Email

Email Print

Print

Data Center Liquid Cooling Market - By Service , By Cooling Strategies , By Cooling Techniques , By End User Types , By Industry Vertical and By Geography - Opportunity Analysis & Industry Forecast, 2024-2030.

Data Center Liquid Cooling Market Overview:

The Data Center Liquid Cooling Market size is estimated to reach $14.8 Billion by 2030, growing at a CAGR of 25.6% during the forecast period 2024-2030. The data center liquid cooling market involves the use of liquid-based systems to manage heat in data centers, offering more efficient and energy-saving solutions compared to traditional air cooling. These systems, which include direct-to-chip cooling, immersion cooling, and chilled liquid cooling, are gaining traction as data centers face rising power densities and the need for more sustainable operations. The increasing demand for energy-efficient and sustainable cooling solutions due to rising energy costs, the expansion of high-performance computing and cloud services, and the need to meet carbon reduction goals are driving the market growth. Additionally, the advances in cooling fluids and materials, shift towards edge computing, data sovereignty, and geopolitical instability are accelerating the adoption of liquid cooling technologies, positioning them as a crucial component in the evolution of modern data centers.

Innovations in immersion cooling technology are focused on enhancing performance, scalability and cost-effectiveness, making it an ideal solution for hyperscale data centers and cloud service providers. For instance, in October 2024, Supermicro, Inc. unveiled a comprehensive liquid cooling solution that includes advanced Coolant Distribution Units (CDUs), cold plates, Coolant Distribution Manifolds (CDMs), cooling towers and end-to-end management software. This solution is designed to significantly reduce ongoing power consumption, lower Day 0 hardware acquisition costs, and streamline data center cooling infrastructure. At the same time, the integration of renewable energy into data center operations is becoming a key trend, as companies seek to reduce their carbon footprint and achieve sustainability goals. For example, in Septemeber 2024 Cloud Carrier launched Australia's first liquid-cooled data campus at the Southern Highlands Data Campus (SHDC), which covers 67 hectares and has the potential to expand up to 300MW. This facility focuses on high-density and sustainable cooling solutions. As both immersion cooling technologies and renewable energy solutions continue to evolve, their combined impact is expected to drive a new wave of innovation in data center cooling, ensuring that these facilities remain both technologically advanced and environmentally sustainable.

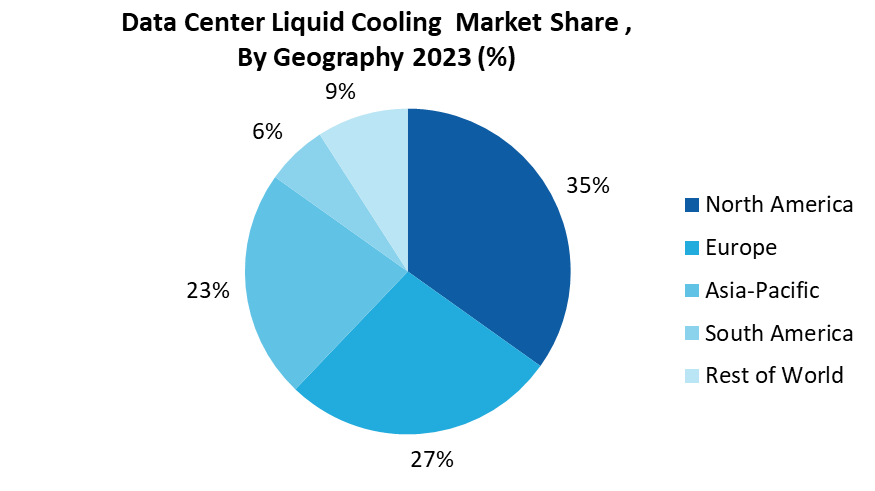

Market Snapshot:

Data Center Liquid Cooling Market- Report Coverage:

The “Data Center Liquid Cooling Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Data Center Liquid Cooling Market.

| Attribute | Segment |

|---|---|

|

By Service

|

|

|

By Cooling Strategies

|

|

|

By Cooling Techniques

|

|

|

By End User Types

|

|

|

By Industry Vertical

|

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

During the COVID-19 pandemic, as digital services surged due to remote work and streaming, the demand for data center capacity skyrocketed placing additional strain on cooling systems. Traditional air cooling became less effective for managing the increased heat output of high-density servers, making liquid cooling solutions, which offer superior heat dissipation and energy efficiency, more attractive. The pandemic also accelerated the adoption of automated and remotely managed cooling systems, as social distancing and staffing challenges made on-site maintenance more difficult.

