Email

Email Print

Print

Offshore Wind Energy Market - By Component , By Water Depth , By Installation , By Capacity , By Application | Industry Trend & Forecast 2024 - 2030

Offshore Wind Energy Market Overview:

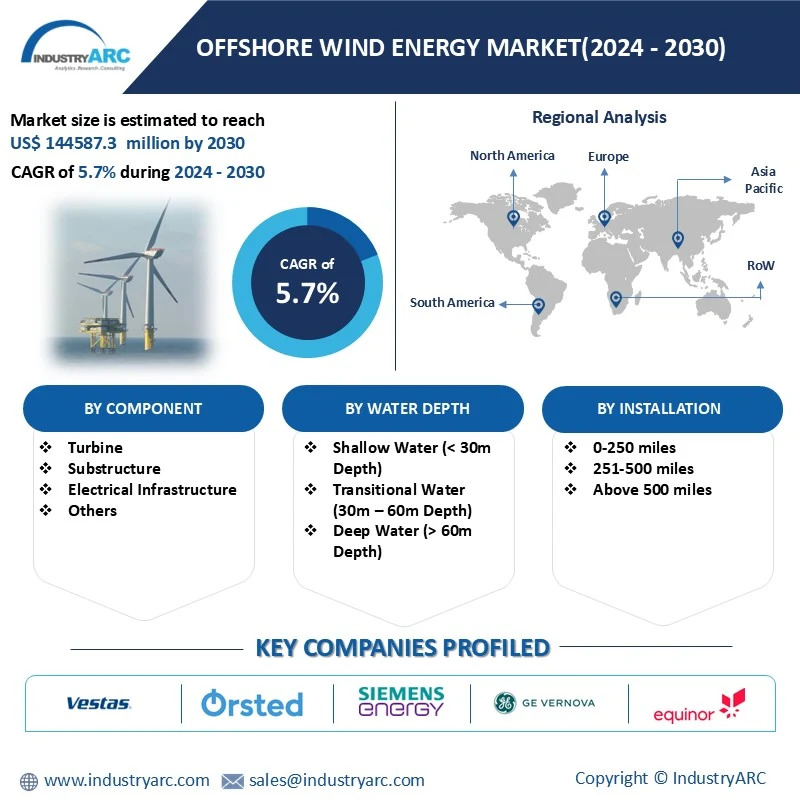

Offshore Wind Energy Market Size is forecast to reach $ 144587.3 Million by 2030, at a CAGR of 5.7%during forecast period 2024-2030.Offshore wind farms generate electricity from wind blowing across the sea. They are considered more efficient than onshore wind farms owing to the higher speed of seawinds, greater consistency and lack of physical interference that land or human-made objects can present, as per National Grid. The global offshore wind energy market is experiencing robust growth due to several factors. A significant driver is the global transition towards renewable energy sources to address climate change and reduce dependence on fossil fuels. Supportive government policies including feed-in tariffs, tax incentives and streamlined permitting processes are further accelerating market expansion. Technological advancements such as improvements in turbine design, foundation structures and installation techniques and the increasing integration of offshore wind into the broader energy grid. Due to these characteristics, the market for offshore wind energy is expected to increase steadily over the next several years. One of the major trends in offshore wind energy is larger turbine sizes. In order to capture the abundant wind resources available offshore turbine manufacturers are continuously developing larger and more powerful turbines. For instance, in 2023, Siemens Gamesa unveiled its SG 14-236 DD offshore wind turbine, one of the world's most powerful wind turbines. A 236-meter rotor with blades based on the trusted Integral Blade technology enables the SG 14-236 DD to produce more than 30% AEP compared to the SG 11.0-200 DD. It is recommended for high-wind and low-wind markets and offshore locations. Larger turbines produce greater amounts of energy, meaning that fewer turbines are needed to generate the same amount of electricity, leading to lower costs. Another trend is floating offshore wind. Floating offshore wind is key to transitioning dense population centers to clean energy. According to U. S. Department of Energy, the floating offshore wind energy shot aims to dramatically reduce the cost of floating offshore wind energy, targeting a cost of $45 per megawatt-hour for deep-water sites by 2035. This ambitious goal represents a 70% reduction in costs.

