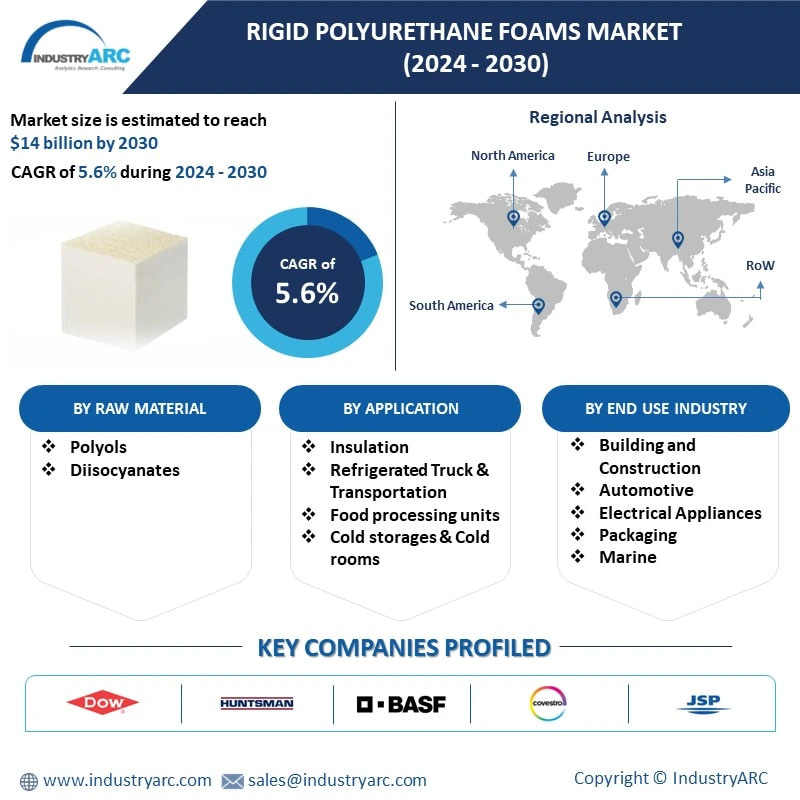

Rigid Polyurethane Foams Market is forecast to reach $14 billion by 2030, after growing at a CAGR of 5.6% during 2024-2030. The growth of the market is driven by the increasing use of rigid polyurethane foam for insulation and energy saving in the building & construction and appliance industries and weight reduction in the automotive industry. Increasing demand for bio-polyols to prepare open cellular structure semi-rigid polyurethane foams for applications in the construction industry is also driving the market demand. Furthermore, due to the lightweight and durability, rigid polyurethane foams are also increasingly used in the laminated insulation panels and packaging industry that is driving new opportunities for the growth of the global rigid polyurethane foams industry in the forecast era.

One prominent trend revolves around sustainability. With a growing awareness of environmental concerns, there's a significant push towards eco-friendly alternatives within the rigid polyurethane foam market. Manufacturers are increasingly focusing on developing formulations that reduce the carbon footprint, incorporating bio-based or recycled materials into foam production. This trend is fueled by both regulatory pressures and consumer demand for greener products. Companies are investing in research and innovation to create foam solutions that maintain performance while minimizing environmental impact, thereby driving the market towards more sustainable practices.

Another key trend centers on improving insulation performance. As energy efficiency becomes a priority across various industries, there's a continuous demand for rigid polyurethane foams with enhanced insulation capabilities. Advancements in foam formulations and manufacturing processes are geared towards achieving higher R-values, better thermal resistance, and improved fire-retardant properties. These developments cater to diverse applications such as construction, refrigeration, and automotive industries, where superior insulation is crucial. The emphasis on boosting insulation performance reflects the market's response to stringent energy efficiency standards and the pursuit of more effective insulation solutions.

Market Snapshot:

Rigid Polyurethane Foams Market Report Coverage

The: “Rigid Polyurethane Foams Market Report – Forecast (2024-2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the rigid polyurethane foams market.

By Raw Material: Polyols and Diisocyanates.

By Application: Insulation, Refrigerated Truck & Transportation, Food processing units, Cold storages & Cold rooms, and Others.

By End Use Industry: Building and Construction, Automotive, Electrical Appliances, Packaging, Marine, Healthcare Industry, Oil & Gas, and Others.

By Geography: North America (U.S, Canada, and Mexico), Europe (U.K., Germany, Italy, France, Spain, Netherlands, Russia, Belgium, and Rest of Europe), APAC (China, Japan, India, South Korea, Australia, Taiwan, Indonesia, Malaysia, and Rest of Asia Pacific), South America(Brazil, Argentina, Colombia, Chile, and Rest of South America), and RoW (Middle East and Africa).

Key Takeaways

- Asia-Pacific region dominated the rigid polyurethane foams market due to the increasing use of open cellular structure polyurethanes in the building and construction activities in countries such as Japan, China, and South Korea.

- Also, the growing understanding of the principle of green construction and the development of bio-based polyols are projected to give substantial prospects towards the growth of the rigid polyurethane foams market.

- Government funding for the use of rigid polyurethane foams in refrigeration applications is anticipated to fuel the consumer demand for rigid polyurethane foams over the forecast period.

Rigid Polyurethane Foams Segment Analysis - By Raw Material

Polyol is a widely used raw material in the rigid polyurethane foams market. The vast array of isocyanate-reacting polyols contributes to a wide variety of polyurethane fabrics, which range from cushioning and insulation to coatings, garments, and electronics. Polyether polyols are additives used mainly by the polyurethane industry to manufacture products such as lightweight and molded foam parts for mattresses, bedding, and upholstered furniture. While highly branched polyols produce solid PU with good heat and resistance to chemicals, less branched polyols offer polyurethane with good flexibility (at low temperature) and low chemical resistance. Low-MW polyols likewise produce rigid polyurethane, and long-chain high-MW polyols produce flexible PU products.