The Russia-Ukraine war has had a notable impact on the data center liquid cooling market, influencing both demand and operational challenges. The disruption of energy supplies, particularly in Europe drove up energy prices prompting data center operators to seek more energy-efficient cooling solutions like liquid cooling, which offers superior performance and lower power consumption compared to traditional air cooling.

Key Takeaways:

-

North America Leads the Market:

North America accounted for largest market share in 2023. In recent years, the construction and expansion of data centers in North America have surged, particularly in key tech hubs such as Northern Virginia, Silicon Valley, Dallas, and Phoenix. These areas are seeing a rise in the development of new hyperscale and colocation data centers. The growing dependence on cloud services and the increasing need for low-latency connections are pushing companies to establish data centers closer to major metropolitan regions. According to CBRE's June 2024 report, North America's data center inventory expanded by 24.4% year-over-year in Q1 2024, adding 807.5 MW across cities like Northern Virginia, Chicago, Dallas and Silicon Valley. Northern Virginia led the way, contributing 391.1 MW of new supply, driven by strong demand from public cloud providers and AI companies. Additionally, the region's favorable regulatory environment, political stability, and easy access to renewable energy make it an attractive destination for data center operations. As a result, North America is expected to maintain its leadership position in the market, with a continued focus on sustainability and energy efficiency as key factors in the development of new facilities.

-

IT/ITES/Cloud Service Providers to Register the Fastest Growth

IT/ITES/Cloud Service Providers in the Data Center Liquid Cooling market are expected to experience the fastest growth in 2024. As demand for cloud computing, big data analytics, and AI-driven applications continues to rise, these sectors are experiencing rapid growth, which places increasing pressure on data centers to scale up their computing capabilities while maintaining energy efficiency. In response, cloud service providers are significantly boosting investments in next-generation data centers to meet the growing demands of industries undergoing digital transformation. These investments extend beyond just infrastructure; they also focus on advanced technologies, including liquid cooling solutions, to ensure that data centers can perform at scale while minimizing energy consumption. According to a July 2023 report from International Data Corporation (IDC), spending on compute and storage infrastructure products for cloud deployments surged by 14.9% year-over-year in Q1 2023, reaching $21.5 billion. Strategic partnerships are also playing a critical role in the adoption of liquid cooling technologies within the IT/ITES and cloud sectors. Collaborations between data center operators, cooling solution providers, and technology firms are driving innovation and facilitating the deployment of state-of-the-art liquid cooling systems. These partnerships allow companies to leverage specialized expertise and integrate next-generation solutions that optimize both performance and energy efficiency. For example, in February 2024, Data Center Frontier stated that the ongoing wave of M&A and strategic partnerships in advanced cooling for AI and cloud data centers has led to the acquisition of a controlling stake in DDC Cabinet Technology, a leader in extreme-density cooling solutions, by the investment backers of multi-tenant cloud and colocation provider TierPoint.

-

Tier 3 Data Center is the Largest Segment

Tier 3 data centers are leading the market due to their outstanding combination of reliability, scalability, and energy efficiency. The growing demand for these data centers is largely driven by the need for high availability and redundancy, essential for businesses that depend heavily on digital infrastructure. Additionally, Tier 3 data centers provide scalable solutions, making them particularly well-suited for organizations experiencing rapid growth, especially in sectors such as cloud computing, AI and big data. As more companies adopt cloud and hybrid cloud strategies, Tier 3 facilities are increasingly the preferred choice because of their strong support for colocation services and their seamless integration with cloud environments. For example, in October 2024, Bit Digital, Inc. acquired Enovum Data Centers for approximately $45 million, integrating their high-performance computing (HPC) operations with an operational Tier 3 facility in a major city, further diversifying their colocation customer base. Moreover, these data centers are placing significant emphasis on energy efficiency and sustainability, adopting advanced cooling technologies and integrating renewable energy sources to comply with regulatory standards and meet environmental goals. As the market continues to develop, Tier 3 data centers are poised to maintain their leadership role, offering businesses the reliable, flexible and cost-effective infrastructure needed to thrive in today’s competitive digital landscape.

