Email

Email Print

Print

Medicated Pain Relieving Plasters Market - Forecast(2025 - 2031)

The global medicated pain-relieving plasters market has been experiencing significant growth, with its market value projected $6,230.3 million in 2031, reflecting a CAGR of 6.6% between 2025 and 2031. This increase is primarily driven by the rising prevalence of chronic pain conditions, such as arthritis, back pain, and musculoskeletal disorders, which are becoming more common due to aging populations and sedentary lifestyles. Additionally, the growing consumer preference for non-invasive and drug-free pain relief options has propelled demand for medicated plasters, which provide targeted relief with fewer systemic side effects than oral medications. Advancements in transdermal drug delivery technology have also improved product effectiveness, leading to better adhesion, longer duration of action, and enhanced penetration of active ingredients. The increasing trend of self-medication and over-the-counter (OTC) pain management solutions has further boosted the market, as consumers seek easy-to-use alternatives for pain relief. However, despite these growth drivers, challenges such as regulatory hurdles, potential product recalls, and competition from alternative pain relief methods, including topical gels and oral painkillers, may pose limitations to market expansion. Additionally, price sensitivity and limited awareness in certain developing regions could restrain the full market potential.

Market Snapshot :

Report Coverage

The report: “Medicated Pain Relieving Plasters Market Forecast (2025-2031)", by Industry ARC covers an in-depth analysis of the following segments of the Medicated Pain Relieving Plasters Market.

By Product- Non-Steroidal Anti-Inflammatory Drugs (NSAIDs), Topical Analgesics, Local Anesthetics, Combination Formulations.

By Usage - Occasional Use, Regular Use, Chronic Use.

By Availability - OTC, Prescription.

By Distribution Channel- Pharmacies, Online Retail, Supermarkets/Hypermarkets, Hospitals/Clinics, Others.

By Application - Muscular and Joint Pain, Headaches, Post-Surgical Pain, Neuropathic Pain, Sports Injuries, Chronic Pain, Others.

By Geography- North America (U.S, Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Russia and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand, and Rest of Asia-Pacific), South America (Brazil, Argentina, Chile, Colombia and Rest of South America), and Rest Of The World (Middle East, Africa).

Key Takeaways

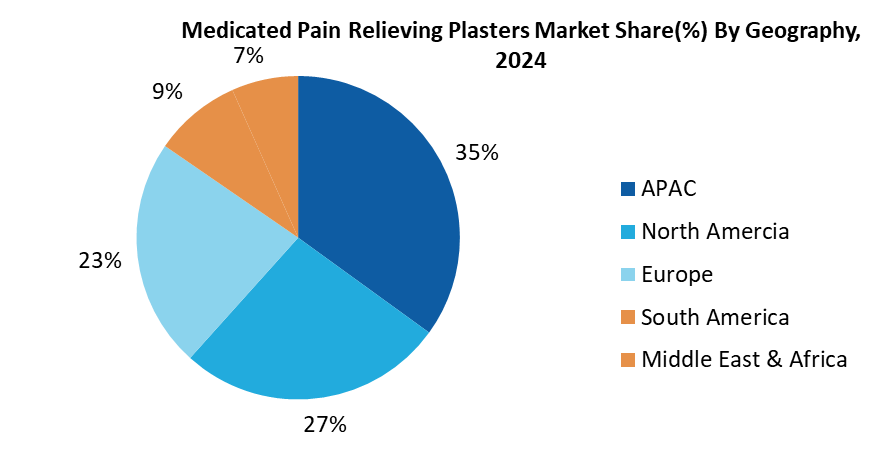

• Asia-Pacific dominates the market, reaching 35% market share in 2024, driven by aging populations, rising musculoskeletal disorders, and a mix of traditional and modern pain management solutions.

• Regulatory approvals fuel innovation, with China’s NMPA approving 210 medical devices in August 2022 and Japan’s Teikoku Seiyaku securing FDA approval for ALLYDONE®, expanding treatment applications.

• Growing preference for non-opioid pain relief in North America and Europe is driving demand for lidocaine and NSAID-based plasters, supported by expanding pharmacy networks and personalized pain management plans.