Market Snapshot :

Offshore Wind Energy Market - Report Coverage:

The “Offshore Wind Energy Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Offshore Wind Energy

| Attribute | Segment |

|---|---|

|

|

|

By Water Depth |

|

|

By Installation |

|

|

By Capacity

|

|

|

By Application

|

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- The COVID-19 pandemic significantly disrupted global supply chains, including those for the offshore wind energy sector. This led to shortages of critical components like turbine blades, towers and electrical systems impacting project timelines and increasing costs.

- The Russia-Ukraine war has disrupted global supply chains leading to increased costs and delays in offshore wind projects. To mitigate these risks, countries are focusing on localizing supply chains to reduce reliance on critical imports. Additionally, the war led to renewed interest in offshore wind farms to move away from Russia oil & gas.

Key Takeaways:

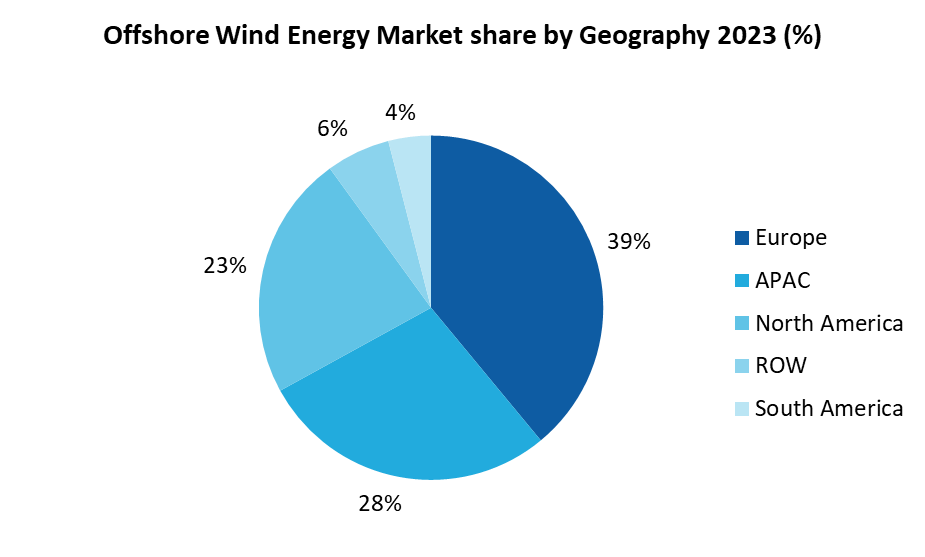

Europe dominates the market

Europe dominates the market with a market share of 39% for offshore wind energy market. Europe is the leader in offshore wind and is home for the largest operational wind farms for both bottom fixed and floating foundation technologies. Europe’s offshore capacity is sufficiently large enough to supply the electricity demand in Europe which will only continue to grow within the upcoming years. According to Wind Europe, Europe installed a record 18.3 GW of new wind power capacity in 2023. However, this is still short of the 29 GW annual target needed to meet the EU's 2030 climate and energy goals. To achieve its 42.5% renewable energy target, the EU needs to install 33 GW per year on average. In November 2024, Hitachi Energy was selected to supply critical grid connection and power quality solutions for the East Anglia TWO (EA TWO) wind farm, an offshore renewable energy project spearheaded by ScottishPower Renewables, a subsidiary of the Iberdrola Group. The EA TWO project, located 32 kilometers off the Suffolk coast in England, aims to generate 960 megawatts (MW) of renewable energy, providing green electricity for nearly one million homes. This development is a significant step towards achieving the UK’s 2030 energy targets. Therefore, due to its growing renewable energy adoption, robust policy framework and presence of major players Europe is positioned to lead the world in the offshore wind energy market.

