Email

Email Print

Print

Automotive Plastics Market - Forecast(2025 - 2031)

Automotive Plastics Market Overview

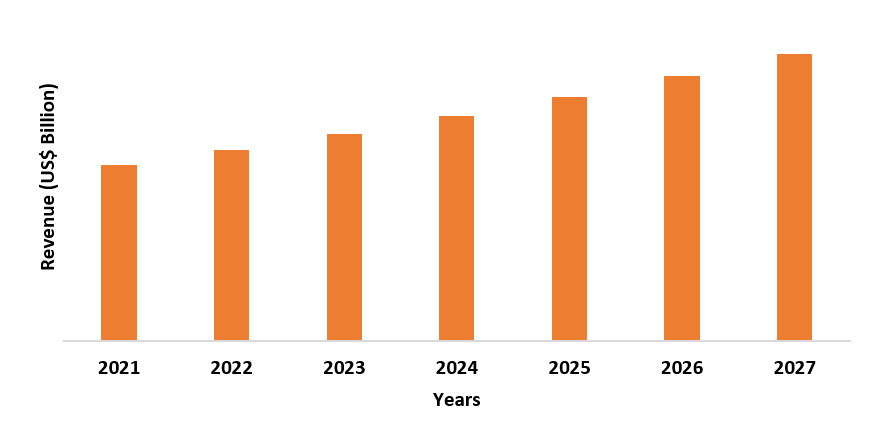

The Automotive Plastics market size is estimated

to reach US$53.8 billion by 2027 after growing at a CAGR of 5.4% during the

forecast period 2022-2027. Automotive Plastics are specialty plastic materials that are used to enhance the safety, performance, and

functionality of vehicles. Automotive plastics such as polypropylene (PP),

polycarbonate (PC), polyvinyl chloride (PVC), polyurethane (PU), acrylonitrile

butadiene styrene (ABS), and others have flourishing applications in automotive

interiors, exteriors, under the bonnet, and other vehicle components. The

superior properties of plastics such as flexibility, corrosion resistance,

thermal insulation, and noise reduction for applicability in light commercial

vehicles for maximum fuel efficiency are creating a drive in the automotive

plastics industry. The covid-19 pandemic disrupted the growth and functioning of

the market. The halt in production, demand and supply gap, and other lockdown

restrictions resulted in a slowdown. However, with robust demand and recovery

in major end-use industries, along with growing automotive vehicle production,

the automotive plastics market is anticipated to rise during the forecast

period.

Report Coverage

The report: “Automotive Plastics Market Report – Forecast (2022-2027)”, by IndustryARC,

covers an in-depth analysis of the following segments of the automotive

plastics market.

Key Takeaways

- Asia-Pacific dominates the automotive plastics market, owing to flourishing lightweight automotive production, established base for light electric vehicles, and rising demand for passenger vehicles in APAC, thereby boosting its growth in the APAC region.

- The passenger vehicles (PV) sector is rapidly growing in the automotive plastics industry due to the rising applicability of plastics such as PP, PU, PVC, PE, and others for various automotive components, along with growing urbanization and demand for light vehicles for transportation, thereby driving the market.

- The rising emphasis on fuel efficiency and lightweight automotive vehicles to reduce carbon emissions and limit fuel consumption creates a drive for the automotive plastics market during the forecast period.

- However, the recyclability issues and emergence of alternatives such as bioplastics, carbon fiber-based plastics, soy, and hemp-based polymers, and others create major challenges and growth slowdown in the automotive plastics market.

