Email

Email Print

Print

Industrial Silica Sand Market- Industry Analysis, Market - Forecast(2025 - 2031)

Industrial Silica Sand Market Overview

Industrial Silica Sand Market is forecast to reach US$29.78 billion by 2030, after growing at a CAGR of 5% during 2024-2030. The Industrial Silica Sand Market refers to the global trade and consumption of silica sand, a granular material composed of finely divided quartz and other minerals. Silica sand is primarily used in various industrial applications, including glassmaking, foundry casting, construction, abrasives, ceramics, filtration, and hydraulic fracturing (fracking) in the oil and gas industry. It is valued for its high purity, strength, and chemical inertness. The Industrial Silica Sand Market is influenced by rising demand from the glass manufacturing industry. Silica sand provides the essential silicon dioxide required for glass formulation; hence it is the primary component in all standards and specialty glass. Moreover, rising demand from the glass and foundry sectors is a pivotal driver for market growth. These industries require silica sand for various applications, including glass production and metal casting. As demand surges, the Industrial Silica Sand Market experiences significant momentum, fueled by the essential role it plays in meeting the needs of these vital sectors. For instance, according to the UK Department for Business and Trade, The UK government aims to boost annual research and development investment to $27.87 billion by 2024-25, while top food manufacturers collectively spend $1140.02 million yearly. In addition, the German government and top automakers reaffirm the aim for 15 million electric vehicles on German roads by 2030, emphasizing a commitment to sustainable transportation. Such initiatives and investments are driving the demand for the glass thereby contributing to the market growth rate.

Market Snapshot :

Industrial Silica Sand Market Report Coverage

The report: “Industrial Silica Sand Market– Forecast (2024-2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the Silica Sand Industry.

By Purity: 94% to 95.9%, 96% to 97.9%, 98% to 98.9%, and Above 99%.

By Silica Sand: Wet Sand, Dry Sand, Frac Sand, Filter Sand, Coated Sand, and others.

By Application: Glass Manufacturing (Flat Glass, Fiberglass Insulation, Specialty Glass, Container Glass & Others), Chemical Production (Sodium Silicate, Silicon Gels, Silicon Tetrachloride & Others), Foundry (Ferrous Foundry, Nonferrous Foundry), Construction (Cement, Asphalt Mixtures, Mortar & Others), Paints & Coatings (Architectural Paints & Coatings, Industrial Paints & Coatings), Ceramics & Refractories (Tableware, Sanitaryware, Floor and Wall Tiles), Filtration and Water Production (Drinking Water, Wastewater), Oil & Gas Recovery and others.

By Geography: North America (USA., Mexico, and Canada), Europe (U.K, Germany, Italy, France, Netherlands, Belgium, Russia, Spain, and Rest of Europe), APAC (China, South Korea, Japan, India, Australia & New Zealand, Indonesia, Taiwan, Malaysia Rest of APAC), South America (Brazil, Argentina, Colombia, Chile, Rest of South America) and RoW (Middle East (Saudi Arabia, U.A.E, Israel, Rest of the Middle East), Africa (South Africa, Nigeria, Rest of Africa)).

Key Takeaways

- North America, dominates the global Industrial Silica Sand Market, owing to increased construction activities and various government initiatives such as the U.S. General Services Administration (GSA), which allocated $2 billion for over 150 construction projects nationwide, promoting low-embodied carbon (LEC) materials under the Biden-Harris Administration's Investing in America agenda. This initiative supports job creation, addresses climate change, and boosts the market for cleaner construction materials like asphalt, concrete, glass, and steel in 2023.

- The significant growth in the construction sector is contributing to the demand for silica sand. The European Construction Sector plan involves a EUR 165.0 billion investment until 2030 in housing and transport infrastructure, including additional funds for cross-border projects as per the European Commission.

- Although COVID-19 has significantly resulted in the pause of production capacity in the manufacturing industries, resulting in the decline of the Economy, the market is set to recover with the vaccine rollout in various countries.

