Email

Email Print

Print

Telecom System Integration Service Market- By Type; By Absorption Units; By Transmission; By Measurement; By End-User; By Geography- Forecast 2024-2030

Telecom System Integration Market Overview

The Global Telecom System Integration Market size is forecast to reach $43.6 billion by 2030, growing at a CAGR of 9% from 2024 to 2030. The telecom system integration market is evolving with several prominent trends shaping its landscape. One significant trend is the increasing adoption of cloud-based solutions, driven by the need for scalability, flexibility, and cost-efficiency in telecom networks. Cloud integration enables telecom operators to streamline operations, deploy services faster, and reduce capital expenditure on infrastructure. Another key trend is the rise of 5G technology and its integration into existing telecom networks. System integrators are playing a crucial role in implementing 5G infrastructure, including radio access networks (RAN), core networks, and edge computing platforms, to support enhanced mobile broadband and IoT applications. Additionally, there is a growing demand for cybersecurity integration as telecom networks become more interconnected and vulnerable to cyber threats. System integrators are focusing on implementing robust security measures to protect sensitive data and ensure regulatory compliance. Moreover, the trend towards network virtualization and software-defined networking (SDN) is driving the need for expertise in integrating virtualized network functions (VNFs) and orchestrating network resources efficiently.

The Telecom System Integration (TSI) services market has experienced substantial growth and transformation, driven by several key trends and developments in 2022 and 2023. One of the most significant trends is the rapid adoption of 5G technology. As telecom operators worldwide deploy 5G networks, there is an increasing demand for system integration services to ensure seamless implementation, optimization, and management of these complex networks. This includes integrating new 5G infrastructure with existing 4G LTE and legacy systems, which requires expertise in hybrid network environments.

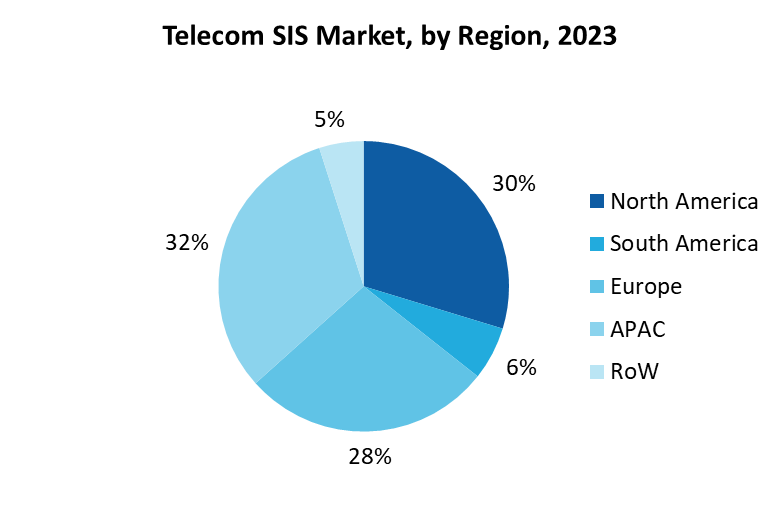

Market Snapshot:

Telecom System Integration Market Report Coverage

The report: “Telecom System Integration Industry Outlook – Forecast (2024-2030)”, by IndustryARC covers an in-depth analysis of the following segments of the Telecom System Integration Industry.

By Services: Planning and Consulting, Infrastructure Integration, Application Integration, Support and Maintenance

By Radio Technology: 5G (5G New Radio Standalone Architecture, 5G New Radio Non-Standalone Architecture), Non 5G

By End Users: Manufacturing (Medical & Pharmaceutical, Chemical, Food & Beverage, FMCG, Metal, Machinery & Equipment, Semiconductor & Electronics, Others), Transportation & Logistics, Consumer, Oil & Gas, Automotive, Ports, Energy, Smart City, Smart Building, Retail, Agriculture, Healthcare, Education, Smart Events & Stadia, Mining, Utilities, Others

By Geography: North America (US, Canada, Mexico), Europe (Germany, U.K, France, Spain, Italy, Others), APAC (China, Japan, Malaysia, Thailand, South Korea, Philippines, Hong Kong, Others), South America (Brazil, Argentina and others), RoW (Middle East and Africa)

Key Takeaways

- 5G Telecom is analyzed to witness highest growth in the Telecom System Integration Market during 2024-2030 owing to higher speed, ultra reliability, lower latency and so on.

- APAC Telecom System Integration Market held the largest share in 2023, attributing to factors like rising demand for the development of technologically advanced solutions that aid in improving supply chain agility, along with minimizing operational time and reducing distribution costs among manufacturers as a part of optimizing smart industrial operations including process automation, remote monitoring, collaborative robots, predictive analytics, augmented reality, additive manufacturing.