For More Details on This Report - Request for Sample

Automotive Plastics Market Segment Analysis – By Type

The Polypropylene (PP) segment held the

largest share in the automotive plastics market in 2021 and is forecasted to

grow at a CAGR of 5.7% during the forecast period 2022-2027. The growth of

polypropylene (PP) plastic in automotive applications is due to its advantages and

preference over other automotive plastics. The superior features of PP such as

fuel efficiency, cost-effectiveness, lightweight, and high suitability for

low-friction applications boost its demand compared to other engineered plastics

options that are not cost-effective and lightweight. Moreover, the versatility

and preference of PP for light vehicles and fuel-efficient vehicles over other

automotive plastics such as polyurethane (PU), acrylonitrile butadiene styrene

(ABS), and others are thereby propelling the demand for polypropylene

automotive plastics. Polypropylene plastics are used in various automotive components

such as dashboards, upholstery, interior trim, car seats, hard plastic parts,

and others. With the increasing applicability of polypropylene in automotive to

manufacture light and low-cost vehicles, the demand for polypropylene plastics is

also substantially rising, thereby supporting the segment growth.

Automotive Plastics Market Segment Analysis – By End-Use Industry

The passenger vehicles (PV) segment held a

significant share in the automotive plastics market in 2021 and is forecasted

to grow at a CAGR of 6.3% during the forecast period 2022-2027. Automotive

plastics such as polycarbonate (PC), polypropylene (PP), polyvinyl chloride

(PVC), and others have major applicability in the passenger vehicles for interior

trim, lighting, bumper, seating, and others. The passenger vehicle sector is

rapidly growing owing to urbanization, demand from the middle-class segment,

and an increase in demand for passenger cars, two-wheelers, and three-wheelers

as public transportation. According to the Society of Indian

Automobile Manufacturers (SIAM), the

domestic sales of passenger vehicles in India rose from 2,711,457 units in

2020-21 to 3,069,499 units in 2021-22. According to the International

Organization of Motor Vehicle Manufacturers (OICA), the total passenger car

production rose from 55,834,456 units in 2020 to 57,054,295 units in 2021. With

the flourishing production and increase in demand for passenger cars across the

globe, the demand for automotive plastics is anticipated to grow rapidly for

applications in exterior, interior components, and others thereby will boost

the growth of the passenger vehicles (PV) industry in the automotive plastics

market during the forecast period.

Automotive Plastics Market Segment Analysis – By Geography

Asia-Pacific region held the largest share in the automotive plastics market in 2021 up to 43%. The robust growth of automotive plastics in APAC is due to flourished automotive vehicle production, growing vehicle manufacturing units, and high demand for specialty plastics in automotive across major counties such as China, India, Japan, and others. The automotive industry, majorly the passenger vehicles and light commercial vehicles sector is growing due to the high demand for fuel-efficient vehicles among the middle-class segment and urbanization. According to the International Organization of Motor Vehicle Manufacturers (OICA), the total automotive production increased from 3% in 2021 after a fall of 2% in China and increased by 30% in 2021 after a decline of 25% in India in 2020. Furthermore, initiatives such as Make in India and Automotive Mission Plan 2026 plan to boost the automotive sector in India and offer a contribution of 12% by automotive in the GDP by 2026. With the increase in automotive vehicle productions and vehicle manufacturing base, majorly for cars and LCV, the demand for automotive plastics such as polypropylene, polyvinyl chloride, polycarbonate, and others for applications in automotive interior, bonnet, exterior parts, and others is anticipated to grow. This will boost the growth of the automotive plastics industry in the Asia-Pacific during the forecast period.

Automotive Plastics Market Drivers

Bolstering Growth of Light Weight and Fuel-Efficient Materials in Vehicles

The demand for lightweight and fuel-efficient

vehicles is growing rapidly. The emphasis by the government on carbon emission

and efficiency is boosting the adoption of lightweight and efficient automotive

vehicles. Automotive plastics such as polypropylene (PP), polyurethane (PU),

and others offer lightweight bodies to the vehicle and have applicability in

vehicle roof, engine, fuel tank, lighting, seating, and others, thereby reducing

the fuel consumption and carbon emissions. For instance, regulations mandate

that the average fuel economy must meet 54.5 miles per gallon in the United

States by 2025. Furthermore, the development of light materials such as lighter

PP, polymethyl methacrylate (PMMA), biodegradable plastic composites, and

others provide lightweight to the automotive body and reduces fuel consumption.