-

Growth of Cloud Computing and Data-Intensive Applications to Boost the Market

The growth of cloud computing and the increasing use of data-intensive applications are major drivers shaping the future of the data center industry. As businesses across industries continue to embrace cloud-based solutions, the demand for scalable, flexible, and efficient data infrastructure is rapidly expanding. Cloud computing allows companies to offload their IT infrastructure management, providing them with on-demand access to resources such as storage, computing power, and networking. This shift is fueling the growth of hyperscale data centers designed to support massive amounts of data traffic and computing demands. At the same time, data-intensive applications, such as those powered by artificial intelligence (AI), big data analytics, and machine learning, require high-performance computing capabilities and the ability to process large datasets in real time. These applications place significant pressure on data centers to deliver enhanced processing power, low-latency performance, and energy-efficient cooling solutions to manage the increasing workloads. As a result, data centers are evolving to support these advanced computing requirements, with a focus on adopting liquid cooling technologies, high-density computing racks, and next-generation server architecture to meet the growing demands of cloud computing and data-intensive applications. For instance, on August 9, 2024, Giga Computing, a subsidiary of GIGABYTE and a leader in generative AI servers and advanced cooling technologies, launched two new GIGABYTE R-series servers (the R183-ZK0 and R283-ZK0). These servers are designed to offer improved performance and reliability for cloud services and data-intensive applications.

-

Lack of Standardization to Hamper the Market

Lack of standardization remains a significant challenge for the data center liquid cooling market. As the industry evolves rapidly, various cooling technologies, design approaches, and operational models have emerged, but the absence of universally accepted standards creates inconsistencies and interoperability issues. Different data centers may adopt unique cooling solutions, which can make it difficult to integrate new technologies or scale operations across multiple facilities. This lack of uniformity also complicates maintenance, as technicians and operators may need specialized training to handle diverse systems. Furthermore, it hinders the development of a cohesive global supply chain for liquid cooling equipment, leading to higher costs and longer lead times. The absence of standardized protocols for things like temperature regulation, fluid management, and system monitoring can also result in inefficiencies and increased energy consumption, making it harder for data centers to meet sustainability goals. For the market to mature and reach its full potential, industry-wide standards are needed to ensure compatibility, streamline operations, and reduce costs.

For more details on this report - Request for Sample

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships, and collaborations are key strategies adopted by players in the Data Center Liquid Cooling Market. The top 10 companies in this industry are listed below:

- Vertiv Group Corp.

- Schneider Electric

- Rittal GmbH & Co. KG

- Asetek A/S

- Asperitas

- Green Revolution Cooling, Inc

- BlackBox

- Chilldyne, Inc

- COOLIT SYSTEMS

- DCX

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

25.6% |

|

Market Size in 2030 |

$14.8 Billion |

|

Segments Covered |

By Service, By Cooling Strategies, By Cooling Techniques, By End User Types, By Industry Vertical and By Geography. |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (UK, Germany, France, Italy, Netherlands, Spain, Belgium, Denmark and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Taiwan Hong Kong, Malaysia and Rest of Asia-Pacific), South America (Brazil, Argentina,Venezuela, Ecuador, Peru, Colombia, Cost Rica and Rest of South America)[MF1] , Rest of the World (Middle East and Africa). |

|

Key Market Players |

|

LIST OF TABLES

1.Global Data Center Liquid Cooling Market Analysis By Liquid Cooling Solution Market 2023-2030 ($M)

1.1 Indirect Liquid Cooling Market 2023-2030 ($M) - Global Industry Research

1.1.1 Rack-Based Liquid Cooling Market 2023-2030 ($M)

1.2 Direct Liquid Cooling Market 2023-2030 ($M) - Global Industry Research

1.2.1 Single-Phase Immersion Cooling Market 2023-2030 ($M)

1.2.2 Two-Phase Immersion Cooling Market 2023-2030 ($M)

2.Global Data Center Liquid Cooling Market Analysis By Service Market 2023-2030 ($M)