- Increasing penetration of industry 4.0 across globe combining artificial intelligence, machine vision with operational technology as a part of optimizing productivity in industrial environments along with growing demand for augmented reality and virtual reality applications in consumer and retail sector as a part of achieving ultimate immersive experience are analyzed to significantly drive the global Telecom System Integration Market during the forecast period 2024-2030.

Telecom System Integration Segment Analysis- By Radio Technology

By radio technology, global Telecom System Integration Market has been segmented into 5G and non 5G technology. 5G technology is analyzed to grow with the highest CAGR of 17.5% during the forecast period 2024-2030. As compared to non 5G technology, 5G architecture acts as a faster solution, enabling higher multi-Gbps peak data speeds, ultra-low latency, more reliability, massive network capacity, increased availability attributing to its market growth. 5G is used across three main types of connected services, including enhanced mobile broadband, mission-critical communications, and the massive IoT for businesses needing the high speed, low latency, and network capacity that 5G is designed to provide, and thus such beneficiary capabilities of 5G technology are boosting its market growth. In November 2021, Ericsson announced its partnership with Korean communications service provider, SK Telecom, to support 5G Standalone networks through the deployment of cloud-native dual-mode 5G Core on its Cloud Native Infrastructure (CNIS). Such factors are further set to propel the market growth of global Telecom System Integration Market in the long run.

Telecom System Integration Segment Analysis- By End Users

Manufacturing sector dominated the global Telecom System Integration Market acquiring a market share of 24.7% in 2023. The burgeoning demand for mission critical communication with ultra-reliable, available, low-latency links like remote control of critical infrastructure, vehicles, and medical procedures is attributing to the market growth. Rising investment towards seamlessly connecting a massive number of embedded sensors in virtually everything through the ability to scale down in data rates, power, and mobility, providing extremely lean and low-cost connectivity solutions is another prime factor contributing towards market growth. According to a report published by Qualcomm, 5G is designed to deliver peak data rates up to 20 Gbps based on IMT-2020 requirements, and such factors are contributing towards expansion of global Telecom System Integration Market. In December 2021, China’s Sinopec Hainan Refining & Chemical Limited Company initiated the second phase of a 5G deployment project in Hainan. Seven base stations have been completed in the first phase and the rest of 15 base stations are expected to complete in the upcoming second phase by 2024. The high bandwidth 5G network decreases the lag affecting intercom system and patrol drones across 4G networks and increases working efficiency significantly. Such factors are set to drive the market forward in the coming years.

A major driver in the telecom system integration market in Manufacturing is the accelerated pace of digital transformation initiatives by telecom operators and enterprises. As businesses strive to adapt to evolving customer demands and technological advancements, there is a heightened focus on modernizing legacy systems and integrating new digital technologies seamlessly. Telecom system integrators play a pivotal role in helping organizations leverage emerging technologies such as AI, IoT, and big data analytics to enhance operational efficiency, improve customer experiences, and drive innovation. The shift towards digital transformation encompasses upgrading infrastructure for improved connectivity, implementing advanced communication platforms for seamless collaboration, and deploying agile and scalable solutions to support dynamic business needs. This driver is pushing telecom system integrators to innovate and collaborate closely with stakeholders to design and implement tailored solutions that empower organizations to thrive in the digital era.

Telecom System Integration Segment Analysis- By Geography

By Geography, Telecom System Integration Market has been segmented into North America, Europe, APAC, South America and Others. APAC dominated the global Telecom System Integration Market with a share of 32% in 2023, owing to exponential growth in factory automation and digitalization in manufacturing sector in this region. The growing adoption of government strategies to promote digitization in government sector along with private sector leveraging advanced communication infrastructure could be considered vital in driving the Telecom System Integration Market growth forward in the coming years. Growing adoption of smart manufacturing utilizing advanced technologies such as AI and IoT in delivering digital transformation (DX) for plant operations, including field automation and remote support is impacting the growth of system integration services in this region. The growing investments towards smart city infrastructure to enhance services like traffic management systems, essential communication services, and city-wide surveillance schemes leveraging AI, automation and IoT is another prime factor driving the market growth forward. In February 2021, Rakuten Mobile and Ligado Networks announced about their collaboration on 5G mobile private networks connecting critical industries, such as farming, energy, logistics and public utilities to deliver continuity of coverage, local computer and connectivity integration, and greater control and security in Japan. Such developments are set to create significant growth opportunities for the market during 2024-2030.