Thus, with rising emphasis on lightweight and reduction in carbon emissions,

the demand for automotive plastics for applications offering lightweight

vehicle components is growing, thereby driving the market.

Rising Production of Electric Vehicles

Automotive plastics

such as polypropylene, polycarbonate, acrylonitrile butadiene, polyurethane,

and others have major applications in the electric vehicle for various

interior, bonnet components, and exterior parts. The electric vehicle sector is

growing rapidly with the increase in government initiatives for vehicle

electrification and stringent emissions norms for fuel-based vehicles for

carbon emissions. For instance, Honda announced plans to invest US$40 billion

in the development of electric vehicles and launch 30 EVs by 2030 in India. According

to the International Energy Agency (IEA), the global electric car sector saw a

growth of 43% in 2020 compared to 2019, hitting a 10 million mark. Furthermore,

the number of electric cars on the roads was 16.5 million in 2021, triple the

number in 2018. With the increase in demand and production for electric

vehicles, the application of automotive plastics such as polypropylene (PP),

polyurethane (PU), and others is growing to offer lightweight and fuel

efficiency for EVs, thereby driving the market and providing major growth in

the market.

Automotive Plastics Market Challenges

Recycling Issues and Emergence of Alternative for

Automotive Applications

Automotive plastics face recycling issues

owing to factors such as the lack of advanced recyclable technology. This

creates environmental impacts and solid waste accumulation, thereby hindering

the demand. Furthermore, the emergence of alternatives such as carbon fiber for

applications in automotive creates a major challenge in the market. The rising

usage of materials prepared from natural fibers, soy and hemp fibers, sheet

molding compounds, and others poses a major threat to automotive plastics such

as polypropylene, polyurethane, PET, and others. Thus, with the issues in

recycling and the threat from other alternative materials, the automotive

plastics market faces a major slowdown and challenge.

Automotive Plastics Industry Outlook

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in the automotive plastics market. Automotive plastics top 10 companies are:

- BASF SE

- LyondellBasell Industries Holdings BV

- Covestro AG

- Evonik Industries

- Solvay SA

- Arkema SA

- LG Chem

- Teijin Ltd.

- Dupont

- SABIC

Recent Developments

- In February 2022, the Celanese planned to acquire the mobility and materials division of DuPont, which produces thermoplastics and elastomers with a large share for automotive applications, thereby boosting the product portfolio and growth in the market.

- In December 2021, the Total Energies and

Plastic Omnium entered into a partnership for the development of recyclable PP

plastic material for applications in the automotive industry. This innovative and recycled PP material will

provide reduced carbon emissions and has flourishing applicability and demand

in 0electric vehicles, thereby offering growth in the market.

- In May 2021, the Covestro AG launched recycled polyethylene terephthalate (rPET) or fused granule technology. This launch has major applications in the automotive industry for interior vehicle parts, thereby boosting the demand and growth in the automotive plastics market.

Relevant Reports

Automotive

Plastic Fasteners Market – Forecast (2022 - 2027)

Report Code: CMR 53208

High

Performance Plastics Market – Forecast (2022 - 2027)

Report Code: CMR 0790

Report Code: CMR 88916

For more Chemicals and Materials Market

reports, please click here

LIST OF TABLES

1.Global Automotive Plastics Market for Passenger Cars By Product Type Market 2023-2030 ($M)1.1 Polypropylene Market 2023-2030 ($M) - Global Industry Research

1.2 Polyurethane Market 2023-2030 ($M) - Global Industry Research

1.3 Polyvinyl Chloride Market 2023-2030 ($M) - Global Industry Research

1.4 Acrylonitrile-Butadiene-Styrene Market 2023-2030 ($M) - Global Industry Research

1.5 Polyamide Market 2023-2030 ($M) - Global Industry Research

1.6 High-Density Polyethylene Market 2023-2030 ($M) - Global Industry Research

1.7 Polycarbonate Market 2023-2030 ($M) - Global Industry Research

1.8 Polybutylene Terephthalate Market 2023-2030 ($M) - Global Industry Research

2.Global Automotive Plastics Market for Passenger Cars By Product Type Market 2023-2030 (Volume/Units)