For more details on this report - Request for Sample

Industrial Silica Sand Market Segment Analysis – By Purity

Above 99% purity held the largest share in the Industrial Silica Sand Market in 2023 and is forecasted to grow at a CAGR of 5.4% during the forecast period. Silica sand with a purity of 99.5% is used in the glass industry. Commercial glass is made by fusing silica sand (Si02), limestone (CaC03), and soda ash (NC03) at 1,100°C. The typical composition is 75% silica, 10% lime, and 15% soda ash. The sand should be uniform in grain size and contain at least 99.5% silica. The reduction of impurities in silica sand to a degree appropriate for the manufacture of acceptable solar-grade silicon for photovoltaic applications using photothermal treatment. This method attracts impurities to the surface of silica grains, where they can be easily removed by dissolving them partially in an acid mixture. The inductively coupled plasma atomic emission spectrometry (ICP– AES) method was used to analyze the silica collected. Al, K, Fe, Na, Ca, Mg, and B were the most common impurities found in silica sand. Almost all significant impurities were effectively eliminated in the new goods. Indeed, according to ICP–AES characterization, the purity degree ranges from 99.76 to 99.96%, with an average impurity removal efficiency of 83.33%.

Industrial Silica Sand Market Segment Analysis – By Silica Sand

Wet silica dominated the Industrial Silica Sand Market in 2023 and is expected to grow at a CAGR of 5.4% during the forecast period. Wet Silica Sand is used as a high-quality sand source for the glass industry because of its high silica content (SiO2). Wet silica sand is primarily used in construction, the glass industry, golf courses, and other applications. Because of the constant demand in the construction industry, wet silica sand with specific grain dimensions and composition characteristics is an excellent option for destination markets. In addition, the sand created by wet silica sand has the properties listed for golf course construction and maintenance. Wet silica sand of this kind has long been used on the best golf courses in and around the Portuguese and Spanish peninsulas. It's used on the green, tee, bunkers, and access paths, among other places.

Industrial Silica Sand Market Segment Analysis – By Application

Glass manufacturing application dominated the Industrial Silica Sand Market in 2020 and is poised to grow at a CAGR of 4.7% during the forecast period. According to National Institute Sand Association (NISA), the production of glass requires a variety of different commodities, silica represents over 70% of its final weight. Flat glass, fiberglass insulation, specialty glass, container glass and others are considered under this segment. Flat glass is widely used in automotive and construction applications, container glass is used in food and beverages and tableware applications and so on. The significant growth in the investments and expansions with the growing demand from these sectors is set to boost the market growth rate during the forecast period 2024-2030.