For More Details on This Report - Request for Sample

Telecom System Integration Market Drivers

- Increasing penetration of industry 4.0 across globe combining artificial intelligence, machine vision with operational technology as a part of optimizing productivity in industrial environments are impacting the market growth

Increasing penetration of industry 4.0 across globe combining artificial intelligence, machine vision with operational technology as a part of addressing worker safety, optimizing field operations, and boosting maintenance productivity in industrial environments is considered vital in driving the Telecom System Integration. Adding to this, rising integration of 5G and Block-Chain Technologies in smart manufacturing leveraging IoT provides strategic unison among connected devices offering optimized remote observation for the assessment and management of the infrastructure while ensuring cost optimization. System integration helps in connecting the different areas of an industry in order to extract data, information. In addition, it also make continuous improvements throughout the manufacturing process. Furthermore growing inclination towards mixed reality platform (AR and VR) is optimizing the integration of process applications involved in process simulation, flow sheets, datasheets, 3D model, etc. It monitors performance in real time using sensors to measure variables and transmit information to control rooms and other applications. In November 2021, Huawei and China Mobile jointly deployed 5G enabled manufacturing solutions powered by mobile edge computing (MEC) at Haier’s smart factories. Haier is leveraging advanced technologies like artificial intelligence and machine vision at seven smart factories in China and has expanded 20 factories as of 2022. Such new development is set to fuel the market growth in the long run.

Moreover, the rise of edge computing has become a crucial trend, significantly impacting the TSI market. Edge computing reduces latency by processing data closer to the source, which is vital for applications such as IoT, autonomous vehicles, and real-time analytics. Telecom system integrators are now focusing on deploying and managing edge data centers, ensuring they are efficiently integrated with core networks and cloud platforms. Another critical trend is the increasing importance of cybersecurity in telecom system integration. With the growing incidence of cyber threats, telecom companies are investing heavily in robust security measures. System integrators are playing a pivotal role in integrating comprehensive cybersecurity solutions that safeguard networks, data, and infrastructure. This involves implementing advanced encryption, intrusion detection systems, and AI-driven threat intelligence.

- Growing demand for augmented reality and virtual reality applications in consumer and retail sector as a part of achieving ultimate immersive experience drives its market forward

Growing adoption of AR/VR in retail sectors to engage more effectively with customers by immersing them in highly informative and engaging experiences act as a major driver boosting its market growth. The emergence of advanced technologies like AR-based apps can help retailers to provide navigation assistance to customers inside stores and help them avoid getting lost while traversing endless aisles for various products. It can also help customers to have a pleasant shopping experience by leading them to the shelf they are looking for. For instance, Lowe’s, a North American giant of home enhancement goods, employs an HTC Vive and a unique controller known as the ‘Holoroom Test Drive’ which lets anyone around power tools wear a VR headset and learn to work with the tools in a secured virtual space. In July 2021, Walmart has introduced a new augmented reality shopping experience in stores that encourages families to explore the aisles in search of AR gamification experience in order to unlock content. Such developments are analyzed to propel the global Telecom System Integration Market growth in the coming years.

Telecom System Integration Market Challenges

High initial cost associated with the deployment and installation of the IT system hinders its market growth

Telecom System Integration incurs high costs associated with installation, integration, deployment and additional maintenance services owing to its robust infrastructure combined with stringent security policies. Tencent has stated that, to deploy a 5G private network for a 1,000 sq meter smart factory in China has costed $2 million, including the 5G modules, terminals and RAN and core network. The up-front costs of a system integration project include the cost of materials, software licenses, travel, installation, and various sorts of technical labour. Small enterprises are limiting its adoptability due to its high financial requirement.There are a wide variety of factors that can significantly influence these costs for any given production line or process. Certain features, such as safety, product integrity, and equipment protection, tend to be universally desired. Others, like flexibility or ease of operations, can be a matter of budget, preference, process, or business requirements. All of these have an influence on both the initial up-front costs and the total true cost of the system over time. Many enterprises are still reluctant to adopt this technology due to limited budget allocation. Such factors have been creating an adverse impact on its market growth.

Telecom System Integration Market Landscape

Product innovations, acquisitions, Partnerships and R&D activities are key strategies adopted by players in the Telecom System Integration Market. Telecom System Integration top 10 companies include:

- Accenture PLC

- IBM Corporation

- Hewlett Packard Enterprise

- Wipro Limited

- Oracle Corporation

- Cisco Systems Inc.

- Ericsson

- HCL Technologies Ltd.

- Amdocs Ltd.