2.1 Polypropylene Market 2023-2030 (Volume/Units) - Global Industry Research

2.2 Polyurethane Market 2023-2030 (Volume/Units) - Global Industry Research

2.3 Polyvinyl Chloride Market 2023-2030 (Volume/Units) - Global Industry Research

2.4 Acrylonitrile-Butadiene-Styrene Market 2023-2030 (Volume/Units) - Global Industry Research

2.5 Polyamide Market 2023-2030 (Volume/Units) - Global Industry Research

2.6 High-Density Polyethylene Market 2023-2030 (Volume/Units) - Global Industry Research

2.7 Polycarbonate Market 2023-2030 (Volume/Units) - Global Industry Research

2.8 Polybutylene Terephthalate Market 2023-2030 (Volume/Units) - Global Industry Research

3.North America Automotive Plastics Market for Passenger Cars By Product Type Market 2023-2030 ($M)

3.1 Polypropylene Market 2023-2030 ($M) - Regional Industry Research

3.2 Polyurethane Market 2023-2030 ($M) - Regional Industry Research

3.3 Polyvinyl Chloride Market 2023-2030 ($M) - Regional Industry Research

3.4 Acrylonitrile-Butadiene-Styrene Market 2023-2030 ($M) - Regional Industry Research

3.5 Polyamide Market 2023-2030 ($M) - Regional Industry Research

3.6 High-Density Polyethylene Market 2023-2030 ($M) - Regional Industry Research

3.7 Polycarbonate Market 2023-2030 ($M) - Regional Industry Research

3.8 Polybutylene Terephthalate Market 2023-2030 ($M) - Regional Industry Research

4.South America Automotive Plastics Market for Passenger Cars By Product Type Market 2023-2030 ($M)

4.1 Polypropylene Market 2023-2030 ($M) - Regional Industry Research

4.2 Polyurethane Market 2023-2030 ($M) - Regional Industry Research

4.3 Polyvinyl Chloride Market 2023-2030 ($M) - Regional Industry Research

4.4 Acrylonitrile-Butadiene-Styrene Market 2023-2030 ($M) - Regional Industry Research

4.5 Polyamide Market 2023-2030 ($M) - Regional Industry Research

4.6 High-Density Polyethylene Market 2023-2030 ($M) - Regional Industry Research

4.7 Polycarbonate Market 2023-2030 ($M) - Regional Industry Research

4.8 Polybutylene Terephthalate Market 2023-2030 ($M) - Regional Industry Research

5.Europe Automotive Plastics Market for Passenger Cars By Product Type Market 2023-2030 ($M)

5.1 Polypropylene Market 2023-2030 ($M) - Regional Industry Research

5.2 Polyurethane Market 2023-2030 ($M) - Regional Industry Research

5.3 Polyvinyl Chloride Market 2023-2030 ($M) - Regional Industry Research

5.4 Acrylonitrile-Butadiene-Styrene Market 2023-2030 ($M) - Regional Industry Research

5.5 Polyamide Market 2023-2030 ($M) - Regional Industry Research

5.6 High-Density Polyethylene Market 2023-2030 ($M) - Regional Industry Research

5.7 Polycarbonate Market 2023-2030 ($M) - Regional Industry Research

5.8 Polybutylene Terephthalate Market 2023-2030 ($M) - Regional Industry Research

6.APAC Automotive Plastics Market for Passenger Cars By Product Type Market 2023-2030 ($M)

6.1 Polypropylene Market 2023-2030 ($M) - Regional Industry Research

6.2 Polyurethane Market 2023-2030 ($M) - Regional Industry Research

6.3 Polyvinyl Chloride Market 2023-2030 ($M) - Regional Industry Research

6.4 Acrylonitrile-Butadiene-Styrene Market 2023-2030 ($M) - Regional Industry Research

6.5 Polyamide Market 2023-2030 ($M) - Regional Industry Research

6.6 High-Density Polyethylene Market 2023-2030 ($M) - Regional Industry Research

6.7 Polycarbonate Market 2023-2030 ($M) - Regional Industry Research

6.8 Polybutylene Terephthalate Market 2023-2030 ($M) - Regional Industry Research

7.MENA Automotive Plastics Market for Passenger Cars By Product Type Market 2023-2030 ($M)