2.1 Design & Consulting Market 2023-2030 ($M) - Global Industry Research

2.2 Installation & Deployment Market 2023-2030 ($M) - Global Industry Research

2.3 Support & Maintenance Market 2023-2030 ($M) - Global Industry Research

3.Global Data Center Liquid Cooling Market Analysis By Data Center Type Market 2023-2030 ($M)

3.1 Small & Medium- Size Data Center Market 2023-2030 ($M) - Global Industry Research

3.2 Enterprise Data Centers Market 2023-2030 ($M) - Global Industry Research

3.3 Large Data Centers Market 2023-2030 ($M) - Global Industry Research

4.Global Data Center Liquid Cooling Market Analysis By Industry Market 2023-2030 ($M)

4.1 IT & Telecom Market 2023-2030 ($M) - Global Industry Research

4.2 Government & Defense Market 2023-2030 ($M) - Global Industry Research

4.3 Healthcare Market 2023-2030 ($M) - Global Industry Research

4.4 Research & Academic Market 2023-2030 ($M) - Global Industry Research

4.5 Retail Market 2023-2030 ($M) - Global Industry Research

4.6 Energy Market 2023-2030 ($M) - Global Industry Research

4.7 Manufacturing Market 2023-2030 ($M) - Global Industry Research

5.Global Data Center Liquid Cooling Market Analysis By Liquid Cooling Solution Market 2023-2030 (Volume/Units)

5.1 Indirect Liquid Cooling Market 2023-2030 (Volume/Units) - Global Industry Research

5.1.1 Rack-Based Liquid Cooling Market 2023-2030 (Volume/Units)

5.2 Direct Liquid Cooling Market 2023-2030 (Volume/Units) - Global Industry Research

5.2.1 Single-Phase Immersion Cooling Market 2023-2030 (Volume/Units)

5.2.2 Two-Phase Immersion Cooling Market 2023-2030 (Volume/Units)

6.Global Data Center Liquid Cooling Market Analysis By Service Market 2023-2030 (Volume/Units)

6.1 Design & Consulting Market 2023-2030 (Volume/Units) - Global Industry Research

6.2 Installation & Deployment Market 2023-2030 (Volume/Units) - Global Industry Research

6.3 Support & Maintenance Market 2023-2030 (Volume/Units) - Global Industry Research

7.Global Data Center Liquid Cooling Market Analysis By Data Center Type Market 2023-2030 (Volume/Units)

7.1 Small & Medium- Size Data Center Market 2023-2030 (Volume/Units) - Global Industry Research

7.2 Enterprise Data Centers Market 2023-2030 (Volume/Units) - Global Industry Research

7.3 Large Data Centers Market 2023-2030 (Volume/Units) - Global Industry Research

8.Global Data Center Liquid Cooling Market Analysis By Industry Market 2023-2030 (Volume/Units)

8.1 IT & Telecom Market 2023-2030 (Volume/Units) - Global Industry Research

8.2 Government & Defense Market 2023-2030 (Volume/Units) - Global Industry Research

8.3 Healthcare Market 2023-2030 (Volume/Units) - Global Industry Research

8.4 Research & Academic Market 2023-2030 (Volume/Units) - Global Industry Research

8.5 Retail Market 2023-2030 (Volume/Units) - Global Industry Research

8.6 Energy Market 2023-2030 (Volume/Units) - Global Industry Research

8.7 Manufacturing Market 2023-2030 (Volume/Units) - Global Industry Research

9.North America Data Center Liquid Cooling Market Analysis By Liquid Cooling Solution Market 2023-2030 ($M)

9.1 Indirect Liquid Cooling Market 2023-2030 ($M) - Regional Industry Research

9.1.1 Rack-Based Liquid Cooling Market 2023-2030 ($M)

9.2 Direct Liquid Cooling Market 2023-2030 ($M) - Regional Industry Research

9.2.1 Single-Phase Immersion Cooling Market 2023-2030 ($M)

9.2.2 Two-Phase Immersion Cooling Market 2023-2030 ($M)

10.North America Data Center Liquid Cooling Market Analysis By Service Market 2023-2030 ($M)

10.1 Design & Consulting Market 2023-2030 ($M) - Regional Industry Research

10.2 Installation & Deployment Market 2023-2030 ($M) - Regional Industry Research

10.3 Support & Maintenance Market 2023-2030 ($M) - Regional Industry Research

11.North America Data Center Liquid Cooling Market Analysis By Data Center Type Market 2023-2030 ($M)