- Mavenir

For more Information and Communications Technology Market reports, please click here

1. Telecom System Integration Market Overview

1.1 Definitions and Scope

2. Telecom System Integration Market - Executive Summary

2.1 Market Revenue, Market Size and Key Trends by Company

2.2 Key trends By Service

2.3 Key trends By End Use Industry

2.4 Key trends segmented by Geography

3. Telecom System Integration Market – Market Landscape

3.1 Comparative Analysis

3.1.1 Product/Company Benchmarking-Top 5 Companies

3.1.2 Top 5 Financial Analysis

3.1.3 Market Value Split by Top 5 Companies

3.1.4 Patent Analysis

3.1.5 Pricing Analysis (Comparison of General Price of Industry Services)

4. Telecom System Integration Market – Industry Market Entry Scenario Premium

4.1 Regulatory Scenario

4.2 Ease of Doing Business Index

4.3 Case Studies

4.4 Customer Analysis

5. Telecom System Integration Market – Startup Company Scenario

5.1 Venture Capital and Funding Scenario

5.2 Startup Company Analysis

6. Telecom System Integration Market - Market Forces

6.1 Market Drivers

6.2 Market Constraints

6.3 Porters five force model

6.3.1 Bargaining power of suppliers

6.3.2 Bargaining powers of customers

6.3.3 Threat of new entrants

6.3.4 Rivalry among existing players

6.3.5 Threat of substitutes

7. Telecom System Integration Market – By Strategic Analysis (Market Size -$Million/Billion)

7.1 Value Chain Analysis

7.2 Opportunities Analysis

7.3 Product Life Cycle/Market Life Cycle Analysis

8. Telecom System Integration Market – By Services (Market Size -$Million/Billion)

8.1 Planning and Consulting

8.2 Infrastructure Integration

8.3 Application Integration

8.4 Support and Maintenance

9. Telecom System Integration Market – By Radio Technology (Market Size -$Million/Billion)

9.1 5G

9.1.1 5G New Radio Standalone Architecture

9.1.2 5G New Radio Non-Standalone Architecture

9.2 Non-5G Telecom

10. Telecom System Integration Market – By Industry Vertical (Market Size -$Million/Billion)

10.1 Manufacturing

10.1.1 Medical and Pharmaceutical

10.1.2 Chemicals

10.1.3 Food and Beverage

10.1.4 FMCG

10.1.5 Metal

10.1.6 Machinery and Equipment

10.1.7 Semiconductor and Electronics

10.1.8 Others

10.2 Transportation and Logistics

10.2.1 Supply Chain

10.2.2 Warehousing/Logistics

10.2.3 Rail

10.3 Consumer

10.4 Ports

10.5 Automotive

10.6 Oil and Gas

10.6.1 Upstream

10.6.2 Midsteam

10.6.3 Downstream

10.7 Energy

10.7.1 Power Generation

10.7.2 Transmission and Distribution

10.8 Smart Cities

10.8.1 Infrastructure

10.8.2 Transit

10.8.3 Government Buildings

10.8.4 Others

10.9 Smart Buildings

10.10 Retail

10.11 Agriculture

10.12 Healthcare

10.12.1 Hospitals

10.12.2 Clinics and Diagnostic Centers

10.12.3 Elder Care Facilities

10.13 Education

10.14 Smart Events & Stadia (major events, conferences, sports and concerts)

10.15 Mining

10.16 Utilities

10.17 Others

11. Telecom System Integration Market - By Geography (Market Size -$Million/Billion)

11.1 North America

11.1.1 US

11.1.2 Canada

11.1.3 Mexico

11.2 Europe

11.2.1 Germany

11.2.2 UK

11.2.3 France

11.2.4 Spain

11.2.5 Italy

11.2.6 Others

11.3 APAC

11.3.1 China

11.3.2 Japan

11.3.3 South Korea

11.3.4 Thailand

11.3.5 Philippines

11.3.6 Hong Kong

11.3.7 Malaysia

11.3.8 Others

11.4 South America

11.4.1 Brazil

11.4.2 Argentina

11.4.3 Others

11.5 RoW

11.5.1.1 Middle East

11.5.1.2 Africa

12. Telecom System Integration Market - Market Entropy

12.1 New product launches

12.2 M&A's, collaborations, JVs and partnerships

13. Telecom System Integration Market – Industry Competitive Landscape

13.1 Market Share – Global

13.2 Market Share by Region

13.3 Market Share By Industry Vertical

13.4 Market Share By Application

14. Telecom System Integration Market – Key Company List by Country Premium

15. Telecom System Integration Market - Company Analysis

15.1 Accenture PLC

15.2 IBM Corporation

15.3 Hewlett Packard Enterprise

15.4 Wipro Limited

15.5 Oracle Corporation

15.6 Cisco Systems Inc.

15.7 Ericsson

15.8 HCL Technologies Ltd.

15.9 Amdocs Ltd

15.10 Mavenir

"*Financials would be provided on a best-efforts basis for private companies"