7.1 Polypropylene Market 2023-2030 ($M) - Regional Industry Research

7.2 Polyurethane Market 2023-2030 ($M) - Regional Industry Research

7.3 Polyvinyl Chloride Market 2023-2030 ($M) - Regional Industry Research

7.4 Acrylonitrile-Butadiene-Styrene Market 2023-2030 ($M) - Regional Industry Research

7.5 Polyamide Market 2023-2030 ($M) - Regional Industry Research

7.6 High-Density Polyethylene Market 2023-2030 ($M) - Regional Industry Research

7.7 Polycarbonate Market 2023-2030 ($M) - Regional Industry Research

7.8 Polybutylene Terephthalate Market 2023-2030 ($M) - Regional Industry Research

LIST OF FIGURES

1.US Automotive Plastics Market Revenue, 2023-2030 ($M)2.Canada Automotive Plastics Market Revenue, 2023-2030 ($M)

3.Mexico Automotive Plastics Market Revenue, 2023-2030 ($M)

4.Brazil Automotive Plastics Market Revenue, 2023-2030 ($M)

5.Argentina Automotive Plastics Market Revenue, 2023-2030 ($M)

6.Peru Automotive Plastics Market Revenue, 2023-2030 ($M)

7.Colombia Automotive Plastics Market Revenue, 2023-2030 ($M)

8.Chile Automotive Plastics Market Revenue, 2023-2030 ($M)

9.Rest of South America Automotive Plastics Market Revenue, 2023-2030 ($M)

10.UK Automotive Plastics Market Revenue, 2023-2030 ($M)

11.Germany Automotive Plastics Market Revenue, 2023-2030 ($M)

12.France Automotive Plastics Market Revenue, 2023-2030 ($M)

13.Italy Automotive Plastics Market Revenue, 2023-2030 ($M)

14.Spain Automotive Plastics Market Revenue, 2023-2030 ($M)

15.Rest of Europe Automotive Plastics Market Revenue, 2023-2030 ($M)

16.China Automotive Plastics Market Revenue, 2023-2030 ($M)

17.India Automotive Plastics Market Revenue, 2023-2030 ($M)

18.Japan Automotive Plastics Market Revenue, 2023-2030 ($M)

19.South Korea Automotive Plastics Market Revenue, 2023-2030 ($M)

20.South Africa Automotive Plastics Market Revenue, 2023-2030 ($M)

21.North America Automotive Plastics By Application

22.South America Automotive Plastics By Application

23.Europe Automotive Plastics By Application

24.APAC Automotive Plastics By Application

25.MENA Automotive Plastics By Application

26.Magna International Inc., Sales /Revenue, 2015-2018 ($Mn/$Bn)

27.Lear Corporation, Sales /Revenue, 2015-2018 ($Mn/$Bn)

28.Adient PLC, Sales /Revenue, 2015-2018 ($Mn/$Bn)

29.BASF SE, Sales /Revenue, 2015-2018 ($Mn/$Bn)

30.Compagnie Plastic Omnium, Sales /Revenue, 2015-2018 ($Mn/$Bn)

31.Borealis AG, Sales /Revenue, 2015-2018 ($Mn/$Bn)

32.Covestro AG, Sales /Revenue, 2015-2018 ($Mn/$Bn)

33.Evonik Industries AG, Sales /Revenue, 2015-2018 ($Mn/$Bn)

34.Saudi Basic Industries Corporation SJSC, Sales /Revenue, 2015-2018 ($Mn/$Bn)

35.Grupo Antolin-Irausa S.A., Sales /Revenue, 2015-2018 ($Mn/$Bn)