Fixed structure dominates the market

Fixed structure dominates the offshore wind energy market. Fixed offshore wind turbines are fixed in a permanent static position because, as their name implies, they are directly and rigidly connected to the seabed. These constructions are made up of big wind turbines that are usually placed under water up to 60 metres deep and supported by monopile, jacket or gravity-based foundations. In Europe, where the sector has quickly developed, fixed turbines are commonly used. The stability of fixed offshore wind turbines is one of their main benefits. These turbines can tolerate severe weather conditions including as strong winds and choppy waves because of their solid static construction which is provided by their direct attachment to the bottom. Because fixed turbines are positioned permanently, they are comparatively easy to construct and maintain, this factor enables consistent power generation by lowering maintenance costs and reliability.

3-5 MW Turbine Segment Dominates the Market

The 3-5 MW turbine segment continues to dominate the offshore wind energy market. Turbines in the 3-5 MW range offer a strong balance between power output and cost-effectiveness. They are capable of generating significant amounts of clean energy while remaining financially viable. This segment benefits from well-established technology and proven performance, reducing risks associated with newer, larger turbines. Mature technologies and experienced manufacturers contribute to the reliability and efficiency of these turbines. Their versatility allows for deployment in various environmental conditions and project sizes, making them suitable for a wide range of offshore wind projects, especially in shallower waters. Therefore, the 3-5 MW segment is expected to remain a significant contributor to the growth of the offshore wind energy market for the foreseeable future.

Global Shift towards Renewable Energy Drives the Market

One of the primary drivers promoting the offshore wind energy market is the global transition to renewable energy. Offshore wind energy has become an attractive choice as nations attempt to reduce greenhouse gas emissions and reduce the effects of climate change. According to International Energy Agency, at COP28, nearly 200 countries pledged to triple the world’s renewable power capacity this decade, which is one of the critical actions to keep alive hopes of limiting global warming to 1.5 °C. However, a new country-by-country analysis reveals nearly 150 countries reveals far more ambitious domestic renewable energy targets, totaling nearly 8,000 GW of global installed capacity by 2030. With the global adoption of renewable energy, offshore wind is ideally positioned to contribute significantly to the energy balance. In the years to come, offshore wind is expected to continue growing quickly due to its enormous potential and environmental advantages.

High initial capital costs to hamper the market

One of the primary challenges facing the offshore wind industry is the significant upfront capital costs associated with project development and installation. Offshore wind farms require extensive infrastructure, including turbines, foundations, subsea cables and offshore substations. The construction and installation of these components are highly specialized and capital-intensive. Specialized vessels and equipment are needed for transportation, installation and maintenance of offshore wind turbines. The procurement and operation of these specialized assets can be costly. To mitigate these high upfront costs, various strategies are being employed, including economies of scale, technological advancements, and government support. As the industry matures and technology improves, it is expected that the cost of offshore wind energy will continue to decline, making it increasingly competitive with traditional energy sources.

For more details on this report - Request for Sample

Key Market Players:

The top 10 companies in this industry are listed below:

- Vestas Wind Systems A/S

- Ørsted A/S

- Siemens Energy

- GE Vernova

- Equinor ASA

- Nordex SE

- Vattenfall AB

- Sinovel Wind Group Co Ltd

- Suzlon Group

- China Ming Yang Wind Power Group Limited

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

13.6% |

|

Market Size in 2030 |

$61.6 Billion |

|

Segments Covered |

By Component, By Water Depth, By Installation, By Installation, By Capacity, By Application, By Geography |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Denmark, Netherlands and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Thailand and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

|

For more Energy and Power Market reports, please click here

The Offshore Wind Energy Market is projected to grow at 13.6% CAGR during the forecast period 2024-2030.

The Offshore Wind Energy Market size is estimated to be $25.2 billion in 2023 and is projected to reach $61.6 billion by 2030.

Vestas Wind Systems A/S, Ørsted A/S, Siemens Energy, GE Vernova, Equinor ASA and others.

Larger turbine sizes and floating offshore wind are the major trends that will shape the market in the future.

The global offshore wind energy market is booming, driven by the global shift to renewable energy, supportive government policies, and technological advancements.