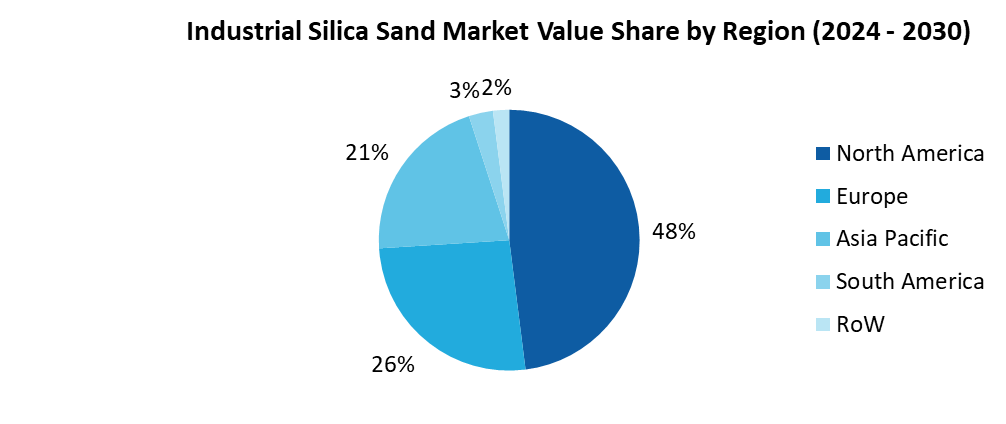

Industrial Silica Sand Market Segment Analysis – By Geography

North America dominated the Industrial Silica Sand Market with a share of approximately 48% in 2023 and is anticipated to grow at a CAGR of 6.3% through the forecast period. Silica sand is the main component in various chemicals such as sodium silicate, silicon tetrachloride, and silicon gels. These chemicals are majorly used in the production of a wide range of materials from household to industrial cleaners, fiber optics, and to remove impurities from cooking oil and brewed beverages. Adding to this, the growing investments and expansions in the fiber optic manufacturing sector with rising demand from the 5G rollout are set to escalate the market growth rate. For instance, The Biden-Harris Administration launches the $1.5 billion Public Wireless Supply Chain Innovation Fund, investing in open and interoperable networks to boost wireless innovation, competition, and supply chain resilience. This initiative aims to strengthen U.S. leadership in 5G and next-gen wireless technology. This marks a significant leap forward in connectivity, promising transformative opportunities for diverse sectors. Furthermore, The American Public Transportation Association (APTA), In 2022, heavy rail, light rail, and commuter rail collectively constituted 46% of all transit trips, aligning with historical trends. Remarkably, heavy rail saw a 36.55% increase, light rail experienced a 37.85% rise, and commuter rail achieved a substantial 51.82% increase in ridership over the year. Furthermore, in 2022, The Biden-Harris Administration allocates $660 million for states to address orphaned oil and gas wells, fostering economic growth and environmental protection. This funding, part of the bipartisan Infrastructure Law, this will further complement Industrial Silica Sand Market growth.

Industrial Silica Sand Market Drivers

Construction is on the Rise as a Result of Consistent Economic Growth

Silica sand is the primary structural component in a wide variety of building and construction products. Silica sand is used in flooring compounds, mortars, specialty cement, stucco, roofing shingles, skid-resistant surfaces, and asphalt mixtures for binding. Moreover, ground silica performs ads durability and anti-corrosion and weathering properties in epoxy-based compounds, sealants, and caulks. The significant growth in initiatives such as smart cities in countries such as India, the US, and so on is set to boost the demand for silica sand. In February 2023, the Indian government allocated approximately $2.67 billion (USD) to metro projects nationwide in the Union Budget 2023-24. This includes equity investment of $645 million, subordinate debt of $191 million, and pass-through assistance of $1.82 billion, is further expected to boost business growth. Furthermore, the United States is seeing significant investment in residential development, which is projected to continue shortly. According to the US Census Bureau, the Construction spending in December 2023 reached a seasonally adjusted annual rate of $2,096.0 billion, up 0.9% from November and 13.9% from December 2022. The total construction value for 2023 was $1,978.7 billion, a 7.0% increase from 2022's $1,848.7 billion. Mexico is also experiencing high housing demand, which has resulted in significant construction expenditure. For example, the Inter-American Development Bank (IDB) granted the Mexican company Procsa a local currency financing program worth up to 150 million Mexican pesos ($7.8 million) in January 2019 to fund land acquisition, development, and commercialization of housing for low- and middle-income families in the country. The construction market is expected to be driven by rapid growth in investments in renewable power generation capacity over the forecast period. A large number of power generation companies, especially in the United States and Europe countries, are investing in renewable energy sources. For example, in 2023, EDF emerged as the global leader in investing and producing on-demand, consistently accessible carbon-free electricity, constituting 434TW, equivalent to 93% of its power output. With a remarkable carbon intensity of 37gCO2/kWh, it marked a 26% reduction from its 2022 levels. Additionally, as of February 2022, Australian wind turbines annually receive over $500,000 in subsidies via Renewable Energy Certificates. The approval and funding for renewable energy projects are typically swift, facilitated, and subsidized. This is expected to increase demand for construction company services, propelling the market forward during the forecast era. As a result, the expansion of building projects and investments is propelling the Industrial Silica Sand Market forward.

Industrial Silica Sand Market Challenges

The Cost of Silica Sand, as Well as Investments and Transportation, are Limiting Market Development

The cost of silica sand extraction and processing can be significant, especially if high-quality silica sand is required for specific applications such as glass manufacturing or hydraulic fracturing (fracking). Factors influencing the cost include mining techniques, processing methods, and transportation expenses. In 2022, industrial sand and gravel consumption rose due to heightened demand for frac sand, driving prices up. Imports remained steady at 350,000 tons. Frac sand prices surged by 185% in 2022 to $40-$45/tonne due to import constraints from Russia amid the Ukraine conflict, driving up costs., but has risen to over $70 per ton during times of scarcity. Spending money on oil is challenging. Sand is heavy, and because of its value, transporting and processing it is expensive and difficult. Traders are unable to buy or sell futures contracts tied to coal, just as they are unable to buy or sell futures contracts tied to other items such as soybeans or gasoline. As a result, shareholders interested in increasing their sand exposure should look for investments in sand-related businesses. However, government regulations on the use of silica, fluctuations in raw material supply, and product cost instability are expected to limit demand growth in the coming years. Illegal sand mining and the production of sand-free construction goods can also stymie global market growth.