Medicated Pain Relieving Plasters Market Segmentation Analysis - By Product

The NSAID segment of the Medicated Pain-Relieving Plasters Market led with a valuation of $1,583.5 million and is projected to reach $2,536.4 million by 2031, growing at a 7.2% CAGR (2025-2031). The market is evolving with advancements in NSAID plasters, topical analgesics, and combination formulations, offering targeted pain relief with minimal systemic side effects. Unlike oral NSAIDs, which can cause gastrointestinal and cardiovascular issues, transdermal plasters provide sustained relief with fewer adverse effects. Studies indicate that 78% of patients with musculoskeletal pain found NSAID plasters more effective than oral alternatives. Additionally, the rising elderly population and the prevalence of chronic pain, affecting over 1.5 billion people globally, are driving demand for easy-to-use pain management solutions. Technological advancements, such as hydrogel and nanotechnology-based plasters, have enhanced efficacy and consumer adoption. Combination formulations, integrating multiple active pharmaceutical ingredients (APIs), are gaining prominence in orthopedic care, sports medicine, and geriatric pain management, particularly for conditions like osteoarthritis and neuropathic pain, reinforcing their role as a key market innovation.

Medicated Pain Relieving Plasters Market Segmentation Analysis - By Usage Type

The medicated pain-relieving plaster market is segmented into occasional, regular, and chronic use, each addressing distinct pain management needs. The occasional use segment, driven by the growing participation in recreational sports and fitness activities—up by over 30% in the past decade—caters to individuals seeking immediate relief for temporary injuries, such as sports-related strains or muscle pain from physically demanding jobs. This segment generated $1,956.7 million, and it is projected to reach $2,815.4 million by 2031, growing at a CAGR of 5.6% (2025-2031). Regular use plasters are vital in occupational health, particularly for repetitive strain injuries and conditions like post-herpetic neuralgia, with some products offering antiseptic benefits. Meanwhile, the chronic use segment is expanding due to its non-invasive approach to managing long-term pain conditions like arthritis and diabetic neuropathy, which affect 1.71 billion people globally. Studies, such as one by China Pharmaceutical University in October 2024, highlight the efficacy of 5% lidocaine plasters in providing safer alternatives to systemic analgesics. Overall, medicated plasters are gaining traction as versatile, accessible solutions for athletes, workers, and chronic pain sufferers alike.

Medicated Pain Relieving Plasters Market Segmentation Analysis - By Availability

The availability segment divides the market into OTC (Over-the-Counter) and Prescription-based pain-relieving plasters. OTC products dominate the market, holding a significant share due to their easy accessibility, affordability, and consumer preference for self-medication. The 6.2% CAGR growth in this segment is fueled by rising disposable income, increased awareness of pain management solutions, and expanded product offerings in retail stores and online platforms. The shift toward e-commerce and direct-to-consumer sales has further propelled growth, as brands invest in digital marketing and subscription-based pain relief solutions. Prescription-based plasters, containing stronger active ingredients like lidocaine, diclofenac, and fentanyl, are primarily used for severe pain conditions, post-surgical recovery, and chronic pain disorders. This segment is expanding at a 7.4% CAGR, driven by increased physician recommendations, insurance coverage for pain management products, and a growing elderly population suffering from degenerative diseases. The rise in personalized pain management plans prescribed by healthcare professionals has contributed to higher demand in this segment. However, regulatory requirements and concerns over potential side effects of prolonged prescription plaster use could impact its growth in certain regions.

Medicated Pain Relieving Plasters Market Segmentation Analysis - By Distribution Channel

Pharmacies serve as a primary distribution channel for medicated pain-relieving plasters, offering both prescription and OTC products. In 2024, the segment generated $2,425.9 million, projected to reach $3,832.6 million by 2031, growing at a 7.0% CAGR (2025-2031). Their integration with sports medicine, physiotherapy, and geriatric care makes them crucial for self-care and home-based pain management. According to the Consumer Healthcare Products Association (CHPA), U.S. consumers purchase OTC products 26 times per year, compared to just three doctor visits, highlighting the critical role of pharmacies in providing easy access to pain relief solutions. Many pharmacies collaborate with clinics and therapy centers to improve product availability, further strengthening their market presence. Meanwhile, e-commerce platforms are rapidly expanding, driven by discounts, quick delivery, and a broader product range, with 60% of consumers preferring to buy OTC healthcare products online. Amazon and Alibaba launched their e-pharmacies in June 2024, accelerating digital healthcare adoption. Supermarkets/Hypermarkets facilitate impulse purchases and accessibility, with OTC healthcare product sales growing by 12% annually (2020–2024) in emerging markets, according to Euromonitor International. Hospitals & Rehabilitation Centers are key distribution points for post-surgical and musculoskeletal pain management, especially with the rising number of orthopedic and sports-related surgeries, as reported by Medical Tourism. Health & Wellness Stores attract consumers seeking alternative pain relief solutions, offering medicated plasters alongside herbal and muscle relaxant products. Direct Sales Channels are expanding in chronic pain management, leveraging demonstration-based marketing and home healthcare solutions in regions with limited pharmacy or clinic access.