11.1 Small & Medium- Size Data Center Market 2023-2030 ($M) - Regional Industry Research

11.2 Enterprise Data Centers Market 2023-2030 ($M) - Regional Industry Research

11.3 Large Data Centers Market 2023-2030 ($M) - Regional Industry Research

12.North America Data Center Liquid Cooling Market Analysis By Industry Market 2023-2030 ($M)

12.1 IT & Telecom Market 2023-2030 ($M) - Regional Industry Research

12.2 Government & Defense Market 2023-2030 ($M) - Regional Industry Research

12.3 Healthcare Market 2023-2030 ($M) - Regional Industry Research

12.4 Research & Academic Market 2023-2030 ($M) - Regional Industry Research

12.5 Retail Market 2023-2030 ($M) - Regional Industry Research

12.6 Energy Market 2023-2030 ($M) - Regional Industry Research

12.7 Manufacturing Market 2023-2030 ($M) - Regional Industry Research

13.South America Data Center Liquid Cooling Market Analysis By Liquid Cooling Solution Market 2023-2030 ($M)

13.1 Indirect Liquid Cooling Market 2023-2030 ($M) - Regional Industry Research

13.1.1 Rack-Based Liquid Cooling Market 2023-2030 ($M)

13.2 Direct Liquid Cooling Market 2023-2030 ($M) - Regional Industry Research

13.2.1 Single-Phase Immersion Cooling Market 2023-2030 ($M)

13.2.2 Two-Phase Immersion Cooling Market 2023-2030 ($M)

14.South America Data Center Liquid Cooling Market Analysis By Service Market 2023-2030 ($M)

14.1 Design & Consulting Market 2023-2030 ($M) - Regional Industry Research

14.2 Installation & Deployment Market 2023-2030 ($M) - Regional Industry Research

14.3 Support & Maintenance Market 2023-2030 ($M) - Regional Industry Research

15.South America Data Center Liquid Cooling Market Analysis By Data Center Type Market 2023-2030 ($M)

15.1 Small & Medium- Size Data Center Market 2023-2030 ($M) - Regional Industry Research

15.2 Enterprise Data Centers Market 2023-2030 ($M) - Regional Industry Research

15.3 Large Data Centers Market 2023-2030 ($M) - Regional Industry Research

16.South America Data Center Liquid Cooling Market Analysis By Industry Market 2023-2030 ($M)

16.1 IT & Telecom Market 2023-2030 ($M) - Regional Industry Research

16.2 Government & Defense Market 2023-2030 ($M) - Regional Industry Research

16.3 Healthcare Market 2023-2030 ($M) - Regional Industry Research

16.4 Research & Academic Market 2023-2030 ($M) - Regional Industry Research

16.5 Retail Market 2023-2030 ($M) - Regional Industry Research

16.6 Energy Market 2023-2030 ($M) - Regional Industry Research

16.7 Manufacturing Market 2023-2030 ($M) - Regional Industry Research

17.Europe Data Center Liquid Cooling Market Analysis By Liquid Cooling Solution Market 2023-2030 ($M)

17.1 Indirect Liquid Cooling Market 2023-2030 ($M) - Regional Industry Research

17.1.1 Rack-Based Liquid Cooling Market 2023-2030 ($M)

17.2 Direct Liquid Cooling Market 2023-2030 ($M) - Regional Industry Research

17.2.1 Single-Phase Immersion Cooling Market 2023-2030 ($M)

17.2.2 Two-Phase Immersion Cooling Market 2023-2030 ($M)

18.Europe Data Center Liquid Cooling Market Analysis By Service Market 2023-2030 ($M)

18.1 Design & Consulting Market 2023-2030 ($M) - Regional Industry Research

18.2 Installation & Deployment Market 2023-2030 ($M) - Regional Industry Research

18.3 Support & Maintenance Market 2023-2030 ($M) - Regional Industry Research

19.Europe Data Center Liquid Cooling Market Analysis By Data Center Type Market 2023-2030 ($M)

19.1 Small & Medium- Size Data Center Market 2023-2030 ($M) - Regional Industry Research

19.2 Enterprise Data Centers Market 2023-2030 ($M) - Regional Industry Research

19.3 Large Data Centers Market 2023-2030 ($M) - Regional Industry Research

20.Europe Data Center Liquid Cooling Market Analysis By Industry Market 2023-2030 ($M)