Industrial Silica Sand Market Industry Outlook

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in the Industrial Silica Sand Market. The key players in the Industrial Silica Sand Market include Sibelco, Hi-Crush Inc., U.S. Silica Holdings Inc., JFE Holdings Inc., Mitsubishi Corporation, Covia Holdings LLC, Badger Mining Corporation, PUM Group, Quarzwerke GmbH, Chem Source Egypt, among others.

Acquisitions/Technology Launches

- In July 2022, Sibelco expands its footprint by acquiring Echasa S.A., a silica sand mining company operating in Northern Spain. The acquisition includes the Laminoria quarry near Vitoria, strategically located 160 kilometers from Sibelco's nearest silica quarry in Arija. The acquisition expands Sibelco's customer reach and silica sand reserves in Western Europe, complementing its existing operations in the region.

- In April 2022, Source Energy Services Ltd. has finalized a transaction with Canadian Silica Industries Inc. and Contractor’s Leasing Corp., acquiring operations, distribution, and sales responsibilities for domestic frac sand from CSI’s Peace River facility. This adds 400,000 metric tonnes of production capacity, enhances offerings, and fosters production efficiencies through consolidation.

For more Chemicals and Materials Market reports, please click here

1. Industrial Silica Sand Market - Overview

1.1 Definitions and Scope

2. Industrial Silica Sand Market - Executive Summary

2.1 Key Trends by Purity

2.2 Key Trends by Silica Sand

2.3 Key Trends by Application

2.4 Key Trends by Geography

3. Industrial Silica Sand Market - Comparative Analysis

3.1 Company Benchmarking

3.2 Global Financial Analysis

3.3 Market Share Analysis

3.4 Patent Analysis

3.5 Pricing Analysis

4. Industrial Silica Sand Market - Start-up Companies Scenario

4.1 Key Start-up Company Analysis by

4.1.1 Investment

4.1.2 Revenue

4.1.3 Venture Capital and Funding Scenario

5. Industrial Silica Sand Market – Market Entry Scenario Premium

5.1 Regulatory Framework Overview

5.2 New Business and Ease of Doing Business Index

5.3 Case Studies of Successful Ventures

6. Industrial Silica Sand Market - Forces

6.1 Market Drivers

6.2 Market Constraints/Challenges

6.3 Porter’s Five Force Model

6.3.1 Bargaining power of suppliers

6.3.2 Bargaining powers of customers

6.3.3 Threat of new entrants

6.3.4 Rivalry among existing players

6.3.5 Threat of substitutes

7. Industrial Silica Sand Market – Strategic Analysis

7.1 Value Chain Analysis

7.2 Opportunities Analysis

7.3 Market Life Cycle

8. Industrial Silica Sand Market– By Purity (Market Size -$Million/Billion)

8.1 94% to 95.9%

8.2 96% to 97.9%

8.3 98% to 98.9%

8.4 Above 99%

9. Industrial Silica Sand Market– By Silica Sand (Market Size -$Million/Billion)

9.1 Wet Sand

9.2 Dry Sand

9.3 Frac Sand

9.4 Filter Sand

9.5 Coated Sand

9.6 Others

10. Industrial Silica Sand Market– By Application (Market Size -$Million/Billion)

10.1 Glass Manufacturing

10.1.1 Flat Glass

10.1.2 Fiberglass Insulation

10.1.3 Specialty Glass

10.1.4 Container Glass & Others

10.2 Chemical Production

10.2.1 Sodium Silicate

10.2.2 Silicon Gels

10.2.3 Silicon Tetrachloride

10.2.4 Others

10.3 Foundry

10.3.1 Ferrous Foundry

10.3.2 Nonferrous Foundry

