Email

Email Print

Print

Cogeneration Equipment Market - By Capacity , By Technology , By Fuel , By Geography - Forecast (2024 - 2030)

Cogeneration Equipment Market Overview

Cogeneration Equipment market size is forecast to reach US$53 billion by 2030, after growing at a CAGR of 7.9% during 2024-2030. The cogeneration equipment market is driven by the need for energy efficiency and cost savings, compliance with environmental regulations, and the demand for reliable power supply. Rising energy costs and government incentives further boost adoption. Technological advancements, increasing industrialization and urbanization and energy security concerns also play significant roles. These factors collectively promote the use of cogeneration systems, which provide efficient, sustainable, and cost-effective energy solutions for various industries and urban areas, helping reduce greenhouse gas emissions and operational expenses.

The cogeneration equipment market is driven by two significant trends: the integration of renewable energy sources and the adoption of digital technologies. Industries are increasingly using biomass, biogas and other fuel alternatives in cogeneration systems to enhance energy efficiency and comply with environmental regulations. This shift supports global sustainability goals. Additionally, digitalization and smart technologies are being integrated into cogeneration equipment enabling real-time monitoring, predictive maintenance and optimized performance. These advancements reduce operational costs and improve system reliability. For instance, American Institute of Chemical Engineers (AIChE) highlights cogeneration's economic benefits while the International Energy Agency (IEA) emphasizes its role in reducing emissions and supporting clean energy transitions.

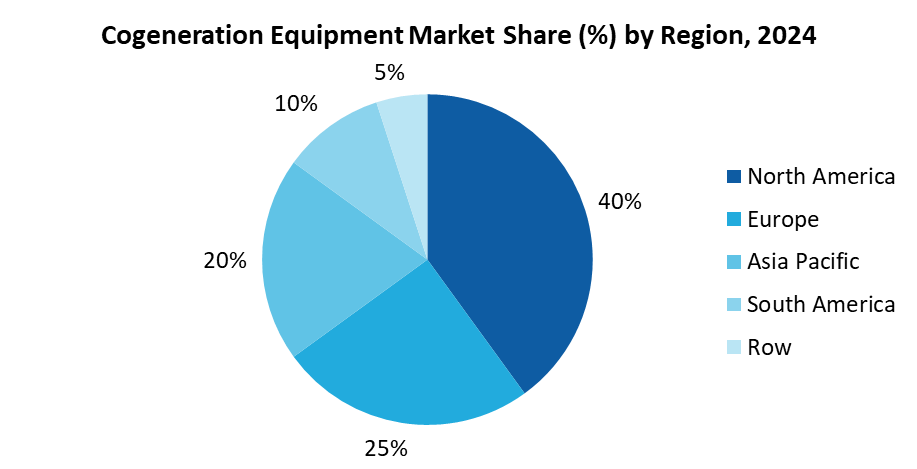

Market Snapshot:

Cogeneration Equipment Market Report Coverage

The report "Cogeneration Equipment Market Report – Forecast (2024-2030)" by IndustryARC covers an in-depth analysis of the following segments of the Cogeneration Equipment market.

| Attribute | Segment |

|---|---|

|

By Type |

|

|

By Capacity |

|

|

By Fuel Type |

|

|

By Application |

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- The COVID-19 pandemic severely impacted the cogeneration equipment market by delaying projects in industries like manufacturing and energy. Closure restrictions and workforce shortages resulted in equipment installations and maintenance slowdowns. In certain industries, such as healthcare and data centers, which depend heavily on continued power availability, were delayed in upgrading cogeneration systems and these delays directly affected operational efficiency as well as energy reliability.

- The Russia-Ukraine war triggered an energy crisis in Europe, where many countries depend on Russian gas for cogeneration. Sanctions on Russia resulted in cogeneration plants to incur increased operational cost and delay in new installations. Furthermore, uncertainties in the energy policies to which energy-demanding plants in affected regions would be exposed also delayed investment in new cogeneration projects causing companies to change their strategies for equipment procurement and energy sourcing.

Key Takeaways

Combined Cycle is the Largest Segment

Combined Cycle cogeneration systems are dominating the cogeneration equipment market due to their high efficiency and versatility. These systems integrate gas and steam turbines, utilizing waste heat from the gas turbine to produce steam which then drives a steam turbine, maximizing energy output. This process enhances efficiency achieving thermal efficiencies of up to 90%, which significantly surpasses single-cycle systems according to the U.S. Department of Energy (DOE) and GE Vernova. Additionally, Combined Cycle systems are highly adaptable to various fuel types including natural gas and biofuels making them a flexible and sustainable option for diverse energy needs. According to the U.S. Energy Information Administration (EIA), more than half of the natural gas-fired electric-generating capacity in the U.S. consists of combined-cycle systems. Government incentives, such as tax credits in the U.S. and supportive policies in the EU, further bolster the adoption of these systems.

Commercial Segment is the Largest Application

The commercial segment is dominating the cogeneration equipment market primarily due to government incentives. The U.S. Inflation Reduction Act offers a 30% federal tax credit for Combined Heat and Power (CHP) system, significantly reducing the cost of installing and operating these systems in commercial buildings. Additionally, various federal grants and tax incentives are available to encourage energy-efficient upgrades in commercial buildings. The Department of Energy notes that the Energy Policy Act provides tax deductions for energy-efficient property installations further motivating commercial facilities to adopt cogeneration systems. Moreover, the commercial sector is driven by the need for energy reliability and cost savings. Cogeneration systems offer significant efficiency improvements by simultaneously producing electricity and useful heat reducing overall energy costs and enhancing energy security. This is particularly beneficial for commercial buildings that have consistent and high energy demand such as hospitals, hotels, and office complexes. These incentives and benefits make cogeneration systems financially attractive and align with broader sustainability goals driving the commercial segment to adopt these technologies more rapidly than other sectors.