20.1 IT & Telecom Market 2023-2030 ($M) - Regional Industry Research

20.2 Government & Defense Market 2023-2030 ($M) - Regional Industry Research

20.3 Healthcare Market 2023-2030 ($M) - Regional Industry Research

20.4 Research & Academic Market 2023-2030 ($M) - Regional Industry Research

20.5 Retail Market 2023-2030 ($M) - Regional Industry Research

20.6 Energy Market 2023-2030 ($M) - Regional Industry Research

20.7 Manufacturing Market 2023-2030 ($M) - Regional Industry Research

21.APAC Data Center Liquid Cooling Market Analysis By Liquid Cooling Solution Market 2023-2030 ($M)

21.1 Indirect Liquid Cooling Market 2023-2030 ($M) - Regional Industry Research

21.1.1 Rack-Based Liquid Cooling Market 2023-2030 ($M)

21.2 Direct Liquid Cooling Market 2023-2030 ($M) - Regional Industry Research

21.2.1 Single-Phase Immersion Cooling Market 2023-2030 ($M)

21.2.2 Two-Phase Immersion Cooling Market 2023-2030 ($M)

22.APAC Data Center Liquid Cooling Market Analysis By Service Market 2023-2030 ($M)

22.1 Design & Consulting Market 2023-2030 ($M) - Regional Industry Research

22.2 Installation & Deployment Market 2023-2030 ($M) - Regional Industry Research

22.3 Support & Maintenance Market 2023-2030 ($M) - Regional Industry Research

23.APAC Data Center Liquid Cooling Market Analysis By Data Center Type Market 2023-2030 ($M)

23.1 Small & Medium- Size Data Center Market 2023-2030 ($M) - Regional Industry Research

23.2 Enterprise Data Centers Market 2023-2030 ($M) - Regional Industry Research

23.3 Large Data Centers Market 2023-2030 ($M) - Regional Industry Research

24.APAC Data Center Liquid Cooling Market Analysis By Industry Market 2023-2030 ($M)

24.1 IT & Telecom Market 2023-2030 ($M) - Regional Industry Research

24.2 Government & Defense Market 2023-2030 ($M) - Regional Industry Research

24.3 Healthcare Market 2023-2030 ($M) - Regional Industry Research

24.4 Research & Academic Market 2023-2030 ($M) - Regional Industry Research

24.5 Retail Market 2023-2030 ($M) - Regional Industry Research

24.6 Energy Market 2023-2030 ($M) - Regional Industry Research

24.7 Manufacturing Market 2023-2030 ($M) - Regional Industry Research

25.MENA Data Center Liquid Cooling Market Analysis By Liquid Cooling Solution Market 2023-2030 ($M)

25.1 Indirect Liquid Cooling Market 2023-2030 ($M) - Regional Industry Research

25.1.1 Rack-Based Liquid Cooling Market 2023-2030 ($M)

25.2 Direct Liquid Cooling Market 2023-2030 ($M) - Regional Industry Research

25.2.1 Single-Phase Immersion Cooling Market 2023-2030 ($M)

25.2.2 Two-Phase Immersion Cooling Market 2023-2030 ($M)

26.MENA Data Center Liquid Cooling Market Analysis By Service Market 2023-2030 ($M)

26.1 Design & Consulting Market 2023-2030 ($M) - Regional Industry Research

26.2 Installation & Deployment Market 2023-2030 ($M) - Regional Industry Research

26.3 Support & Maintenance Market 2023-2030 ($M) - Regional Industry Research

27.MENA Data Center Liquid Cooling Market Analysis By Data Center Type Market 2023-2030 ($M)

27.1 Small & Medium- Size Data Center Market 2023-2030 ($M) - Regional Industry Research

27.2 Enterprise Data Centers Market 2023-2030 ($M) - Regional Industry Research

27.3 Large Data Centers Market 2023-2030 ($M) - Regional Industry Research

28.MENA Data Center Liquid Cooling Market Analysis By Industry Market 2023-2030 ($M)