Medicated Pain Relieving Plasters Market Segmentation Analysis - By Application

The Medicated Pain-Relieving Plasters Market is driven by increasing demand across multiple application segments, including muscular & joint pain, headache pain, sports injuries, chronic pain management, wound care, and post-surgical pain. The Muscular & Joint Pain segment dominates the market, generating $1,926.8 million in revenue in 2024 and is projected to reach $2,792.5 million by 2031, growing at a CAGR of 5.7% (2025-2031). The rising elderly population is a major driver, with the global 60+ population expected to reach 2.1 billion by 2050, significantly increasing musculoskeletal disorder prevalence. Additionally, growing participation in physical activities, marathons, and sports has led to a rise in muscular injuries. Studies indicate that pain-relieving plasters can reduce recovery time by 20% compared to oral medication in mild to moderate injuries, further driving demand.

Beyond this, the Headache Pain segment benefits from increasing demand for non-oral treatments, with 45% of chronic headache sufferers preferring topical solutions, per the International Headache Society. The Sports Injury segment is expanding as sports participation rises, with 1.35 million children suffering sports-related injuries annually and a 20% rise in reported injuries in 2021, followed by 12% in 2022 and 2% in 2023. The Chronic Pain Management segment, crucial for conditions like osteoarthritis and fibromyalgia, is fueled by 20% of adults suffering from chronic pain globally, according to NIH. Meanwhile, the Wound Care segment, including minor burns and post-surgical scar management, is growing due to demand for dual-action analgesic and healing solutions. Lastly, Post-Surgical Pain Management is a key application, as over 313 million surgical procedures are performed annually, with 80% of patients experiencing postoperative pain. Studies show lidocaine patches reduce post-surgical pain by 60% compared to oral NSAIDs, highlighting their potential as an alternative. With ongoing advancements in transdermal technology, medicated pain-relieving plasters are set for strong market expansion across multiple applications.

Medicated Pain Relieving Plasters Market Segmentation Analysis - By Geography

The Asia-Pacific region dominates the global medicated pain-relieving plasters market, accounting for the largest share in 2024 with $1,411.4 million, driven by rapidly aging populations, increasing musculoskeletal disorders, and a strong preference for traditional and modern pain management solutions. According to China's National Health Commission, 20% of the population was aged 60 or older by the end of 2022, a figure projected to exceed 30% within a decade, significantly boosting demand for pain relief solutions. A cost-effectiveness analysis in China found that 5% lidocaine-medicated plasters (LMPs) were more cost-effective than PGs, offering better clinical effectiveness and higher economic value. In August 2022, China's NMPA approved 210 medical devices, including a wound care product from Nantong Changyu Medical Technology Co., Ltd., underscoring regulatory support for pain management innovations. Japan’s market, deeply rooted in traditional medicine and advanced pharmaceutical innovations, is led by companies like Teikoku Seiyaku, which pioneered transdermal technology. In December 2022, Teikoku Seiyaku received FDA approval for ALLYDONE®, a medicated patch for treating early-onset dementia associated with Alzheimer's disease, expanding the scope of medicated plasters beyond pain relief. North America follows, with the U.S. witnessing rising demand for non-opioid pain relief solutions, such as lidocaine and NSAID-based plasters, amid growing awareness of opioid risks. Europe, led by Germany and the U.K., is experiencing steady growth due to expanding retail pharmacy networks and personalized pain management plans. Meanwhile, South America and the Middle East & Africa are emerging as high-potential markets, with South America projected to grow at an 8.5% CAGR, the highest among regions, fueled by increasing consumer spending on non-prescription healthcare products. Technological advancements, regulatory approvals, and rising awareness of topical pain management alternatives are expected to drive the market’s future growth globally.