North America Dominates the Market

The North American region is dominating the cogeneration equipment market due to a combination of supportive government policies, high energy consumption and a strong emphasis on energy efficiency and sustainability. The U.S. government implemented several incentives and regulations promoting cogeneration also known as combined heat and power (CHP) as part of its broader strategy to improve energy efficiency and reduce greenhouse gas emissions. This led to significant investments in cogeneration technology, especially in industrial and commercial sectors. For instance, In April 2023, specialty chemicals company, Orion Engineered Carbons announced the installation of cogeneration technology at its Ivanhoe plant in Louisiana. This upgrade increased efficiency, reliability and sustainability while producing renewable energy. Additionally, the U.S. Energy Information Administration (EIA) reports that the adoption of renewable energy sources has been on the rise further driving the market. The region's robust energy infrastructure and the need to modernize aging power plants also contribute to the growth of cogeneration equipment ensuring reliable and efficient energy supply across various industries.

Increased Efficiency and Cost Savings Propel Cogeneration Equipment Adoption

One of the primary drivers in the cogeneration equipment market is its superior energy efficiency and the resultant cost savings. Cogeneration systems also known as combined heat and power (CHP) systems simultaneously generate electricity and useful thermal energy from the same energy source effectively utilizing fuel that would otherwise be wasted. This efficiency leads to significant reductions in energy costs for users. According to the U.S. Environmental Protection Agency (EPA), CHP systems can achieve efficiencies of over 80% compared to the typical 50% efficiency of separate heat and power generation. This substantial efficiency translates directly into lower operational costs and improved energy security for industries and facilities, making CHP an attractive investment.

Environmental Regulations and Sustainability Goals to Drive Growth

Environmental regulations and sustainability goals are also major drivers in the cogeneration equipment market. Governments worldwide are increasingly implementing stringent regulations aimed at reducing greenhouse gas emissions and promoting energy efficiency. CHP systems are recognized for their environmental benefits, as they significantly lower carbon dioxide emissions compared to traditional power generation methods. The U.S. Department of Energy emphasizes that CHP systems can reduce emissions by up to 50% compared to conventional fossil fuel power plants. Additionally, the European Association for the Promotion of Cogeneration (COGEN Europe) highlights, cogeneration, also known as Combined Heat and Power (CHP), plays a crucial role in helping Europe reach its goal of carbon neutrality by 2050. This alignment with regulatory and sustainability frameworks positions cogeneration equipment as a vital component in achieving both national and global environmental goals.

For more details on this report - Request for Sample

Cogeneration Equipment Market Challenges

High Initial Investment Hampers Cogeneration Adoption

One of the major challenges in the Cogeneration Equipment Market is the high initial capital investment required for setting up cogeneration systems. This significant upfront cost includes expenses for purchasing and installing advanced equipment, integrating the system with existing infrastructure, and ensuring compliance with regulatory requirements. For instance, T&T Power Group highlights that the capital costs for cogeneration systems can be quite high, averaging around $700/kW, which can significantly burden the owner if they are responsible for absorbing these upfront costs. Furthermore, the return on investment (ROI) can take as long as 6 years to materialize. These costs can be particularly prohibitive for small and medium-sized enterprises, making it difficult for them to adopt cogeneration technologies. Moreover, the complexity and customization needed for each installation further drive up the expenses. Additionally, the American Institute of Chemical Engineers (AIChE) highlights that achieving optimal operational efficiency and energy savings through cogeneration requires a substantial initial outlay, which can be a barrier for widespread adoption.

Cogeneration Equipment Industry Outlook

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in the Cogeneration Equipment market. Global Cogeneration Equipment top 10 companies include:

- GE Vernova

- Siemens AG

- Mitsubishi Heavy Industries, Ltd.

- ABB Ltd.

- Caterpillar Inc.

- Cummins Inc.

- Capstone Turbine Corporation

- MAN Diesel & Turbo SE

- 2G Energy AG

- Wärtsilä Corporation

Scope of the Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

7.9% |

|

Market Size in 2030 |

$53 Billion |

|

Segments Covered |

By Type, By Capacity, By Fuel Type, By Application and By Geography.

|

|

Geographies Covered |

North America (U.S, Canada and Mexico), Europe (UK, Germany, Italy, France, Spain, Netherlands, Denmark, Belgium, and Rest of Europe), Asia Pacific (China, Japan, India, South Korea, Australia and New Zealand, Thailand, Indonesia, Malaysia, and Rest of Asia Pacific), South America (Brazil, Argentina, Colombia, Chile, and Rest of South America), RoW (Middle East and Africa) |

|

Key Market Players |

1. GE Vernova 2. Siemens AG 3. Mitsubishi Heavy Industries, Ltd. 4. ABB Ltd. 5. Caterpillar Inc. 6. Cummins Inc. 7. Capstone Turbine Corporation 8. MAN Diesel & Turbo SE 9. 2G Energy AG 10. Wärtsilä Corporation |

For more Energy and Power Market reports, please click here

The Cogeneration Equipment Market is projected to grow at 7.9% CAGR during the forecast period 2024-2030.

The Cogeneration Equipment Market size is estimated to be $31.13 billion in 2023 and is projected to reach $53 billion by 2030

The leading players in the Cogeneration Equipment Market are GE Vernova, Siemens AG, Mitsubishi Heavy Industries, Ltd., ABB Ltd., Caterpillar Inc. and others

Integration of renewable energy sources and the adoption of digital technologies are some of the major Cogeneration Equipment Market trends in the industry which will create growth opportunities for the market during the forecast period.

The need for energy efficiency, compliance with regulations, rising energy costs, and reliable power are the driving factors of the market.