Rigid Polyurethane Foams Segment Analysis - By Application

Insulation held the largest share in the rigid polyurethane foams market with 24% in the year 2023. Rigid polyurethane foams are the most reliable insulation materials used for roof and wall insulation, sealed windows and doors, and air barrier sealants. Installers use rigid polyurethane foam to insulate door entrances and garage doors, where the method can be constant or discontinuous. Entry doors with a rigid polyurethane foam core help to inhibit sound and provide insulation benefits that further decrease heating and cooling energy needs. And for appliances, rigid polyurethane foams are used to insulate ice machines and drinking machines, water heaters, among other applications. Also, the rising demand for laminated insulation panels has raised the growth of the market. Thus, with the growing demand for rigid polyurethane foams for insulation applications, the market is anticipated to rise in the forecast period.

Rigid Polyurethane Foams Segment Analysis - By End Use Industry

Building and Construction held the largest share in the rigid polyurethane foams market in 2023 and are projected to grow at a CAGR of 5.5% during the forecast period 2024-2030. To minimize heat flow between the interior of the building and the exterior environment, rigid foams are used. They contribute greatly towards reducing the impact of thermal bridges and efficiently insulating the interior of the house. Additionally, the rising use of laminated insulation panels owing to the excellent dimensional stability and compressive strength in building and construction activities has raised the demand for polyurethane foams. Expanded polystyrene (EPS), extruded polystyrene (XPS), and polyisocyanurate are the most popular rigid foams used as thermal insulators for building and construction uses. Therefore, the increasing use of rigid polyurethane foams in various building and construction activities is expected to drive the growth of the market in the forecast period.

Rigid Polyurethane Foams Segment Analysis - By Geography

The Asia Pacific region held the largest share with 42% in the rigid polyurethane foams market in 2023. Globally, the Asia Pacific region dominates the demand for rigid polyurethane foams market due to growing building and construction activities from different countries. According to the United States Department of Energy, rigid polyurethane foam can save money by keeping a steady temperature with heating and cooling costs equivalent to 56 percent of the electricity used in the typical American home. The rising disposable income and consumer urbanization in Asia have seen a substantial rise in the construction sectors. China is the leading construction market in the world. Thus, the demand for the rigid polyurethane foams market is therefore anticipated to increase in the APAC region over the forecast period.

For more details on this report - Request for Sample

Rigid Polyurethane Foams Market Drivers

Development of Eco-Friendly Rigid Foams

Chlorofluorocarbons (CFCs) and HFCs are responsible for the ozone depletion and global warming of rigid foam insulators. Cellulose rigid foam insulation boards are environmentally friendly choices for rigid Styrofoam and have begun to gain momentum in the rigid foam industry. The cellulose rigid foam insulation boards, recently formulated for use are manufactured from water-based solvents and contain no toxic GHG blowing agents that contribute to ozone depletion and global warming. The growing value of eco-friendly rigid foams in the building and construction industry is expected to sway house builders to renewable and ecological foams like rigid cellulose foam isolation boards and rigid bio-composite foam. Thus, with an increasing demand for eco-friendly rigid foam, the market demand for rigid polyurethane foams is anticipated to rise over the forecast period.

Growing Demand for Rigid Foam in the Automotive Industry

Polyurethanes are commonly used in vehicle production, providing real comfort, safety, and energy-saving benefits. Rigid polyurethane foams can be found in armrests, and headrests, where their coating properties help to reduce driving fatigue and stress. Durability and lightweight, coupled with the efficiency, rigid polyurethane foams suitable for car bodies where they protect against heat and noise in the engine with their insulation characteristics. Since rigid polyurethanes are strong and light, these polyurethanes are used to minimize automotive weight and increase fuel economy and environmental performance. Also, for automotive seat cushion construction, open cellular structure polyurethane (PUR) foam has become the preferred material. As compared to more conventional steel spring seat support systems, it offers a significantly lower weight/performance ratio. Thus, the rising demand for rigid polyurethane foams in the automotive industry will raise the market demand in the projected period.

Rigid Polyurethane Foams Market Challenges

Volatility in Crude Oil Prices

Rigid SPFs are mainly synthesized from petroleum-derived feedstocks such as MDI and TDI. These compounds are derived from benzene, a crude oil derivative. The demand for crude oil is highly concentrated and oligopolistic. The supply of crude oil has also been a crucial factor in restricting demand expansion. Owing to the supply-demand divide, there has been an oscillation of crude oil markets. This has resulted in price volatility for its derivatives. Factors include political unrest in the Middle East region and the embargo on Iran has contributed to a slowdown in the production of crude oil that has impacted petrochemical prices. As a result, the price instability of raw materials has been a key factor hindering the demand growth of the rigid polyurethane foams market.

Rigid Polyurethane Foams Market Landscape

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in the rigid polyurethane foams market. Major players in the rigid polyurethane foams market are The Dow Chemical Company, Huntsman Corporation, BASF SE, Covestro AG, JSP Corporation, Sealed Air Corporation, Armacell International S.A, Zotefoams Plc, Woodbridge Foam Corporation, and Borealis AG among others.

Developments

Between 2022 and 2023, ongoing research and development aimed at enhancing the properties of rigid polyurethane foams were notable. Innovations in formulation techniques, such as the incorporation of nanoparticles or the use of novel catalysts, were being explored to improve foam insulation properties, fire resistance, and overall performance.

For more Chemicals and materils related reports, please click here