10.4 Construction

10.4.1 Cement

10.4.2 Asphalt Mixtures

10.4.3 Mortar

10.4.4 Others

10.5 Paints & Coatings

10.5.1 Architectural Paints & Coatings

10.5.2 Industrial Paints & Coatings

10.6 Ceramics & Refractories

10.6.1 Tableware

10.6.2 Sanitaryware

10.6.3 Floor and Wall Tiles

10.7 Filtration and Water Production

10.7.1 Drinking Water

10.7.2 Wastewater

10.8 Oil & Gas Recovery

10.9 Others

11. Industrial Silica Sand Market – By Geography (Market Size - $Million/$Billion)

11.1 North America

11.1.1 U.S.

11.1.2 Canada

11.1.3 Mexico

11.2 Europe

11.2.1 UK

11.2.2 Germany

11.2.3 France

11.2.4 Italy

11.2.5 Netherlands

11.2.6 Spain

11.2.7 Russia

11.2.8 Belgium

11.2.9 Rest of Europe

11.3 Asia-Pacific

11.3.1 China

11.3.2 Japan

11.3.3 India

11.3.4 South Korea

11.3.5 Australia and New Zealand

11.3.6 Indonesia

11.3.7 Taiwan

11.3.8 Malaysia

11.3.9 Rest of Asia-Pacific

11.4 South America

11.4.1 Brazil

11.4.2 Argentina

11.4.3 Chile

11.4.4 Colombia

11.4.5 Rest of South America

11.5 Rest of The World

11.5.1 Middle East

11.5.1.1 Saudi Arabia

11.5.1.2 UAE

11.5.1.3 Israel

11.5.1.4 Rest of the Middle East

11.5.2 Africa

11.5.2.1 South Africa

11.5.2.2 Nigeria

11.5.2.3 Rest of Africa

12. Industrial Silica Sand Market - Entropy

13. Industrial Silica Sand Market – Industry/Segment Competition Landscape

13.1 Market Share Analysis

13.1.1 Global Market Share – Key Companies

13.1.2 Market Share by Region – Key Companies

13.1.3 Market Share by Countries – Key Companies

13.2 Competition Matrix

13.3 Best Practices for Companies

14. Industrial Silica Sand Market – Key Company List by Country Premium

15. Industrial Silica Sand Market- Company Analysis

15.1 Sibelco

15.2 Hi-Crush Inc.

15.3 U.S. Silica Holdings Inc.

15.4 JFE Holdings Inc.

15.5 Mitsubishi Corporation

15.6 Covia Holdings LLC

15.7 Badger Mining Corporation

15.8 PUM Group

15.9 Quarzwerke GmbH

15.10 Chem Source Egypt

* "Financials would be provided to private companies on best-efforts basis."

LIST OF TABLES

1.Global Industrial Silica Sand Technology Analysis Market 2023-2030 ($M)

1.1 Foundry Market 2023-2030 ($M) - Global Industry Research

1.2 Hydraulic Fracturing Market 2023-2030 ($M) - Global Industry Research

1.3 Construction Market 2023-2030 ($M) - Global Industry Research

2.Global Competitive Landscape Market 2023-2030 ($M)

2.1 Revenue Analysis Market 2023-2030 ($M) - Global Industry Research

3.Global Industrial Silica Sand Technology Analysis Market 2023-2030 (Volume/Units)

3.1 Foundry Market 2023-2030 (Volume/Units) - Global Industry Research

3.2 Hydraulic Fracturing Market 2023-2030 (Volume/Units) - Global Industry Research

3.3 Construction Market 2023-2030 (Volume/Units) - Global Industry Research

4.Global Competitive Landscape Market 2023-2030 (Volume/Units)

4.1 Revenue Analysis Market 2023-2030 (Volume/Units) - Global Industry Research

5.North America Industrial Silica Sand Technology Analysis Market 2023-2030 ($M)

5.1 Foundry Market 2023-2030 ($M) - Regional Industry Research

5.2 Hydraulic Fracturing Market 2023-2030 ($M) - Regional Industry Research

5.3 Construction Market 2023-2030 ($M) - Regional Industry Research

6.North America Competitive Landscape Market 2023-2030 ($M)