Medicated Pain Relieving Plasters Market Drivers

Rising Prevalence of Chronic Pain Conditions:

The increasing prevalence of chronic pain conditions, such as arthritis, lower back pain, and musculoskeletal disorders, is a significant driver of the medicated pain-relieving plasters market. According to the World Health Organization (WHO), chronic pain affects approximately 20% of the global population, with aging populations and sedentary lifestyles exacerbating the issue. As individuals seek non-invasive and convenient solutions for pain management, medicated plasters have gained popularity due to their ease of use, targeted relief, and minimal side effects compared to oral medications. These plasters deliver active ingredients like menthol, lidocaine, or capsaicin directly to the affected area, providing localized relief without systemic exposure. The growing awareness of pain management and the preference for self-medication further fuel demand, especially among elderly populations and individuals with mobility issues. Additionally, the rise in sports-related injuries and occupational strains contributes to the market growth, as athletes and workers increasingly adopt plasters for quick and effective pain relief.

Advancements in Transdermal Drug Delivery Technology:

Technological advancements in transdermal drug delivery systems have significantly boosted the medicated pain-relieving plasters market. Innovations in patch design, adhesive formulations, and active ingredient delivery mechanisms have enhanced the efficacy, comfort, and duration of pain relief provided by these plasters. Modern plasters are designed to release therapeutic agents gradually over extended periods, ensuring sustained pain management and reducing the need for frequent reapplication. Additionally, the development of plasters with improved skin permeability and reduced irritation has expanded their appeal to a broader consumer base. The integration of natural and herbal ingredients, such as arnica and turmeric, has also attracted health-conscious consumers seeking alternative pain relief options. Furthermore, the growing trend of personalized medicine has led to the development of plasters tailored to specific pain types and patient needs, driving market differentiation and consumer loyalty. These technological advancements, coupled with increasing R&D investments by pharmaceutical companies, are expected to continue propelling the market forward.

Medicated Pain Relieving Plasters Market Challenges

Regulatory and Safety Concerns

One of the major challenges facing the medicated pain-relieving plasters market is the stringent regulatory requirements and safety concerns associated with their use. Regulatory bodies, such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA), impose rigorous standards for the approval and commercialization of medicated plasters to ensure their safety, efficacy, and quality. These regulations often require extensive clinical trials, toxicity studies, and post-market surveillance, which can be time-consuming and costly for manufacturers. Additionally, the potential for adverse reactions, such as skin irritation, allergies, or sensitization to the active ingredients or adhesives used in the plasters, poses a significant challenge. Consumers with sensitive skin or pre-existing dermatological conditions may be particularly vulnerable, limiting the product's applicability and market reach. Furthermore, the risk of misuse or overuse of medicated plasters, especially among elderly populations or individuals with chronic pain, raises concerns about systemic absorption of active ingredients and potential side effects. This has led to increased scrutiny from healthcare professionals and regulatory authorities, who emphasize the need for clear labeling, dosage instructions, and patient education. Compliance with these regulatory and safety standards not only increases production costs but also delays product launches, hindering market growth. Manufacturers must navigate these challenges by investing in robust research, quality control, and consumer education to ensure compliance and build trust, which can be a significant barrier for smaller players in the market.

Medicated Pain Relieving Plasters Market Competitive Landscape

Product launches, mergers and acquisitions, joint ventures, and geographical expansions are key strategies adopted by players in the Medicated Pain Relieving Plasters Market. The Medicated Pain Relieving Plasters top 10 companies are: Major players in the Medicated Pain Relieving Plasters are Hisamitsu Pharmaceutical Co., Inc., Teikoku Seiyaku Co., Ltd., Johnson & Johnson, Nichiban Co., Ltd., Beiersdorf AG, Teva Pharmaceutical Industries Ltd., Grünenthal GmbH, Solstice Medicine Company, AdvaCare Pharma, and Taisho Pharmaceutical Holdings Co., Ltd. & others.

Recent Developments

• 24 July 2024, Grünenthal announced the acquisition of US-based Valinor Pharma, LLC, making it the global owner of Movantik® (naloxegol), in a deal valued at approximately $250 million, including all royalty obligations. This acquisition strengthens Grünenthal’s presence in the U.S. and aligns with its strategic growth, having invested over €2 billion in M&A transactions since 2017. The transaction will be financed using available liquidity.

• 29 June 2023, Biolinq Incorporated, a medtech company specializing in biosensing technologies, announced an exclusive license agreement with Taisho Pharmaceutical Co., Ltd. Under this collaboration, Taisho Pharmaceutical will serve as the commercial partner for Biolinq’s novel biowearable glucose monitoring technology in Japan.