28.1 IT & Telecom Market 2023-2030 ($M) - Regional Industry Research

28.2 Government & Defense Market 2023-2030 ($M) - Regional Industry Research

28.3 Healthcare Market 2023-2030 ($M) - Regional Industry Research

28.4 Research & Academic Market 2023-2030 ($M) - Regional Industry Research

28.5 Retail Market 2023-2030 ($M) - Regional Industry Research

28.6 Energy Market 2023-2030 ($M) - Regional Industry Research

28.7 Manufacturing Market 2023-2030 ($M) - Regional Industry Research

LIST OF FIGURES

1.US Data Center Liquid Cooling Market Revenue, 2023-2030 ($M)

2.Canada Data Center Liquid Cooling Market Revenue, 2023-2030 ($M)

3.Mexico Data Center Liquid Cooling Market Revenue, 2023-2030 ($M)

4.Brazil Data Center Liquid Cooling Market Revenue, 2023-2030 ($M)

5.Argentina Data Center Liquid Cooling Market Revenue, 2023-2030 ($M)

6.Peru Data Center Liquid Cooling Market Revenue, 2023-2030 ($M)

7.Colombia Data Center Liquid Cooling Market Revenue, 2023-2030 ($M)

8.Chile Data Center Liquid Cooling Market Revenue, 2023-2030 ($M)

9.Rest of South America Data Center Liquid Cooling Market Revenue, 2023-2030 ($M)

10.UK Data Center Liquid Cooling Market Revenue, 2023-2030 ($M)

11.Germany Data Center Liquid Cooling Market Revenue, 2023-2030 ($M)

12.France Data Center Liquid Cooling Market Revenue, 2023-2030 ($M)

13.Italy Data Center Liquid Cooling Market Revenue, 2023-2030 ($M)

14.Spain Data Center Liquid Cooling Market Revenue, 2023-2030 ($M)

15.Rest of Europe Data Center Liquid Cooling Market Revenue, 2023-2030 ($M)

16.China Data Center Liquid Cooling Market Revenue, 2023-2030 ($M)

17.India Data Center Liquid Cooling Market Revenue, 2023-2030 ($M)

18.Japan Data Center Liquid Cooling Market Revenue, 2023-2030 ($M)

19.South Korea Data Center Liquid Cooling Market Revenue, 2023-2030 ($M)

20.South Africa Data Center Liquid Cooling Market Revenue, 2023-2030 ($M)

21.North America Data Center Liquid Cooling By Application

22.South America Data Center Liquid Cooling By Application

23.Europe Data Center Liquid Cooling By Application

24.APAC Data Center Liquid Cooling By Application

25.MENA Data Center Liquid Cooling By Application

26.Asetek, Sales /Revenue, 2015-2018 ($Mn/$Bn)

27.Rittal GmbH & Co. Kg., Sales /Revenue, 2015-2018 ($Mn/$Bn)

28.Emerson Electric Co., Sales /Revenue, 2015-2018 ($Mn/$Bn)

29.Schneider Electric SE, Sales /Revenue, 2015-2018 ($Mn/$Bn)

30.IBM, Sales /Revenue, 2015-2018 ($Mn/$Bn)

31.Green Revolution Cooling Inc., Sales /Revenue, 2015-2018 ($Mn/$Bn)

32.Allied Control Ltd., Sales /Revenue, 2015-2018 ($Mn/$Bn)

33.Green Data Center LLP, Sales /Revenue, 2015-2018 ($Mn/$Bn)

34.Horizon Computing Solutions, Sales /Revenue, 2015-2018 ($Mn/$Bn)

The Data Center Liquid Cooling Market is projected to grow at 25.6% CAGR during the forecast period 2024-2030.

The Data Center Liquid Cooling Market size is estimated to be $3.0 Billion in 2023 and is projected to reach $14.8 Billion by 2030.

The leading players in the Data Center Liquid Cooling Market are Vertiv Group Corp., Schneider Electric, Rittal GmbH & Co. KG, Asetek A/S, Asperitas and Others.

Adoption of immersion and direct liquid cooling, integration of renewable energy into data center operations and deployment of hyperscale data centers are some of the major data center liquid cooling market trends in the industry which will create growth opportunities for the market during the forecast period.

Key driving factors include rising power density in data centers, advances in cooling fluids or materials, growth of cloud computing, the increasing demand for energy-efficient, sustainable cooling solutions and the need to meet carbon reduction goals.