6.1 Revenue Analysis Market 2023-2030 ($M) - Regional Industry Research

7.South America Industrial Silica Sand Technology Analysis Market 2023-2030 ($M)

7.1 Foundry Market 2023-2030 ($M) - Regional Industry Research

7.2 Hydraulic Fracturing Market 2023-2030 ($M) - Regional Industry Research

7.3 Construction Market 2023-2030 ($M) - Regional Industry Research

8.South America Competitive Landscape Market 2023-2030 ($M)

8.1 Revenue Analysis Market 2023-2030 ($M) - Regional Industry Research

9.Europe Industrial Silica Sand Technology Analysis Market 2023-2030 ($M)

9.1 Foundry Market 2023-2030 ($M) - Regional Industry Research

9.2 Hydraulic Fracturing Market 2023-2030 ($M) - Regional Industry Research

9.3 Construction Market 2023-2030 ($M) - Regional Industry Research

10.Europe Competitive Landscape Market 2023-2030 ($M)

10.1 Revenue Analysis Market 2023-2030 ($M) - Regional Industry Research

11.APAC Industrial Silica Sand Technology Analysis Market 2023-2030 ($M)

11.1 Foundry Market 2023-2030 ($M) - Regional Industry Research

11.2 Hydraulic Fracturing Market 2023-2030 ($M) - Regional Industry Research

11.3 Construction Market 2023-2030 ($M) - Regional Industry Research

12.APAC Competitive Landscape Market 2023-2030 ($M)

12.1 Revenue Analysis Market 2023-2030 ($M) - Regional Industry Research

13.MENA Industrial Silica Sand Technology Analysis Market 2023-2030 ($M)

13.1 Foundry Market 2023-2030 ($M) - Regional Industry Research

13.2 Hydraulic Fracturing Market 2023-2030 ($M) - Regional Industry Research

13.3 Construction Market 2023-2030 ($M) - Regional Industry Research

14.MENA Competitive Landscape Market 2023-2030 ($M)

14.1 Revenue Analysis Market 2023-2030 ($M) - Regional Industry Research

LIST OF FIGURES

1.US Industrial Silica Sands Market Revenue, 2023-2030 ($M)

2.Canada Industrial Silica Sands Market Revenue, 2023-2030 ($M)

3.Mexico Industrial Silica Sands Market Revenue, 2023-2030 ($M)

4.Brazil Industrial Silica Sands Market Revenue, 2023-2030 ($M)

5.Argentina Industrial Silica Sands Market Revenue, 2023-2030 ($M)

6.Peru Industrial Silica Sands Market Revenue, 2023-2030 ($M)

7.Colombia Industrial Silica Sands Market Revenue, 2023-2030 ($M)

8.Chile Industrial Silica Sands Market Revenue, 2023-2030 ($M)

9.Rest of South America Industrial Silica Sands Market Revenue, 2023-2030 ($M)

10.UK Industrial Silica Sands Market Revenue, 2023-2030 ($M)

11.Germany Industrial Silica Sands Market Revenue, 2023-2030 ($M)

12.France Industrial Silica Sands Market Revenue, 2023-2030 ($M)

13.Italy Industrial Silica Sands Market Revenue, 2023-2030 ($M)

14.Spain Industrial Silica Sands Market Revenue, 2023-2030 ($M)

15.Rest of Europe Industrial Silica Sands Market Revenue, 2023-2030 ($M)

16.China Industrial Silica Sands Market Revenue, 2023-2030 ($M)

17.India Industrial Silica Sands Market Revenue, 2023-2030 ($M)

18.Japan Industrial Silica Sands Market Revenue, 2023-2030 ($M)

19.South Korea Industrial Silica Sands Market Revenue, 2023-2030 ($M)

20.South Africa Industrial Silica Sands Market Revenue, 2023-2030 ($M)

21.North America Industrial Silica Sands By Application

22.South America Industrial Silica Sands By Application

23.Europe Industrial Silica Sands By Application

24.APAC Industrial Silica Sands By Application

25.MENA Industrial Silica Sands By Application